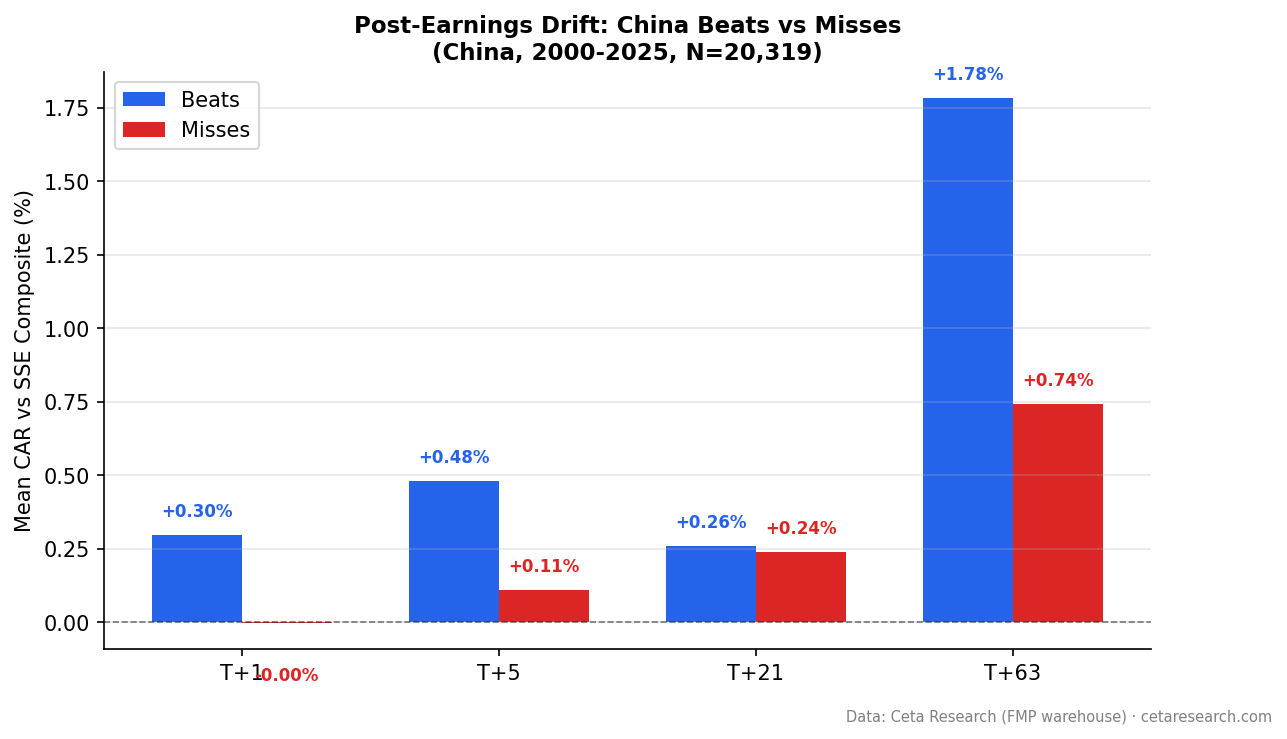

Post-Earnings Drift in China: Everything Drifts Up on A-Shares

20,319 earnings events across Shenzhen and Shanghai (2000-2025). Beats drift +1.78% vs SSE Composite at T+63 (t=+8.18). Misses drift +0.74% (t=+4.67, also significant). Both sides positive. Q5-Q1 spread: +2.03pp. Next-day close entry.

China's PEAD pattern is unusual. Both beats and misses drift positive against the SSE Composite. The entire market of earnings-covered stocks outperforms the index, with beats outperforming more.

Contents

- The Strategy

- What We Found

- Why Everything Drifts Up

- China vs the Global Pattern

- Limitations

- Takeaway

- References

We ran 20,319 earnings events across Shenzhen (SHZ) and Shanghai (SHH) exchanges from 2000 to 2025 using next-day close (MOC) entry and the SSE Composite as benchmark. Beats drifted +1.78% over 63 trading days (t=+8.18). Misses drifted +0.74% (t=+4.67). Both are statistically significant.

The beat-vs-miss gradient still works: beats outperform misses by about 1 percentage point at T+63. But the old story of "misses don't move" was an artifact of using FXI as benchmark. With a local index, misses drift positive too.

The Strategy

Post-Earnings Announcement Drift (PEAD) is an event study. We measure cumulative abnormal returns in the days and weeks after an earnings surprise, not a portfolio.

The signal: Surprise = (epsActual - epsEstimated) / |epsEstimated|

Parameters:

- Universe: SHZ + SHH (Shenzhen + Shanghai), market cap > ¥2B RMB (historical FY)

- Period: 2000-2025 (20,319 events: 7,009 beats, 13,310 misses)

- Benchmark: SSE Composite (000001.SS)

- Execution: Next-day close (market-on-close)

- Surprise cap: |surprise| <= 200%

- Winsorized means: 1st/99th percentile

- Event windows: T+1, T+5, T+21, T+63 trading days

Data: Ceta Research (FMP financial data warehouse), earnings_surprises table.

Screen for current earnings surprises on Chinese A-shares:

SELECT es.symbol,

CAST(es.date AS DATE) AS event_date,

es.epsActual AS actual_eps,

es.epsEstimated AS est_eps,

ROUND((es.epsActual - es.epsEstimated)

/ ABS(NULLIF(es.epsEstimated, 0)) * 100, 1) AS surprise_pct

FROM earnings_surprises es

JOIN profile p ON es.symbol = p.symbol

WHERE CAST(es.date AS DATE) >= CURRENT_DATE - INTERVAL '30' DAY

AND es.epsEstimated IS NOT NULL

AND ABS(es.epsEstimated) > 0.01

AND es.epsActual > es.epsEstimated

AND p.exchange IN ('SHZ', 'SHH')

ORDER BY surprise_pct DESC

LIMIT 30

What We Found

Both sides drift positive. Beats drift more.

| Category | T+63 | t-stat | Significant? |

|---|---|---|---|

| Beats (7,009 events) | +1.78% | +8.18 | Yes |

| Misses (13,310 events) | +0.74% | +4.67 | Yes |

Beats drift upward and keep drifting. The +1.78% abnormal return at T+63 is highly significant (t=+8.18).

Misses also drift positive. The +0.74% at T+63 is significant (t=+4.67). This is a major change from our earlier FXI-benchmarked analysis, which showed misses flat at -0.04%. The difference is entirely benchmark-driven: FXI (a USD-traded ETF) was a poor proxy for A-share returns. Against the SSE Composite, stocks with analyst coverage outperform the broad index regardless of whether they beat or miss.

One more thing to notice: 65.5% of the 20,319 events are misses. Chinese companies beat analyst estimates less than 35% of the time. That's the inverse of the US market, where beat rates have climbed to ~65%. Despite being the majority of events, misses still drift positive. This suggests that having analyst coverage itself is a positive selection filter in the A-share market.

The quintile breakdown confirms the gradient.

| Quintile | CAR at T+63 |

|---|---|

| Q1 (worst misses) | +0.49% |

| Q2 | +0.40% |

| Q3 | +1.05% |

| Q4 | +1.01% |

| Q5 (biggest beats) | +2.52% |

The Q5-Q1 spread is +2.03 percentage points. Every quintile is positive. Even Q1 (worst misses) drifts +0.49% vs the SSE Composite. The surprise gradient still works: Q5 at +2.52% is the clear winner, and Q1 is the weakest. But "weakest" here means slightly positive, not negative.

The middle quintiles are noisy (Q3 slightly above Q4), but the extremes tell the story: bigger beats produce more drift, and even the worst misses don't underperform the index.

Why Everything Drifts Up

The pattern where all quintiles drift positive against the SSE Composite reflects structural features of China's A-share market.

Analyst coverage as a quality filter. The SSE Composite includes thousands of stocks, many with no analyst coverage at all. The subset of companies that have earnings estimates is inherently higher quality: larger, more liquid, more institutionally held. When you benchmark this subset against the full index, positive drift is expected. The +0.74% miss drift may not be PEAD at all. It may be a coverage premium.

Retail-dominated trading. A-share investors are predominantly retail. Institutional penetration, while growing, remains lower than in developed markets. Retail-heavy markets tend to be optimism-biased: investors buy aggressively on positive surprises but react inconsistently to bad news. This helps explain why beats drift more than misses, even though both sides are positive.

State-owned enterprise earnings management. A significant portion of Chinese listed companies are partially or majority state-owned. SOEs have strong incentives to manage reported earnings, often smoothing results over time. Analyst estimates for SOEs carry unusual uncertainty, making the "miss" label less meaningful.

Short-sale constraints. A-share shorting is severely restricted. Securities lending is limited, margin rules are tight, and many stocks have no borrowable shares at all. In developed markets, miss drift is partly sustained by short sellers building positions after a negative surprise. In China, that mechanism barely exists. This contributes to the absence of negative drift even for the worst misses.

China vs the Global Pattern

| Market | Beats T+63 | Misses T+63 | Pattern |

|---|---|---|---|

| India | +2.89% | -2.28% | Both sides significant |

| China | +1.78% | +0.74% | Both positive (coverage premium?) |

| Canada | +1.13% | -0.34% (not sig.) | Beat side only |

| US | -0.40% | -1.96% | Miss side dominates |

| Japan | -0.26% | -1.38% | Miss side dominates |

China is unusual because both beats and misses drift positive. No other market shows this pattern. The likely explanation is that analyst-covered A-shares systematically outperform the SSE Composite, and the beat/miss gradient sits on top of that base effect.

For practical purposes, the Q5-Q1 spread of +2.03pp still means beats outperform misses. But you can't capture the miss side as a short signal. Everything drifts up.

Limitations

Benchmark and coverage premium. We use the SSE Composite (000001.SS) as benchmark, which is a better local match than FXI or MCHI. However, the positive drift across all quintiles raises the question of whether we're measuring PEAD or simply a coverage premium (analyst-covered stocks outperforming the broad index). The Q5-Q1 gradient is real, but the baseline drift may not be earnings-specific.

Exchange coverage gaps. The dataset covers SHZ and SHH (Shenzhen and Shanghai main boards) but not ChiNext, STAR Market, or B-shares separately. Smaller growth companies on ChiNext may have different PEAD dynamics.

Shorting constraints in analysis. Even though misses drift positive, the relative underperformance of misses vs beats isn't capturable as a short signal. Executing short strategies on A-shares remains operationally difficult for most investors.

Estimate quality. Chinese analyst consensus estimates vary in quality and coverage. The high miss rate (65.5%) likely reflects systematic over-estimation rather than a pattern of company underperformance.

Transaction costs. Gross abnormal returns. A-share bid-ask spreads and stamp duty (0.1% on sells) reduce practical capture.

Takeaway

China's PEAD pattern is positive across the board. Beats drift +1.78% (t=+8.18) and misses drift +0.74% (t=+4.67) at T+63 vs the SSE Composite. The Q5-Q1 spread of +2.03pp shows the surprise gradient still works, but there's no negative drift on the miss side.

The practical signal is beat selection: Q5 at +2.52% outperforms Q1 at +0.49%. If you're building a long-only screen for Chinese A-shares, earnings beats are a stronger positive signal than non-beats. But the absence of any negative drift means the "avoid misses" leg of a traditional PEAD strategy has no value here.

Part of this pattern is likely a coverage premium rather than pure PEAD. Analyst-covered stocks outperform the SSE Composite as a group. The surprise gradient sits on top of that base effect. Whether the beat-vs-miss spread of ~1pp at T+63 justifies the trading costs is the practical question.

Data: Ceta Research (FMP financial data warehouse). 20,319 events, SHZ+SHH (Shenzhen+Shanghai), 2000-2025. Abnormal returns computed vs SSE Composite (000001.SS) benchmark. Next-day close (MOC) entry. 1st/99th percentile winsorization. Surprise cap 200%. Past performance does not guarantee future results. Educational content only, not investment advice.

References

- Ball, R. & Brown, P. (1968). "An Empirical Evaluation of Accounting Income Numbers." Journal of Accounting Research, 6(2), 159-178.

- Bernard, V. & Thomas, J. (1989). "Post-Earnings-Announcement Drift: Delayed Price Response or Risk Premium?" Journal of Accounting Research, 27(Supplement), 1-36.

- Bernard, V. & Thomas, J. (1990). "Evidence that Stock Prices Do Not Fully Reflect the Implications of Current Earnings for Future Earnings." Journal of Accounting and Economics, 13(4), 305-340.