Earnings Surprise Drift in China: The Market That Beats the Least but

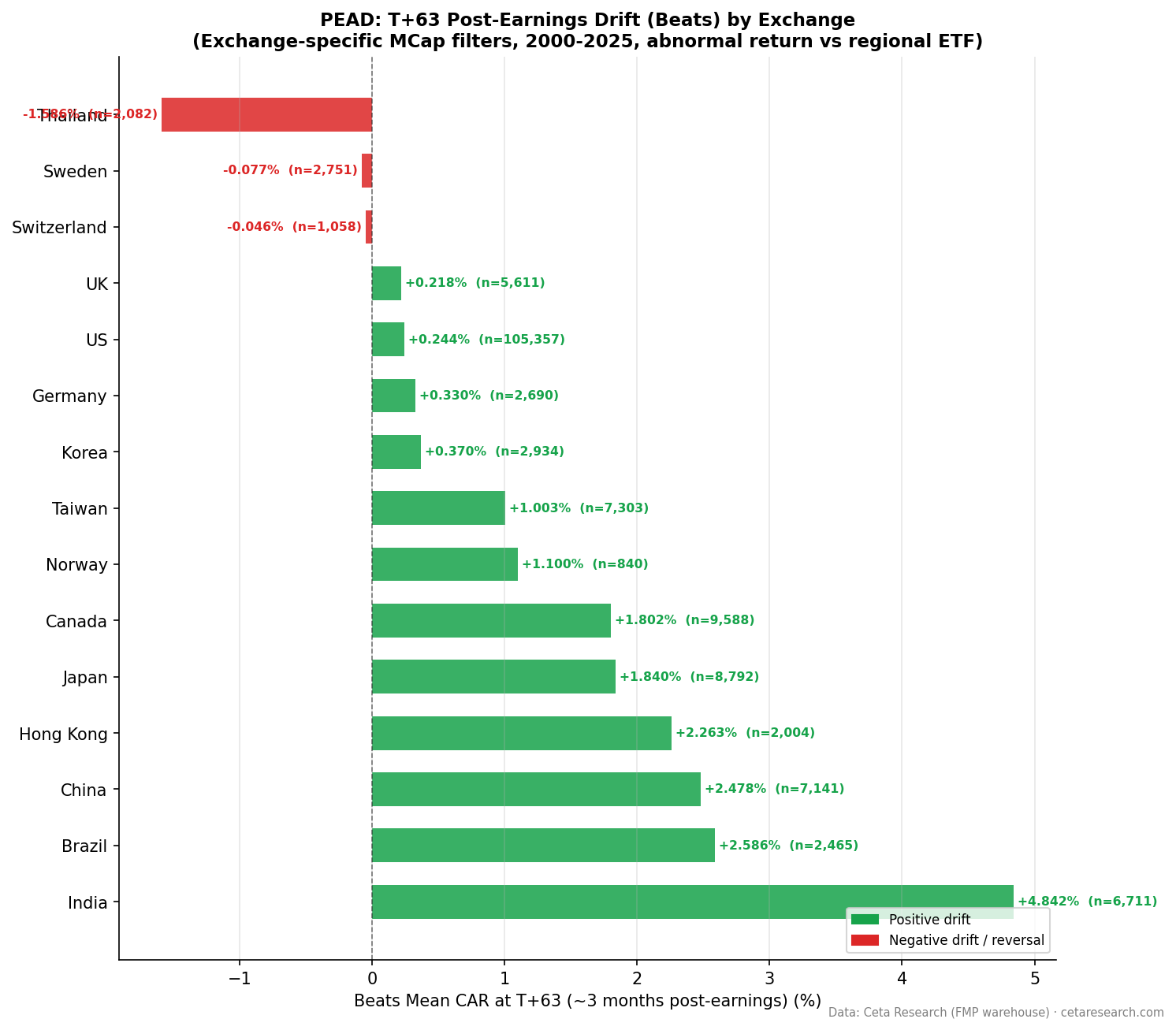

China has the lowest beat rate of any exchange in our global study: just 34.6% of earnings announcements come in above analyst estimates. Two-thirds of Chinese companies miss. Despite this, when they do beat, the drift is real and sustained. Positive surprises produce +2.48% CAR at T+63. The top quintile reaches +3.43%. The miss side, by contrast, barely drifts at all (-0.08% at T+63). China is a one-sided PEAD market: follow the beats, ignore the misses.

Contents

- Method

- The Strategy

- What We Found

- Positive vs Negative Surprise Drift

- Quintile Analysis at T+63

- Why China's Beat Rate Is So Low

- The Miss-Side Structure

- When It Works and When It Struggles

- Run It Yourself

- Limitations

- Part of a Series

- References

Method

| Parameter | Details |

|---|---|

| Data source | FMP earnings_surprises + stock_eod (Ceta Research warehouse) |

| Universe | SHZ + SHH (China A-shares) — market cap threshold applied per exchange |

| Period | 2000–2025 (26 years) |

| Events | 20,667 total (deduplicated per symbol/date) |

| Benchmark | Equal-weighted SHZ+SHH market return |

| Surprise metric | (epsActual − epsEstimated) / ABS(epsEstimated) |

| Windows | T+1, T+5, T+21, T+63 trading days |

The Strategy

Post-Earnings Announcement Drift (PEAD) documents that stocks continue drifting in the direction of their earnings surprise for weeks after announcement. Ball and Brown (1968) first established this. Bernard and Thomas (1989) confirmed the drift persists up to 60 trading days. The standard explanation is behavioral: markets underreact to earnings news on announcement day.

China A-shares present a distinctive test case. The market is retail-dominated, has shorter average analyst coverage history, and operates under different disclosure norms than Western markets. We ran the same event study framework on 20,667 Chinese earnings announcements to see how these structural differences affect PEAD.

What We Found

Positive vs Negative Surprise Drift

| Direction | Events | Beat% | T+1 | T+5 | T+21 | T+63 |

|---|---|---|---|---|---|---|

| Positive surprises | 7,141 | 34.6% | +0.97% | +1.52% | +1.23% | +2.48% |

| Negative surprises | 13,526 | 65.4% | -0.27% | -0.12% | -0.22% | -0.08% |

The contrast is stark. Positive surprises build steadily through all four windows, peaking at +2.48% by T+63. Negative surprises do almost nothing. The -0.27% at T+1 is the sharpest reaction on the miss side, and even that fades toward zero by T+63 (-0.08%).

This pattern is the inverse of what we see in the UK, where misses drive the spread and beats barely drift. In China, bad news is priced in rapidly or simply absorbed without sustained drift.

Quintile Analysis at T+63

| Quintile | Description | Events | CAR T+63 | t-stat | Hit Rate |

|---|---|---|---|---|---|

| Q5 | Biggest beats | 3,791 | +3.43% | +9.6 | 51.6% |

| Q4 | Moderate beats | — | +1.34% | — | — |

| Q3 | Near-consensus | — | +0.71% | — | — |

| Q2 | Moderate misses | — | -0.11% | — | — |

| Q1 | Worst misses | 3,745 | -1.33% | -3.6 | 40.5% |

The Q5-Q1 spread is +4.76% at T+63. Q5 is statistically robust (t=9.6). Q1's -1.33% with a t-stat of -3.6 is significant but modest. The entire distribution skews toward positive drift, even Q3 (near-consensus events) produces +0.71% at T+63.

The hit rate for Q5 (51.6%) means slightly more than half of Chinese earnings beats produce positive CAR at T+63. It's not a clean majority, but across nearly 4,000 events the statistical signal is clear.

Why China's Beat Rate Is So Low

China's 34.6% beat rate is the lowest across all 14 exchanges. Several factors likely contribute. Analyst coverage of A-shares has historically been optimistic, creating high baseline estimates that are difficult to clear. State-owned enterprise reporting norms differ from private companies. The proportion of companies with genuine consensus estimates (rather than single-analyst estimates) is also lower in the early years of our sample.

The low beat rate has a practical implication: the positive surprise events in China are genuine beats against meaningful consensus, not the routine conservative-guidance beats common in the US. This may explain why Chinese beats drift more strongly (+2.48% vs +0.24% for US positive surprises).

The Miss-Side Structure

Chinese negative surprises don't drift in the traditional PEAD direction. This is notable. One interpretation: China's retail-dominated market structure means negative news gets priced in on announcement day or shortly after. Chinese retail investors are fast to react to bad news but slower to fully price in positive news. This creates the asymmetric pattern we observe.

Another factor: many Chinese A-share companies with negative surprises operate in sectors with implicit government support. Investors may discount earnings misses partly because of perceived downside protection, suppressing the miss-side drift.

When It Works and When It Struggles

China's PEAD is a long-only signal. Shorting Q1 misses is unlikely to produce consistent returns given the -1.33% at T+63 and the large number of events required. The Q5 drift is where the actionable edge lives.

The drift for Chinese beats builds over time. T+1 is +0.97%, T+5 is +1.52%, and T+63 is +2.48%. This suggests a wider capture window than markets where the drift concentrates in the first week. Execution doesn't need to be immediate.

China A-shares have daily price limits (±10% for most stocks, ±20% for newly listed stocks). This can smooth the T+1 reaction and spread the price adjustment over multiple days, which may contribute to the gradual drift pattern.

Run It Yourself

python3 earnings-surprise/screen.py --preset china

-- Recent large positive earnings surprises on China A-shares

WITH deduped AS (

SELECT

es.symbol,

es.date,

es.epsActual,

es.epsEstimated,

(es.epsActual - es.epsEstimated) / NULLIF(ABS(es.epsEstimated), 0) AS std_surprise,

ROW_NUMBER() OVER (PARTITION BY es.symbol, es.date ORDER BY es.lastUpdated DESC) AS rn

FROM earnings_surprises es

JOIN profile p ON es.symbol = p.symbol

WHERE p.exchange IN ('SHZ', 'SHH')

AND p.isActivelyTrading = true

AND es.date >= CURRENT_DATE - INTERVAL '90 days'

AND ABS(es.epsEstimated) > 0.01

)

SELECT

symbol,

date,

epsActual,

epsEstimated,

ROUND(std_surprise * 100, 1) AS surprise_pct

FROM deduped

WHERE rn = 1

AND std_surprise > 0.10

ORDER BY date DESC, std_surprise DESC

LIMIT 50

Run this query on Ceta Research →

Limitations

20,667 events is the second-largest sample in our global study (after the US at 170,115). But the beat side is much smaller than the miss side: 7,141 positive events vs 13,526 negative events. Q5 results are based on roughly 3,800 events, which is adequate but thinner than comparable quintiles in larger markets.

Analyst coverage quality for Chinese A-shares has improved since 2005. The early years of our sample (2000–2004) have sparse consensus data, and the EPS estimates in those years may be single-analyst rather than true consensus. This creates more noise in the standardized surprise metric for earlier periods.

Disclosure timing in China doesn't always align with calendar year-end reporting. Many Chinese companies report on a fiscal calendar that differs from the calendar year, which creates variation in event clustering.

Part of a Series

- PEAD Across 14 Global Exchanges: The Drift Is Universal

- Earnings Surprise Drift on US Stocks: 170,000 Events, 26 Years

References

- Ball, R. & Brown, P. (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research.

- Bernard, V. & Thomas, J. (1989). Post-earnings-announcement drift: Delayed price response or risk premium? Journal of Accounting Research.

- Foster, G., Olsen, C. & Shevlin, T. (1984). Earnings releases, anomalies, and the behavior of security returns. The Accounting Review.

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research, FMP financial data warehouse