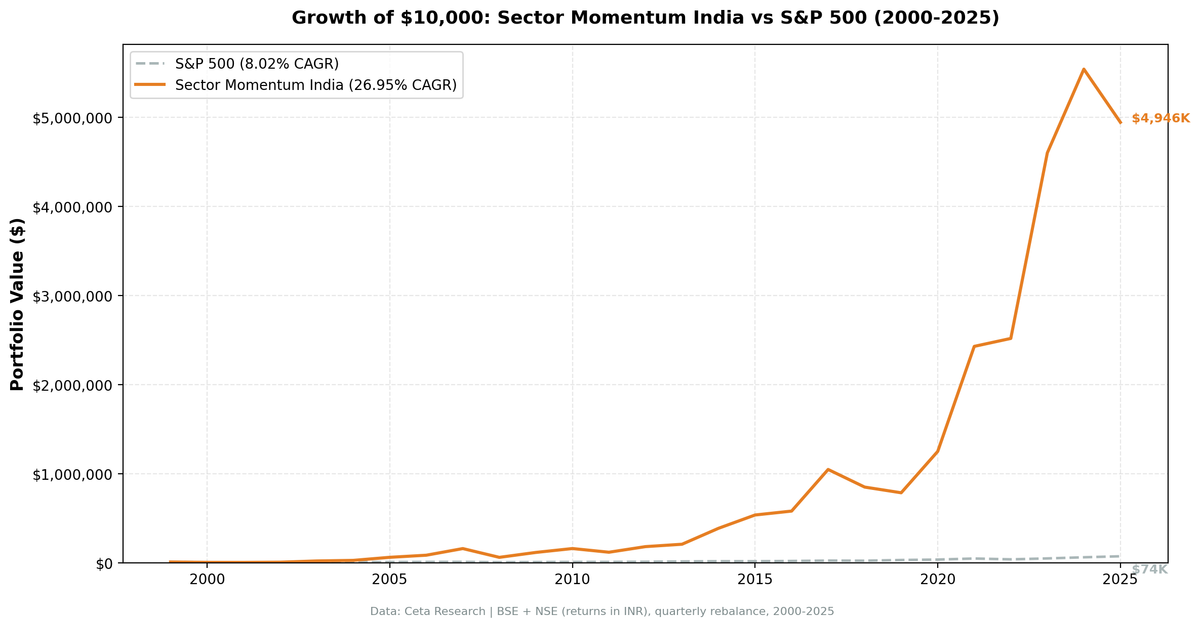

Sector Momentum in India: 26.95% CAGR, +18.93% Excess Over 26 Years

India produced the highest absolute CAGR of any exchange in our 14-market sector momentum study. 26.95% annually over 26 years. $10,000 grew to nearly $5 million in INR-denominated terms. No other market in the dataset came close.

Contents

- The Strategy

- What We Found

- Sector Rotation Patterns

- When It Worked and When It Didn't

- Full Annual Returns

- Limitations

The strategy is simple: every quarter, identify the two sectors with the strongest trailing 12-month returns and hold the stocks within them. Rotate when the leaders change. That mechanical rule, applied to India's BSE + NSE exchanges from 2000 to 2025, produced returns that look impossible until you study how India's sector cycles actually work.

The Strategy

Indian equity markets don't move uniformly. Technology ran for years. Healthcare ran for years. Utilities and Consumer Defensive showed up repeatedly as top-two sectors across two dozen quarters each. When a sector catches a structural tailwind in India's growth economy, it tends to sustain momentum for multiple rebalance periods. That persistence is exactly what this strategy exploits.

The mechanics:

| Parameter | Value |

|---|---|

| Universe | BSE + NSE (India) |

| Signal | Top 2 sectors by trailing 12-month equal-weighted return |

| Selection | All qualifying stocks in those sectors |

| Rebalancing | Quarterly |

| Period | 2000-2025 (26 years, 104 quarters) |

| Cash periods | 3 of 104 (3%) |

| Avg stocks held | 186.7 |

| Benchmark | S&P 500 Total Return (SPY, USD) |

| Data source | Ceta Research (FMP financial data warehouse) |

Returns are in INR. SPY is a USD benchmark used for cross-exchange comparison. The currency difference means the excess return comparison is illustrative, not exact. Full methodology: backtests/METHODOLOGY.md

What We Found

Start with the calendar years. In 2003, the portfolio returned +178.66% while SPY returned +24.12%. In 2005: +121.27% vs +7.17%. In 2007: +86.39% vs +4.40%. In 2021: +94.20% vs +31.26%. In 2023: +82.68% vs +26.0%.

These aren't one-off flukes scattered across 26 years. They're a pattern. India's sector momentum strategy produced explosive calendar-year gains repeatedly, in different macro environments, driven by different sectors each time.

The aggregate numbers reflect that:

| Metric | Portfolio | S&P 500 (USD) |

|---|---|---|

| CAGR (2000-2025) | 26.95% | 8.02% |

| Excess CAGR | +18.93% | — |

| Max drawdown | -63.87% | -36.27% |

| Sharpe ratio | 0.560 | — |

| Sortino ratio | 1.101 | — |

| Calmar ratio | 0.422 | — |

| Beta | 1.082 | 1.0 |

| Alpha | 18.8% | — |

| Up capture | 185.72% | 100% |

| Down capture | 42.42% | 100% |

| Win rate vs SPY | 65.38% | — |

| $10K → | ~$4,946,400 | $74,347 |

The up capture of 185.72% is the central result. When global markets rise, this strategy rose nearly twice as fast. That's what 26.95% CAGR over 26 years looks like mechanically: sustained outperformance in up markets, with a down capture of 42.42% providing partial protection when markets fall.

Sector Rotation Patterns

The strategy doesn't hold one sector forever. It rotates as momentum shifts. But some sectors dominated the top-two positions far more than others across 104 quarterly rebalances:

| Sector | Quarters in Top 2 |

|---|---|

| Technology | 29 |

| Consumer Defensive | 24 |

| Healthcare | 26 |

| Utilities | 25 |

| Consumer Cyclical | 21 |

| Real Estate | 21 |

| Industrials | 16 |

| Financial Services | 16 |

| Energy | 15 |

| Basic Materials | 11 |

| Communication Services | 4 |

Technology, Healthcare, Utilities, and Consumer Defensive occupied the top-two positions for 25+ quarters each. That's not random rotation. India's IT sector (Infosys, TCS, Wipro, HCL) and its pharma sector (Sun Pharma, Dr. Reddy's, Cipla) have sustained structural growth stories that produced multi-year momentum trends. Utilities and Consumer Defensive showed up in defensive rotation periods. The strategy captured all of it.

Communication Services appeared only 4 times. Basic Materials only 11. India's sector momentum is concentrated in quality-growth and defensive sectors, not commodities. That's the opposite of Canada's pattern.

When It Worked and When It Didn't

The early boom years (2002-2007)

After a difficult 2000 (-41.75%, tech crash), the strategy strung together extraordinary returns:

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2002 | +41.77% | -19.92% | +61.7% |

| 2003 | +178.66% | +24.12% | +154.5% |

| 2004 | +29.44% | +10.24% | +19.2% |

| 2005 | +121.27% | +7.17% | +114.1% |

| 2006 | +37.64% | +13.65% | +24.0% |

| 2007 | +86.39% | +4.40% | +82.0% |

Six consecutive years of substantial outperformance. India's IT sector was in a global outsourcing boom. Healthcare was expanding domestically. The strategy rotated through these momentum leaders and captured the bulk of the gains.

2008: The severity of the drawdown

India wasn't insulated from the global financial crisis:

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2008 | -61.26% | -34.31% | -27.0% |

| 2009 | +88.55% | +24.73% | +63.8% |

A -61.26% drawdown is severe. The strategy's max drawdown of -63.87% came primarily from this period. The recovery in 2009 was swift, but 2008 is the honest caveat in this dataset. When Indian sectors got caught in momentum positions heading into the global crash, the drawdown was painful.

The Modi years and beyond (2014-2017)

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2014 | +85.55% | +14.50% | +71.1% |

| 2015 | +38.42% | -0.12% | +38.5% |

| 2016 | +8.16% | +14.45% | -6.3% |

| 2017 | +80.33% | +21.64% | +58.7% |

2014 was an election year. The BJP's decisive victory unleashed a broad equity rally across Indian sectors. The momentum strategy was already positioned in the leading sectors and captured most of that move. 2015 and 2017 continued the theme.

2022-2023: Resilience during US rate hike cycle

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2022 | +3.66% | -18.99% | +22.7% |

| 2023 | +82.68% | +26.0% | +56.7% |

When US rate hikes crushed growth equities globally, India's sector momentum held. 2022 returned +3.66% while SPY fell nearly 19%. Then 2023 delivered +82.68%. India's domestic demand story and sector rotation kept the strategy productive.

Difficult years: 2019 and 2025

The strategy had two notably bad recent years:

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2019 | -7.51% | +32.31% | -39.8% |

| 2025 | -10.77% | +17.88% | -28.6% |

2019 was a particularly bad miss. SPY surged while the India portfolio fell. Indian equity markets underperformed globally that year as economic growth slowed and credit stress spread. The strategy was caught in sectors that reversed sharply. 2025 shows a similar dynamic, with INR-denominated returns turning negative while US markets advanced.

Full Annual Returns

| Year | Portfolio (INR) | SPY (USD) | Excess |

|---|---|---|---|

| 2000 | -41.75% | -10.5% | -31.2% |

| 2001 | -4.92% | -9.17% | +4.3% |

| 2002 | +41.77% | -19.92% | +61.7% |

| 2003 | +178.66% | +24.12% | +154.5% |

| 2004 | +29.44% | +10.24% | +19.2% |

| 2005 | +121.27% | +7.17% | +114.1% |

| 2006 | +37.64% | +13.65% | +24.0% |

| 2007 | +86.39% | +4.40% | +82.0% |

| 2008 | -61.26% | -34.31% | -27.0% |

| 2009 | +88.55% | +24.73% | +63.8% |

| 2010 | +37.21% | +14.31% | +22.9% |

| 2011 | -25.72% | +2.46% | -28.2% |

| 2012 | +52.62% | +17.09% | +35.5% |

| 2013 | +14.61% | +27.77% | -13.2% |

| 2014 | +85.55% | +14.50% | +71.1% |

| 2015 | +38.42% | -0.12% | +38.5% |

| 2016 | +8.16% | +14.45% | -6.3% |

| 2017 | +80.33% | +21.64% | +58.7% |

| 2018 | -18.85% | -5.15% | -13.7% |

| 2019 | -7.51% | +32.31% | -39.8% |

| 2020 | +59.00% | +15.64% | +43.4% |

| 2021 | +94.20% | +31.26% | +62.9% |

| 2022 | +3.66% | -18.99% | +22.7% |

| 2023 | +82.68% | +26.00% | +56.7% |

| 2024 | +20.42% | +25.28% | -4.9% |

| 2025 | -10.77% | +17.88% | -28.6% |

Limitations

Currency mismatch. Returns are in INR. USD-based investors face additional USD/INR exchange rate risk. Rupee depreciation periods reduce the USD-equivalent return. The comparison to SPY (USD) is illustrative rather than directly tradeable.

The max drawdown. -63.87% isn't a comfortable strategy to hold. 2008 alone produced a -61.26% calendar year loss. Any investor running this strategy through 2008 needed extreme conviction to stay in through the recovery.

Sector concentration. When Technology or Healthcare dominate the top-two positions for 6-8 consecutive quarters, the portfolio is heavily concentrated in one sector type. That works when momentum is sustained. When a sector reverses sharply, the next rebalance captures the losses before rotating out.

Benchmark mismatch. SPY (USD) is a global comparison tool, not a local Indian benchmark. Against the Nifty 50 or Sensex, the excess returns would be different, and potentially smaller.

Data coverage. FMP's BSE + NSE coverage from 2000 isn't complete for early years. The avg stock count of 186.7 reflects current coverage, but early periods may have thinner representation. Results before 2005 should be read with some caution.

Not replicable as stated. The strategy selects from all qualifying stocks in the top-two sectors. With 186 average holdings, transaction costs, slippage, and liquidity constraints on smaller Indian names would reduce actual returns meaningfully. Treat these as theoretical backtest results, not live portfolio projections.

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP financial data warehouse). Universe: BSE + NSE (India). Period: 2000-2025 (26 years), quarterly rebalance, returns in INR. Past performance doesn't guarantee future results. This is educational content, not investment advice.

Part of the Sector Momentum Rotation series. US flagship blog