Cyclical Sector Timing in Switzerland: Sharpe 0.415, Precision

Cyclical Sector Timing in Switzerland: Tied for Highest Sharpe Ratio

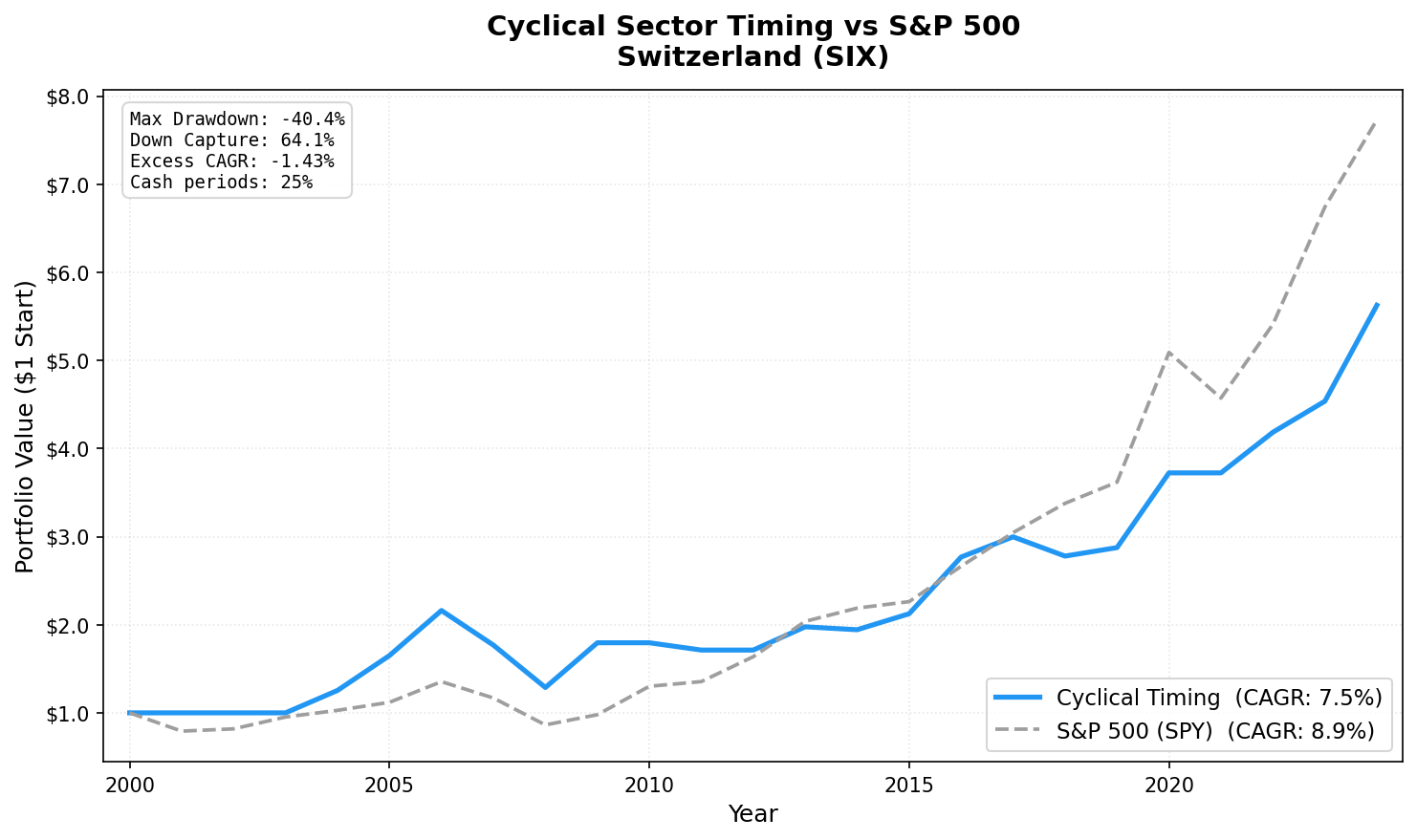

Switzerland tied Germany for the highest Sharpe ratio in the cyclical timing study at 0.415. The CAGR is modest at 7.46% against SPY's 8.89%, but the risk-adjusted profile reflects a consistency that raw returns don't fully capture.

Contents

Swiss precision machinery and specialty chemicals companies (Sulzer, Georg Fischer, Clariant, Sika) operate in narrow niches with global customer bases. Their revenue cycles are driven by industrial capex orders worldwide. When the global industrial cycle expands, these companies show it cleanly in revenue data. When it contracts, they show that too. The expansion signal on SIX is among the most reliable in the study.

The cost: 25% cash rate (6 of 24 periods). The strategy sits out contraction years entirely, which limits the compounding base.

Method

| Parameter | Value |

|---|---|

| Universe | SIX (Swiss Exchange) |

| Sectors | Basic Materials, Industrials, Energy, Consumer Cyclical |

| Signal | ≥ 50% of cyclical stocks with positive YoY FY revenue growth |

| Selection | Top 30 by ROE, among stocks with positive revenue growth AND ROE ≥ 5% |

| Rebalancing | Annual (July) |

| Period | 2001–2024 |

| Cash periods | 6 of 24 (25%) |

| Avg stocks | 18.2 |

| Benchmark | S&P 500 Total Return (SPY) |

Full methodology: backtests/METHODOLOGY.md US flagship blog (methodology + SQL): blog.tradingstudio.finance/cyclical-sector-timing-us-backtest

Results

| Metric | Portfolio | S&P 500 |

|---|---|---|

| CAGR (2001–2024) | 7.46% | 8.89% |

| Excess CAGR | -1.43% | — |

| Max drawdown | -40.42% | -36.27% |

| Sharpe ratio | 0.415 | — |

| Beta | 0.607 | 1.0 |

| Down capture | 64.08% | 100% |

| Up capture | 81.58% | 100% |

| Cash periods | 6 of 24 | — |

| Avg stocks held | 18.2 | — |

The 0.607 Beta is notable. Swiss cyclical stocks move at roughly 60% of the US market's amplitude. When SPY falls 10%, this portfolio historically fell about 6%. The cash periods then add a second layer of protection in confirmed contraction years.

The 18.2 average stocks is the smallest portfolio among dedicated markets. Swiss cyclical universe is compact. This concentration can amplify single-stock effects in either direction.

Key Periods

2009: Post-crisis recovery (+39.4%)

Swiss industrial companies recovered strongly in 2009. The export-focused machinery sector saw orders recover as Asian manufacturing picked back up. +39.4% is the best year in the SIX data.

2016: Political uncertainty year (+30.3%)

Despite broader political uncertainty in Europe, Swiss industrials posted strong revenue growth in 2016. The ROE screen captured the quality operators. +30.3% in a year when many markets struggled.

2024: Recent strength (+24.0%)

Swiss precision machinery benefited from advanced manufacturing demand: semiconductor equipment, medical devices, automation. 2024 was one of the portfolio's stronger recent years.

Full Annual Returns

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2001 | 0.0% (CASH) | -20.8% | — |

| 2002 | 0.0% (CASH) | +3.3% | — |

| 2003 | 0.0% (CASH) | +16.4% | — |

| 2004 | +25.4% | +7.9% | +17.5% |

| 2005 | +31.6% | +8.9% | +22.7% |

| 2006 | +31.0% | +20.9% | +10.1% |

| 2007 | -18.2% | -13.7% | -4.5% |

| 2008 | -27.2% | -26.1% | -1.1% |

| 2009 | +39.4% | +13.4% | +26.0% |

| 2010 | 0.0% (CASH) | +32.9% | — |

| 2011 | -4.6% | +4.1% | -8.7% |

| 2012 | 0.0% (CASH) | +20.9% | — |

| 2013 | +15.4% | +24.5% | -9.1% |

| 2014 | -1.7% | +7.4% | -9.1% |

| 2015 | +9.3% | +3.4% | +5.9% |

| 2016 | +30.3% | +17.7% | +12.6% |

| 2017 | +8.3% | +14.3% | -6.0% |

| 2018 | -7.3% | +10.9% | -18.2% |

| 2019 | +3.5% | +7.1% | -3.6% |

| 2020 | +29.5% | +40.7% | -11.2% |

| 2021 | 0.0% (CASH) | -10.2% | — |

| 2022 | +12.4% | +18.3% | -5.9% |

| 2023 | +8.4% | +24.6% | -16.2% |

| 2024 | +24.0% | +14.7% | +9.3% |

Limitations

Small universe. 18.2 average stocks is the smallest in the dedicated markets. Individual company performance creates more single-stock risk than in larger markets.

Currency. Returns are in CHF. The Swiss franc tends to appreciate in risk-off environments, which helps USD/CHF-adjusted returns but creates complexity for non-CHF investors.

Three early cash years (2001-2003). Thin early FMP SIX coverage means the backtest only starts investing in 2004. The CAGR calculation includes those zero years.

2010 and 2012 both cash. Two of six cash periods fell in the post-2008 recovery. Missing both 2010 (+32.9% SPY) and 2012 (+20.9% SPY) is the primary source of the -1.43% excess deficit.

Data: Ceta Research (FMP financial data warehouse). Universe: SIX cyclical sectors. Period: 2001-2024, annual rebalance (July). Past performance doesn't guarantee future results. This is educational content, not investment advice.