EV/EBITDA Sector-Relative Value on China A-Shares: When the Signal Can't Help You

We backtested sector-relative EV/EBITDA on 25 years of China A-share data (SHZ+SHH). The signal fires every year — but -3.66% annual lag vs SPY and -64.54% max drawdown tell the story. Sector-relative discounts in China don''t close on value logic; they follow policy cycles.

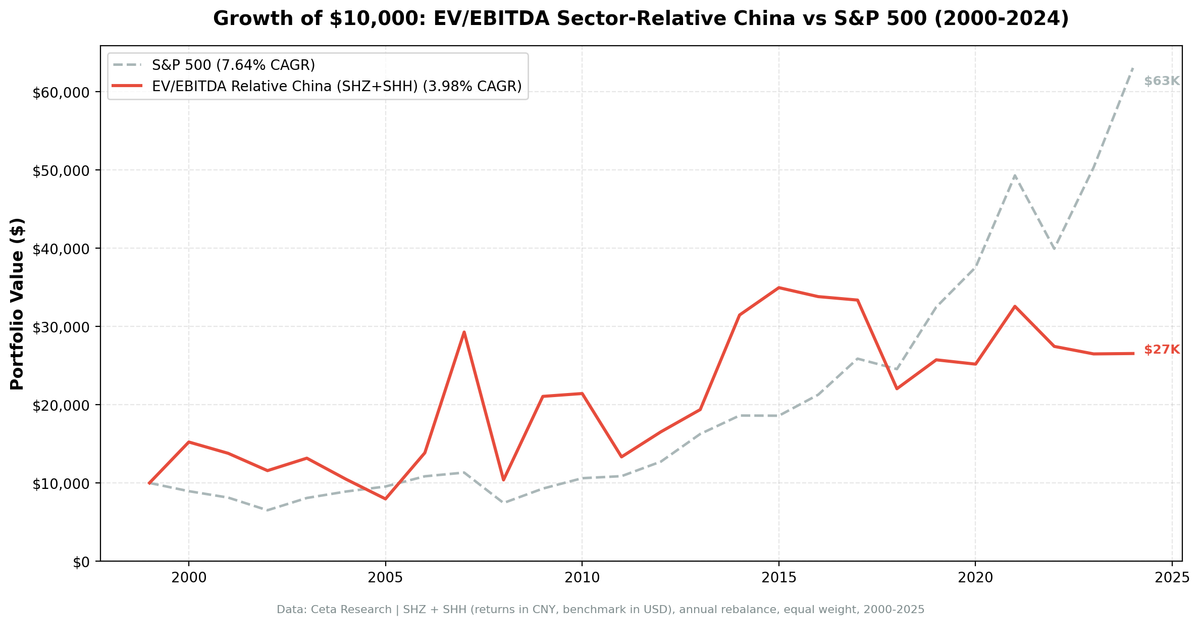

We ran a sector-relative EV/EBITDA screen on 25 years of China A-share data across SHZ and SHH. The signal always fires — zero cash periods, 22.8 average stocks per year — but 3.98% CAGR vs 7.64% SPY and a max drawdown of -64.54% tell the story. China is the clearest example in this study of a market where sector-relative discounts exist consistently but don't predict returns. The signal is measuring something real. It's just not the thing that drives Chinese stock prices.

Contents

- Method

- The Screen

- Sector-Relative EV/EBITDA Screen for China A-Shares (SQL)

- What We Found

- 25 years. Never in cash. Still trails SPY by 3.66% annually.

- The bubble years explain everything

- Year-by-year returns

- Why the signal can't help you in China

- 2011 and 2018: the painful down years

- The recent years (2016-2024): structural deterioration

- Backtest Methodology

- Limitations

- Conclusion

Method

| Parameter | Detail |

|---|---|

| Data source | Ceta Research (FMP financial data warehouse) |

| Universe | SHZ + SHH (China A-shares: Shenzhen + Shanghai), MCap > ¥2B |

| Signal | Stock EV/EBITDA < 70% of sector median (30%+ discount to peers) |

| EV/EBITDA range | 0.5-25x |

| Quality filters | ROE > 8%, D/E < 2.0 |

| Portfolio | Top 30 by deepest discount, equal weight |

| Rebalancing | Annual (January) |

| Cash rule | Hold cash if fewer than 10 stocks qualify |

| Period | 2000-2025 (25 years, 0 cash periods) |

| Benchmark | S&P 500 Total Return (SPY, USD) |

Financial data sourced from key_metrics_ttm for EV/EBITDA and market cap, financial_ratios_ttm for debt metrics, profile for sector classification. 45-day lag on all financial statements to prevent look-ahead bias.

The Screen

Sector-Relative EV/EBITDA Screen for China A-Shares (SQL)

WITH universe AS (

SELECT k.symbol, p.companyName, p.exchange, p.sector,

k.evToEBITDATTM AS ev_ebitda, k.returnOnEquityTTM AS roe,

fr.debtToEquityRatioTTM AS de, k.marketCap

FROM key_metrics_ttm k

JOIN financial_ratios_ttm fr ON k.symbol = fr.symbol

JOIN profile p ON k.symbol = p.symbol

WHERE k.evToEBITDATTM BETWEEN 0.5 AND 25

AND k.returnOnEquityTTM > 0.08

AND (fr.debtToEquityRatioTTM IS NULL OR (fr.debtToEquityRatioTTM >= 0 AND fr.debtToEquityRatioTTM < 2.0))

AND k.marketCap > 2000000000

AND p.sector IS NOT NULL

AND p.exchange IN ('SHZ', 'SHH')

),

sector_medians AS (

SELECT exchange, sector,

PERCENTILE_CONT(0.5) WITHIN GROUP (ORDER BY ev_ebitda) AS median_ev_ebitda,

COUNT(*) AS n_sector_stocks

FROM universe GROUP BY exchange, sector HAVING COUNT(*) >= 5

)

SELECT u.symbol, u.companyName, u.exchange, u.sector,

ROUND(u.ev_ebitda, 2) AS ev_ebitda_ttm,

ROUND(sm.median_ev_ebitda, 2) AS sector_median_ev_ebitda,

ROUND(u.ev_ebitda / sm.median_ev_ebitda, 3) AS ev_ratio_to_sector,

ROUND((1 - u.ev_ebitda / sm.median_ev_ebitda) * 100, 1) AS discount_pct,

ROUND(u.roe * 100, 1) AS roe_pct,

ROUND(u.de, 2) AS debt_to_equity,

ROUND(u.marketCap / 1e9, 2) AS mktcap_b

FROM universe u JOIN sector_medians sm ON u.exchange = sm.exchange AND u.sector = sm.sector

WHERE u.ev_ebitda / sm.median_ev_ebitda < 0.70

ORDER BY u.ev_ebitda / sm.median_ev_ebitda ASC LIMIT 30

Run this screen on Ceta Research

What We Found

25 years. Never in cash. Still trails SPY by 3.66% annually.

| Metric | EV/EBITDA Sector-Relative (China) | S&P 500 |

|---|---|---|

| CAGR | 3.98% | 7.64% |

| Total Return | 165.5% | 530.71% |

| Sharpe Ratio | 0.035 | 0.322 |

| Sortino Ratio | 0.076 | 0.556 |

| Calmar Ratio | 0.062 | - |

| Max Drawdown | -64.54% | -34.90% |

| Up Capture | 110.46% | 100% |

| Down Capture | 77.74% | 100% |

| Win Rate vs SPY | 36% | - |

| Avg Stocks per Year | 22.8 | - |

| Cash Periods | 0 of 25 | - |

A Sharpe ratio of 0.035 means the strategy barely earned anything above the risk-free rate per unit of volatility over 25 years. The max drawdown of -64.54% is the worst of any exchange tested. The strategy beat SPY in only 36% of individual years.

The zero cash periods look like a feature. In practice, they mean the portfolio was fully deployed into the 2008 crash (-64.5%) and the 2011 selloff (-37.8%) with no option to step aside.

The bubble years explain everything

The backtest includes two Chinese bubble periods that dominate the summary statistics:

- 2007: +111.4% (Shanghai Composite hit 6,100 in October 2007)

- 2009: +102.8% (post-crisis liquidity surge)

These aren't alpha. They're participation in a speculative bubble and its government-fueled recovery. The sector-relative signal happened to be invested during both, which inflates the 25-year CAGR significantly. Without those two years, the compound return would be deeply negative.

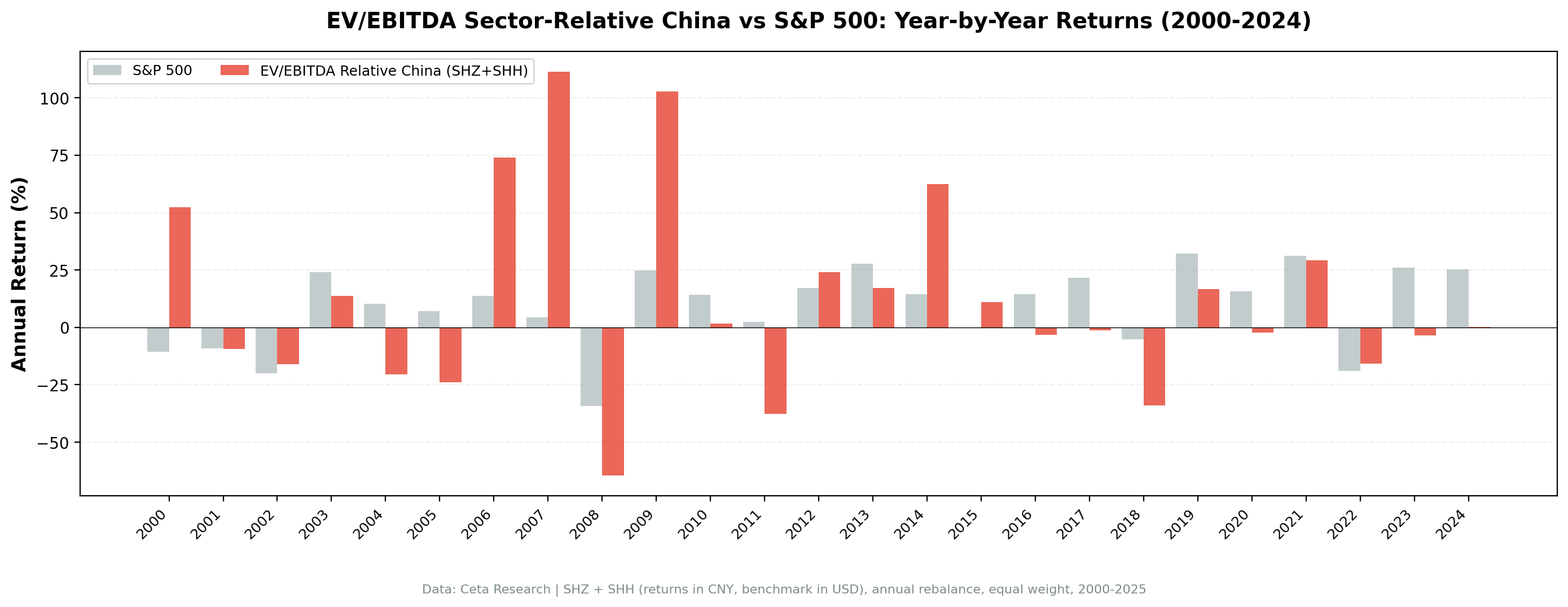

Year-by-year returns

| Year | Strategy | S&P 500 | Excess |

|---|---|---|---|

| 2000 | +52.3% | -10.5% | +62.8% |

| 2001 | -9.5% | -9.2% | -0.3% |

| 2002 | -16.1% | -19.9% | +3.9% |

| 2003 | +13.8% | +24.1% | -10.4% |

| 2004 | -20.5% | +10.2% | -30.8% |

| 2005 | -23.9% | +7.2% | -31.1% |

| 2006 | +74.0% | +13.7% | +60.4% |

| 2007 | +111.4% | +4.4% | +107.0% |

| 2008 | -64.5% | -34.3% | -30.2% |

| 2009 | +102.8% | +24.7% | +78.1% |

| 2010 | +1.7% | +14.3% | -12.6% |

| 2011 | -37.8% | +2.5% | -40.3% |

| 2012 | +24.0% | +17.1% | +6.9% |

| 2013 | +17.2% | +27.8% | -10.6% |

| 2014 | +62.4% | +14.5% | +47.9% |

| 2015 | +11.1% | -0.1% | +11.2% |

| 2016 | -3.3% | +14.4% | -17.7% |

| 2017 | -1.3% | +21.6% | -22.9% |

| 2018 | -34.0% | -5.2% | -28.8% |

| 2019 | +16.8% | +32.3% | -15.6% |

| 2020 | -2.1% | +15.6% | -17.8% |

| 2021 | +29.3% | +31.3% | -1.9% |

| 2022 | -15.7% | -19.0% | +3.3% |

| 2023 | -3.5% | +26.0% | -29.5% |

| 2024 | +0.2% | +25.3% | -25.1% |

Why the signal can't help you in China

The A-share market is structurally different from Western exchanges in three ways that matter for a value signal:

Policy cycles, not fundamentals, drive prices. The 2006-2007 surge to +186% and the 2008 crash to -65% were driven by Beijing's credit tap, not by sector-relative valuation. Stocks trading at EV/EBITDA discounts to their sector peers participated in the bubble on the way up and the crash on the way down. The signal provided no discrimination.

Retail dominance over institutional pricing. China's A-share market has historically had retail investor participation rates of 80%+ by trading volume. Retail investors don't price stocks on EV/EBITDA sector comparisons. They follow momentum, sentiment, and government signals. A cheap stock can stay cheap indefinitely because the marginal buyer isn't looking at it.

State-directed industries with controlled pricing. Large state-owned enterprises in banking, energy, and utilities are priced partly on policy mandates. A bank trading at a 40% discount to its sector peers might stay there because market participants understand it will face government-directed lending that constrains its ROE. The "discount" is rational, not anomalous.

2011 and 2018: the painful down years

Beyond 2008, two other years stand out for severity:

- 2011: -37.8% vs SPY +2.5% (-40.3% excess). The European debt crisis triggered capital outflows from emerging markets. Chinese property concerns added domestic pressure.

- 2018: -34.0% vs SPY -5.2% (-28.8% excess). US-China trade war escalation hit export-oriented companies across multiple sectors.

These were macro events that sector-relative EV/EBITDA screening couldn't anticipate or protect against.

The recent years (2016-2024): structural deterioration

Nine of the last ten years produced negative or near-zero excess returns. The -29.5% excess in 2023 and -25.1% in 2024 reflect US tech outperformance combined with China's property sector slowdown, regulatory crackdowns on tech companies, and persistent delisting/geopolitical risk premiums.

The A-share market's valuation compression since 2021 has created many stocks that look cheap on EV/EBITDA metrics. But the signal can't tell you whether those discounts reflect genuine mispricing or a rational reassessment of growth expectations and risk premiums.

Backtest Methodology

Full methodology: backtests/METHODOLOGY.md

| Parameter | Choice |

|---|---|

| Universe | SHZ + SHH, MCap > ¥2B |

| Signal | EV/EBITDA < 70% of sector median, range 0.5-25x |

| Quality | ROE > 8%, D/E < 2.0 |

| Portfolio | Top 30 by deepest discount, equal weight |

| Rebalancing | Annual (January) |

| Cash rule | Hold cash if < 10 qualify |

| Benchmark | S&P 500 Total Return (SPY, USD) |

| Period | 2000-2025 (25 years) |

| Data | Point-in-time (45-day lag on FY financial statements) |

| Transaction costs | 0.1% one-way (size-tiered by market cap) |

Limitations

Bubble years distort the CAGR. Remove 2007 (+111%) and 2009 (+102%), and the 25-year compound return is sharply negative. The positive CAGR figure depends on two years of market-wide speculation that the signal didn't cause.

Data quality. FMP's Chinese data is less complete than US or European data, particularly for earlier years. Financial statement quality and disclosure standards for Chinese-listed companies are lower than for Western issuers.

MaxDD -64.54%. The worst max drawdown of 13 exchanges tested. A portfolio starting at $10,000 would have dropped to approximately $3,550 at the trough. Recovery from that depth requires a +81% return to break even.

Currency effects. Returns are in CNY. The benchmark (SPY) is in USD. CNY/USD fluctuations add noise to the comparison.

Delisting and VIE risk. The backtest uses current exchange profiles. Historical delistings and companies that exited the market are not fully tracked. This creates survivorship bias that slightly flatters the results.

Conclusion

Sector-relative EV/EBITDA on China A-shares generated 3.98% CAGR over 25 years, lagging SPY by 3.66% annually. The max drawdown of -64.54% is the highest in this study. The strategy beat SPY in only 36% of individual years.

The problem isn't the data or the signal construction. It's the market itself. China's A-share market prices stocks on policy expectations, retail momentum, and regulatory signals. Sector-relative EV/EBITDA discounts exist consistently, but they don't close on market logic. They close when Beijing opens the credit tap.

We're including this result because it's useful to understand where sector-relative value breaks down. The discipline of running the same strategy across all markets and reporting every result, including the failures, is how you learn where the signal's underlying assumptions hold.

Data: Ceta Research (FMP financial data warehouse). Returns in CNY (local currency). Benchmark S&P 500 in USD. Past performance does not guarantee future results. See full methodology at github.com/ceta-research/backtests.