What Happens to Acquirer and Target Stocks After M&A Filings

We ran an event study on 2,064 M&A announcements from 2000-2025. Acquirers gained +0.28% at T+1 (t=3.27) and +0.44% at T+5 (t=2.71). The acquirer curse is not in this data. Target T+63 underperformance is a survivorship artifact, not a prediction.

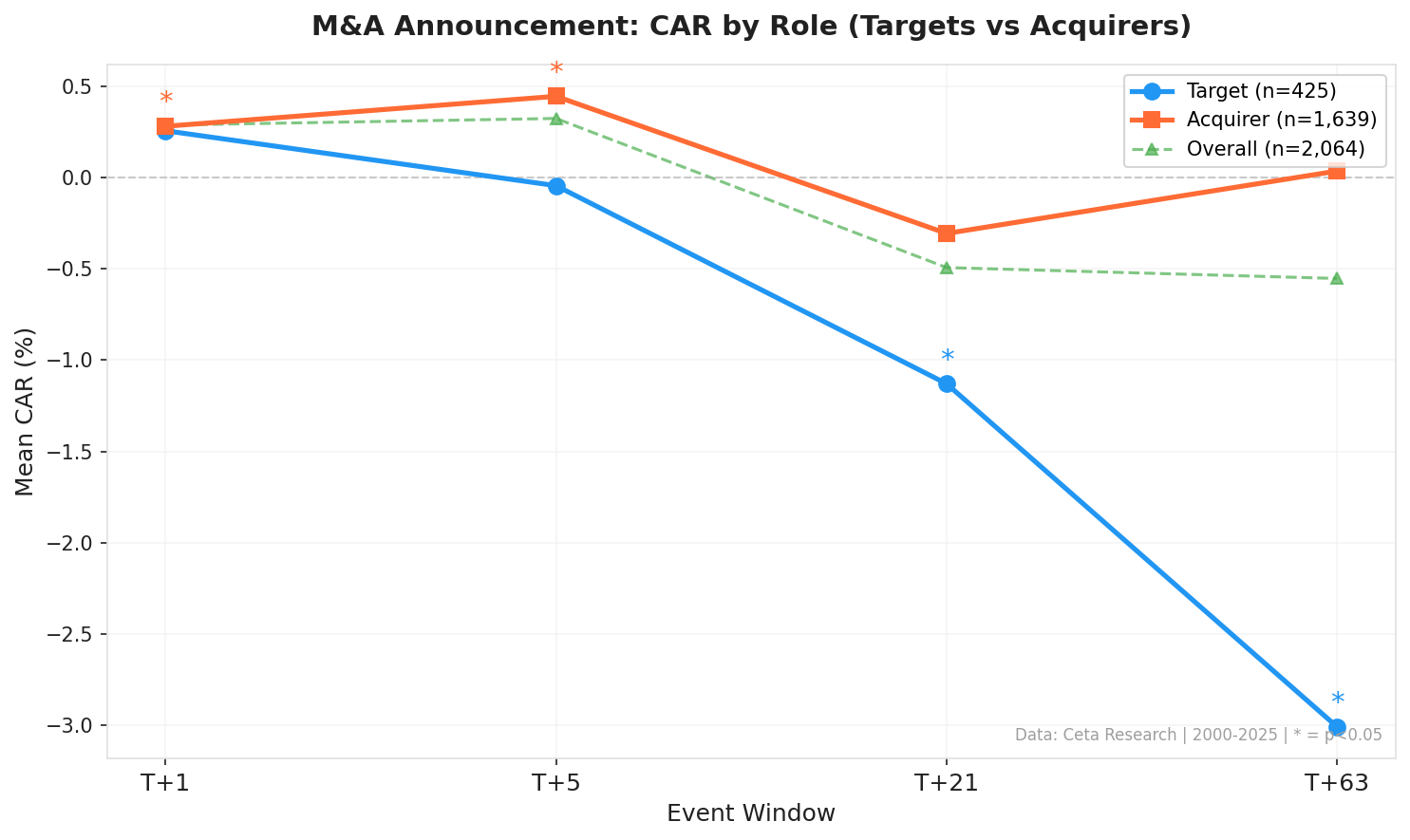

We ran an event study on 2,064 M&A announcements from 2000 to 2025. The finding that surprised us most: acquirers don't drop. They drift higher in the week after the filing. The classic "acquirer's curse" doesn't show up in this dataset. Here's what the data actually shows.

Contents

Method

We used the mergers_acquisitions_latest table, which contains SEC-sourced M&A filing data from FMP. Each row is an acquirer reporting a target company to regulators.

A few things to know about the data before we get to results.

It's SEC filing data, not press announcements. The transactionDate field is when the deal was filed with the SEC, which may be days or weeks after the press release. By the time a filing hits, some of the initial price reaction may already be in.

It needs deduplication. The average deal generates 2.9 filings because different share classes of the same acquirer file separately. We collapse to one event per (symbol, transaction date) pair.

Coverage is selective. Not every public M&A deal appears in this dataset. Coverage improved after 2016. And about half of target companies have no US price data because they're private or foreign. We only include targets with price data in the target pool.

No deal price or terms. This is the biggest limitation. We can't compute deal spreads, premium percentages, or deal-type breakdowns. This is a post-announcement return study, not a traditional merger arbitrage analysis.

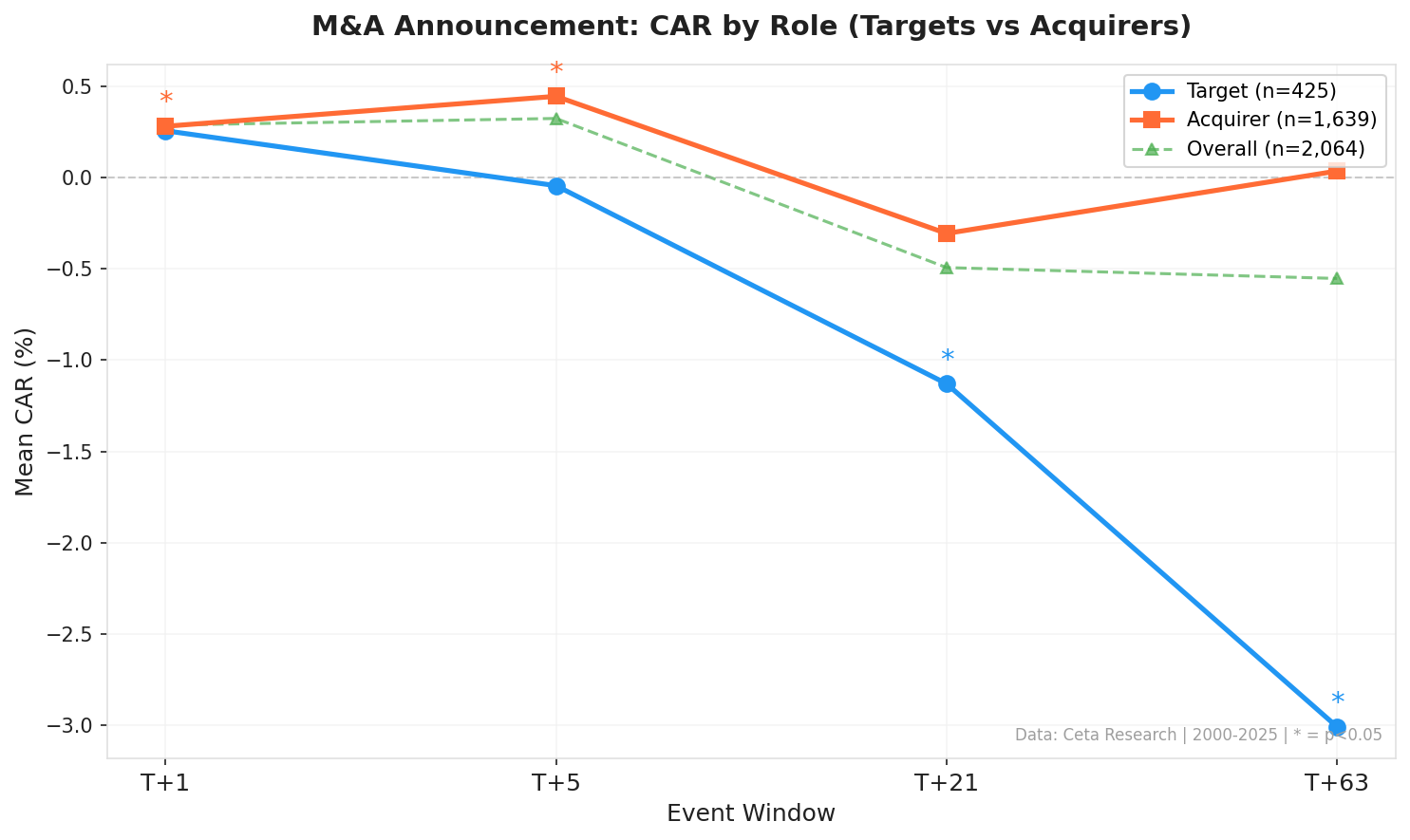

The final dataset: 425 target events and 1,639 acquirer events, spanning 2000 through 2025. We measure cumulative abnormal returns (CAR) at T+1, T+5, T+21, and T+63 trading days. Abnormal return means the stock's return minus SPY's return over the same window. We use winsorization at the 1st/99th percentile to limit the impact of extreme outliers.

What We Found

Acquirers drift higher, not lower.

The dominant narrative in M&A research is that acquirers pay too much and their shareholders suffer. Roll's "hubris hypothesis" from 1986 describes exactly this. Our data doesn't support it for short-term windows.

Acquirer stocks gained an average of +0.28% abnormal return at T+1 (t-stat 3.27, significant at p<0.05) and +0.44% at T+5 (t-stat 2.71, also significant). By T+21 and T+63, the effect fades to noise.

Why might acquirers hold up or gain slightly? A few reasons. First, because transactionDate is the filing date, not the press date, the initial negative market reaction may have already resolved by the time we measure. Second, this dataset skews toward deals that cleared the $1B market cap threshold for both parties. Larger, more strategic acquirers may command more market trust for their M&A decisions than the full universe.

Targets show no statistically significant T+1 reaction.

This one surprised us too. Targets gained +0.26% at T+1, but the t-stat is only 1.59. That's not significant. The filing-vs-announcement gap almost certainly explains this: by the time the SEC filing is in, the target's stock has already repriced toward the deal value.

The target T+63 number is a survivorship artifact.

At T+63, targets show -3.01% mean CAR (t-stat -2.85, statistically significant). That sounds like targets dramatically underperform. But the sample size tells the real story.

We start with 425 target events at T+1. By T+63, only 326 remain. That's 99 events, or 23% of the sample, that dropped out. Most of those missing events are successfully completed deals where the target was delisted after the acquisition closed.

So the targets still trading at T+63 are disproportionately those where the deal stalled, faced regulatory challenges, or fell apart. Deals that break are disasters for targets. The -3.01% is measuring the "failed or delayed deal" population, not M&A targets in general.

This doesn't make the T+63 number useless. It's informative about what happens to acquisition targets when deals don't go smoothly. But it's not a forward-looking prediction about all targets.

The Data

| Pool | Events | T+1 CAR | t-stat | T+5 CAR | t-stat | T+21 CAR | t-stat | T+63 CAR | t-stat |

|---|---|---|---|---|---|---|---|---|---|

| Overall | 2,064 | +0.29%* | 3.70 | +0.32%* | 2.36 | -0.49% | -1.87 | -0.55% | -1.02 |

| Acquirers | 1,639 | +0.28%* | 3.27 | +0.44%* | 2.71 | -0.31% | -0.97 | +0.04% | 0.06 |

| Targets | 425 | +0.26% | 1.59 | -0.05% | -0.19 | -1.13%* | -2.53 | -3.01%* | -2.85 |

* = significant at p<0.05

Note: Target T+63 n=326 (99 events delisted, mostly completed deals).

The acquirer signal is the clean finding here. Positive and statistically significant at both T+1 and T+5. Then it goes to noise. There's no long-term drift for acquirers in either direction.

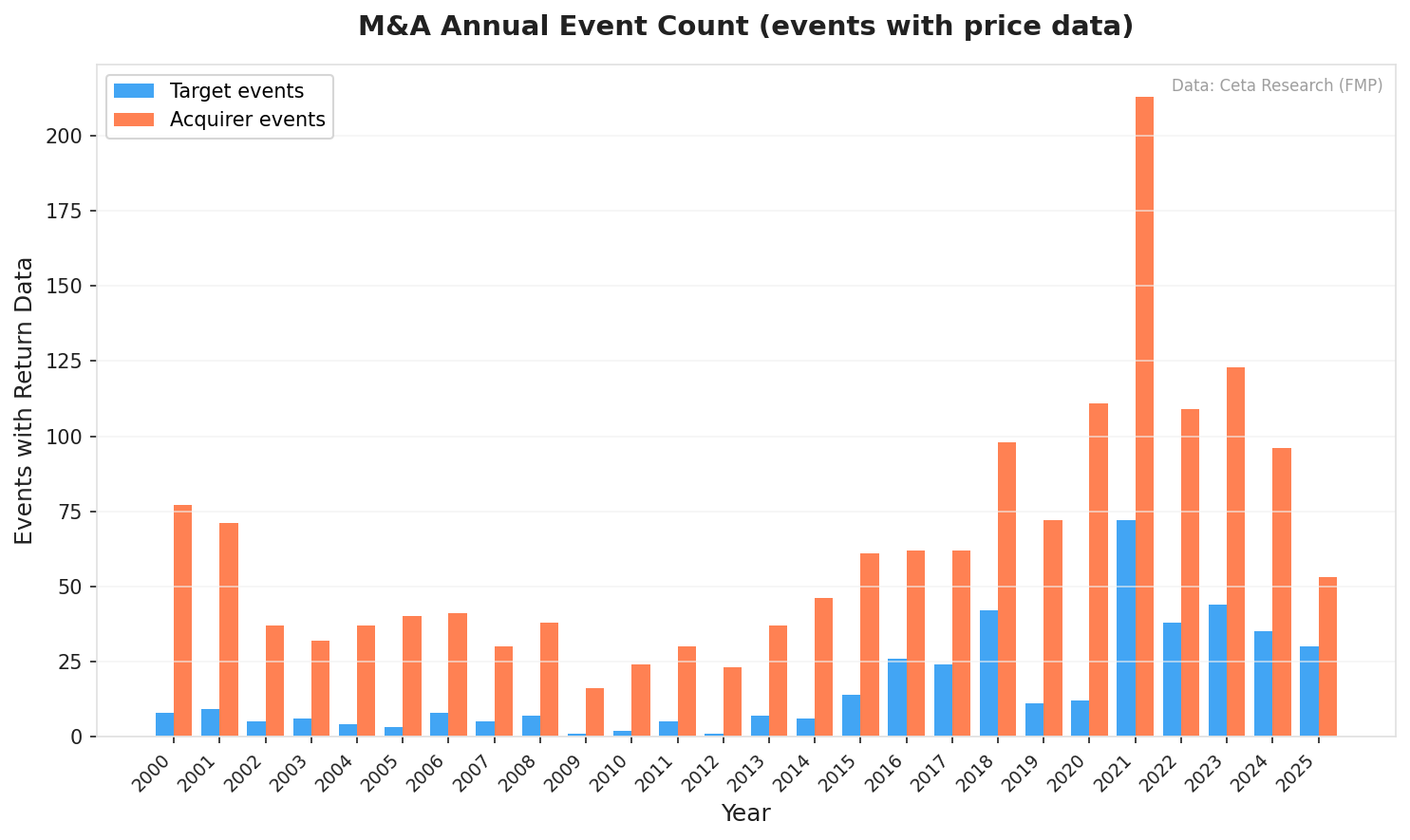

Annual event counts

M&A activity follows the credit cycle. The 2009 financial crisis nearly stopped deals entirely (17 total events). Activity rebuilt through the 2010s and peaked in 2021 at 285 events, driven partly by the SPAC-driven deal surge. It's run at 130-165 events per year since.

Limitations

The filing-vs-announcement gap. The most important limitation. If transactionDate is systematically days or weeks after the press announcement, our T+1 and T+5 results are measuring post-announcement drift, not announcement reaction. The acquirer gains might be drift rather than an initial market judgment. We can't separate these with the available data.

No deal terms. We can't split by cash vs stock deals, premium size, deal size relative to acquirer, or hostile vs friendly. All of these affect how markets react. We're averaging across a heterogeneous population.

No deal outcome tracking. Failed deals get pooled with completed deals in the T+1 through T+21 windows. If failed deals account for, say, 15% of events and they produce extreme negative returns, that dilutes any completion premium signal.

Coverage selectivity. Not every M&A deal is in this dataset. The coverage improved significantly after 2016 (2021 has 6x more events than 2010). We don't know what systematic differences exist between covered and uncovered deals.

SPY as benchmark. SPY captures broad market movement but doesn't control for sector or size factors. An acquirer in a bull tech market will look artificially good vs SPY even if its M&A reaction was flat.

What This Tells You

For anyone holding an acquirer stock when a deal is announced: based on 25 years of data, the short-term market reaction is slightly positive, not negative. The "acquirer drops on deal news" narrative fits some high-profile cases but doesn't hold in aggregate for large-cap US acquirers.

For anyone holding a target: the immediate reaction in this dataset is muted because the filing date lags the announcement. If you own a target from the day of press announcement (which our data doesn't capture cleanly), you've likely already seen the bulk of the gain.

The long-term target underperformance is real, but it's telling you about deal uncertainty and failure risk, not about M&A in general. A target still trading at 63 days post-filing is one where something is going slower than expected.

Screen for Current M&A Activity

To see deals filed in the last 90 days, run this query on Ceta Research:

WITH recent AS (

SELECT

symbol AS acquirer,

targetedSymbol AS target,

companyName AS acquirer_name,

targetedCompanyName AS target_name,

CAST(transactionDate AS DATE) AS deal_date,

ROW_NUMBER() OVER (

PARTITION BY targetedSymbol, CAST(transactionDate AS DATE)

ORDER BY acceptedDate DESC

) AS rn

FROM mergers_acquisitions_latest

WHERE CAST(transactionDate AS DATE) >= CURRENT_DATE - INTERVAL 90 DAY

AND targetedSymbol IS NOT NULL AND TRIM(targetedSymbol) != ''

AND NOT (symbol LIKE '%-WT' OR symbol LIKE '%-WS'

OR (symbol LIKE '%W' AND LENGTH(symbol) > 5))

)

SELECT acquirer, target, acquirer_name, target_name, deal_date

FROM recent

WHERE rn = 1

ORDER BY deal_date DESC

LIMIT 30

References

- Mitchell, M. & Pulvino, T. (2001). "Characteristics of Risk and Return in Risk Arbitrage." Journal of Finance, 56(6), 2135-2175.

- Baker, M. & Savasoglu, S. (2002). "Limited Arbitrage in Mergers and Acquisitions." Journal of Financial Economics, 64(1), 91-115.

- Roll, R. (1986). "The Hubris Hypothesis of Corporate Takeovers." Journal of Business, 59(2), 197-216.

Data: Ceta Research data warehouse (FMP/SEC-sourced M&A filing data). 2,064 events, 2000-2025. US stocks only (NYSE/NASDAQ/AMEX), market cap above $1B. CAR = cumulative abnormal return vs SPY. Winsorized at 1st/99th percentile. transactionDate = SEC filing date, not necessarily press announcement date. This is educational content, not investment advice.