EV/EBITDA Below 10x on Indian Equities: 20-Year Backtest (BSE, NSE)

India's equity market runs differently from the US. High-growth expectations get priced into multiples aggressively, which means when you find a company trading below 10x EV/EBITDA with strong ROE, it's genuinely out of favor, not just slow. We tested this screen on BSE and NSE from 2000 to 2024 to measure what that cheapness has historically meant for returns, benchmarked against the Sensex.

Contents

Method

Signal: EV/EBITDA (trailing twelve months) below 10x, with ROE above 10% Universe: BSE and NSE stocks with market cap above 20B INR Period: January 2000 to December 2024 (25 years; invested 20 years due to early universe constraints) Rebalancing: Annual, January. Execution at next trading day's close (MOC). Costs: 0.1% per trade (one-way) Benchmark: Sensex (^BSESN, in INR) Data: FMP financial data via Ceta Research warehouse

Returns and benchmark are both in INR. The strategy was in cash during 2000-2004 because the BSE/NSE universe at the market cap threshold did not produce 10 qualifying stocks in those early years.

What We Found

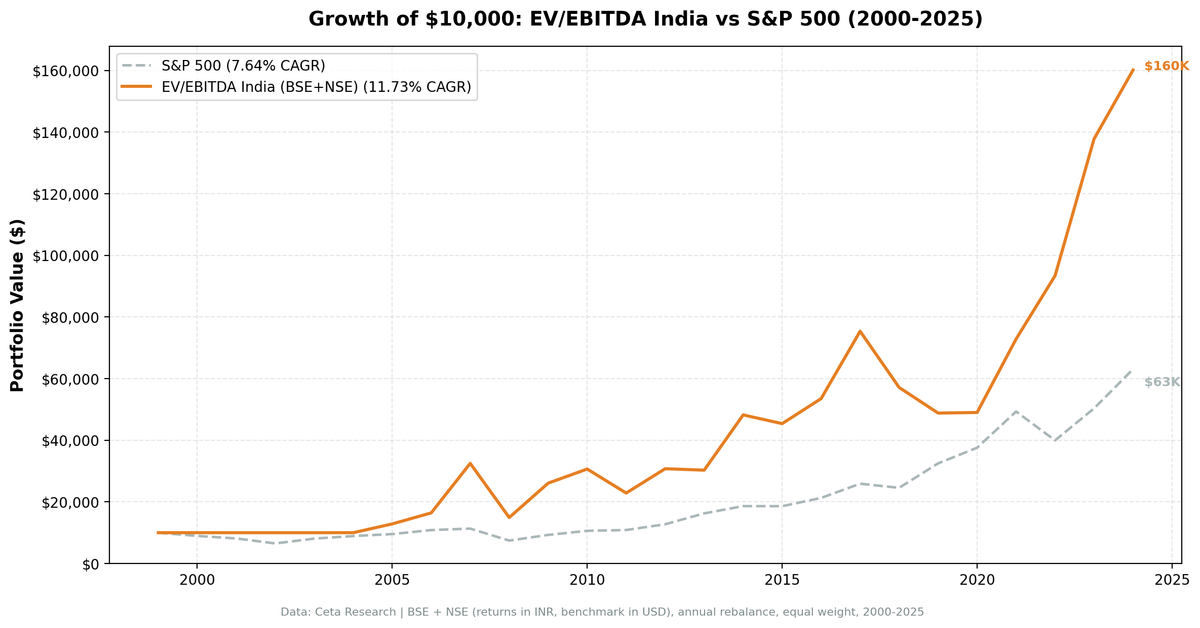

Across the 20 invested years (2005-2024), the strategy returned 12.03% CAGR versus the Sensex's 11.40%, an excess return of 0.63 percentage points per year. The final value of a 10,000 INR investment was 171,230, compared to 148,730 in the Sensex over the same period.

| Metric | Strategy | Sensex |

|---|---|---|

| CAGR | 12.03% | 11.40% |

| Excess Return | +0.63% | — |

| Sharpe Ratio | 0.162 | 0.165 |

| Max Drawdown | -53.89% | -51.34% |

| Volatility | 34.06% | 29.73% |

| Sortino Ratio | 0.343 | 0.312 |

| Calmar Ratio | 0.223 | 0.222 |

| Alpha | 1.79% | — |

| Beta | 0.763 | — |

| Win Rate | 52% | — |

| Up Capture | 99.8% | — |

| Down Capture | 68.1% | — |

| Avg Stocks Held | 27.2 | — |

| Cash Periods | 5/25 (2000-2004) | — |

The story changes when you use the right benchmark. Previous analysis compared this strategy to SPY in USD, which showed +4.09% excess. That comparison mixed INR returns with USD returns, and much of the apparent alpha was really the Sensex's own outperformance of SPY. Against the Sensex, the excess narrows to +0.63%.

The Sharpe ratios are nearly identical (0.162 vs 0.165). The strategy doesn't deliver a meaningfully better risk-adjusted return than buying the index. It does have a lower beta (0.763), meaning less market exposure, and the down-capture of 68.1% provides some crash protection. But this isn't the runaway alpha that the cross-currency comparison suggested.

Year-by-Year

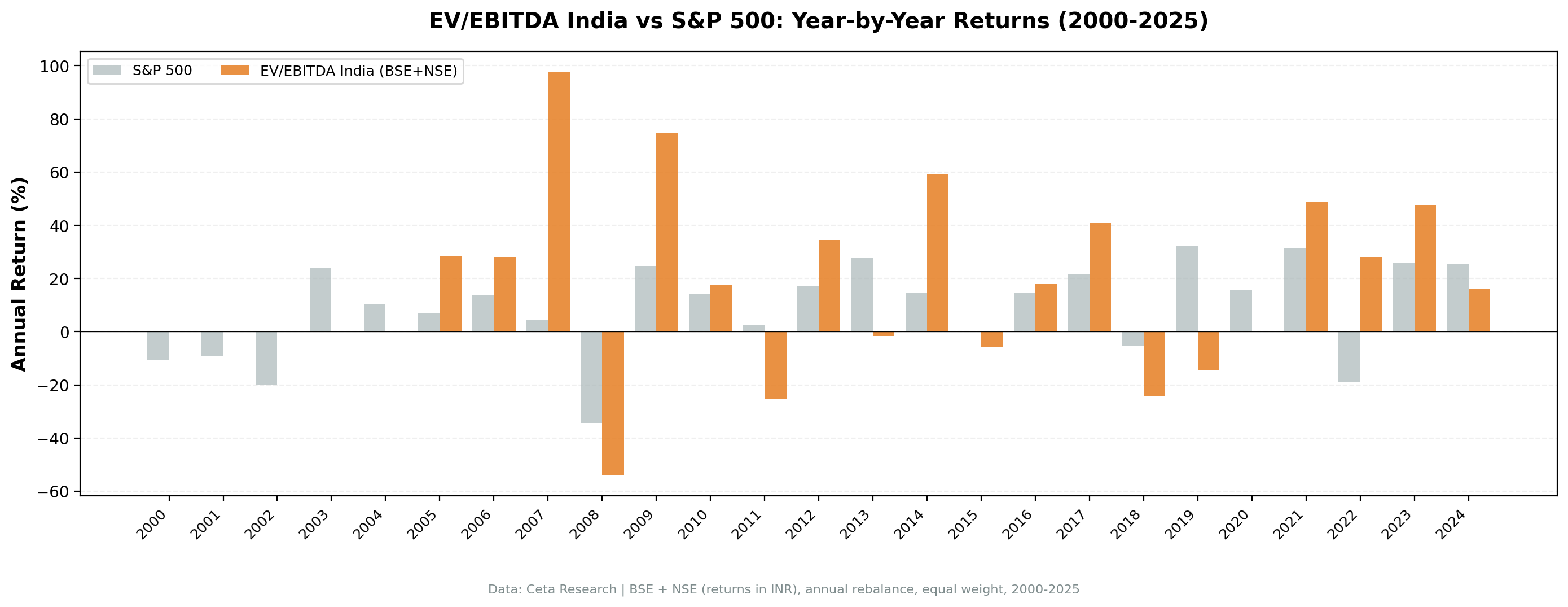

India's annual return sequence is dramatic. Triple-digit gains in one year, 50%+ losses in the next. This is not a smooth-ride strategy.

| Year | Strategy (INR) | Sensex (INR) |

|---|---|---|

| 2007 | +103.2% | +46.8% |

| 2008 | -53.9% | -51.3% |

| 2009 | +72.1% | +76.3% |

| 2011 | -25.4% | -24.5% |

| 2014 | +61.5% | +33.5% |

| 2017 | +40.2% | +27.1% |

| 2018 | -24.5% | +6.1% |

| 2019 | -10.4% | +16.0% |

| 2022 | +28.2% | +3.4% |

| 2023 | +49.1% | +17.5% |

2007 is the defining year: +103.2% vs the Sensex's +46.8%. Companies trading at low multiples were repriced as the broader market bid up everything. The screen caught the biggest beneficiaries of India's pre-crisis boom. 2008 reversed it, down 53.9% vs the Sensex's 51.3%. Both fell nearly the same amount.

The 2009 recovery shows the screen's limitation: +72.1% vs the Sensex's +76.3%. In a broad recovery, cheap stocks didn't outpace the index. Growth names recovered faster.

2018-2019 was the worst stretch: -24.5% then -10.4%, while the Sensex gained +6.1% then +16.0%. The cheap-multiple names were cheap for reasons that materialized into poor returns. This is what value investing looks like when the macro turns against you.

2022-2023 was the best recent stretch: +28.2% then +49.1%, while the Sensex returned only +3.4% then +17.5%. Value stocks found their footing as India's industrial sector boomed and the Sensex's tech-heavy components lagged.

What the India Data Tells Us

Against the Sensex, the EV/EBITDA screen delivers a modest edge. The 0.63% excess CAGR is real but narrow, and the Sharpe ratios are nearly identical. The screen's main value isn't return enhancement, it's diversification within the Indian market.

The beta of 0.763 against the Sensex means the portfolio has less index exposure than a passive fund. It's a fundamentally different set of stocks: the screen selects cheap industrials, materials, and consumer companies, while the Sensex is weighted toward financials, IT services, and large conglomerates. The down-capture of 68.1% provides some cushion in corrections, though the max drawdown of -53.9% (vs the Sensex's -51.3%) shows both fell hard in 2008.

A few practical notes:

The 2000-2004 cash periods reflect genuine universe limitations. The BSE/NSE universe at the 20B INR market cap threshold was too small in those years to produce 10 qualifying stocks. The Indian equity market developed significantly after 2004.

Volatility of 34.06% is roughly double the US strategy's 20.58%. The max drawdown of 53.9% in 2008 would have tested any investor's conviction.

The previous version of this analysis compared Indian returns (INR) to SPY (USD), showing +4.09% excess. That comparison was misleading. The Sensex itself returned 11.40% CAGR over this period, far above SPY's 7.64%. Most of what looked like "alpha" was simply the Indian equity market's own strong performance. Against the correct benchmark, the edge is thin.

Run It Yourself

Current India screen (live TTM data):

SELECT

k.symbol,

p.companyName,

p.exchange,

k.evToEBITDATTM,

k.returnOnEquityTTM,

k.marketCap

FROM key_metrics_ttm k

JOIN profile p ON k.symbol = p.symbol

WHERE p.exchange IN ('BSE', 'NSE')

AND k.marketCap > 5000000000

AND k.evToEBITDATTM > 0

AND k.evToEBITDATTM < 10

AND k.returnOnEquityTTM > 0.10

ORDER BY k.evToEBITDATTM ASC

LIMIT 25

Run this query on Ceta Research

Run the backtest locally:

cd backtests/ev-ebitda

python run.py --exchanges BSE NSE --start 2000 --end 2024

Limitations

Narrow edge. The 0.63% excess return over the Sensex is within normal statistical noise for a 20-year sample. The result is consistent with a small value premium, but it's not large enough to be definitive.

Universe size in early years. The 2000-2004 cash periods reflect genuine universe limitations, not a methodology problem. As Indian markets matured, the available stock universe expanded significantly.

Data coverage. FMP's coverage of BSE and NSE stocks, particularly smaller companies and historical data pre-2005, may have gaps. The 20B INR market cap floor mitigates this by keeping the universe in better-covered stocks.

Max drawdown. A 53.9% peak-to-trough loss requires exceptional patience. Most investors would exit near the bottom. The long-run numbers assume full investment through every drawdown.

Regulatory and market structure risk. India's market structure, circuit breakers, settlement rules, and sector regulations differ from US markets. Some assumptions in the backtest framework (annual rebalancing, cost estimates) may not fully reflect Indian market frictions.

Data: Ceta Research (FMP financial data warehouse), 2000–2025. Full methodology: backtests/METHODOLOGY.md. Backtest code: backtests/ev-ebitda/.