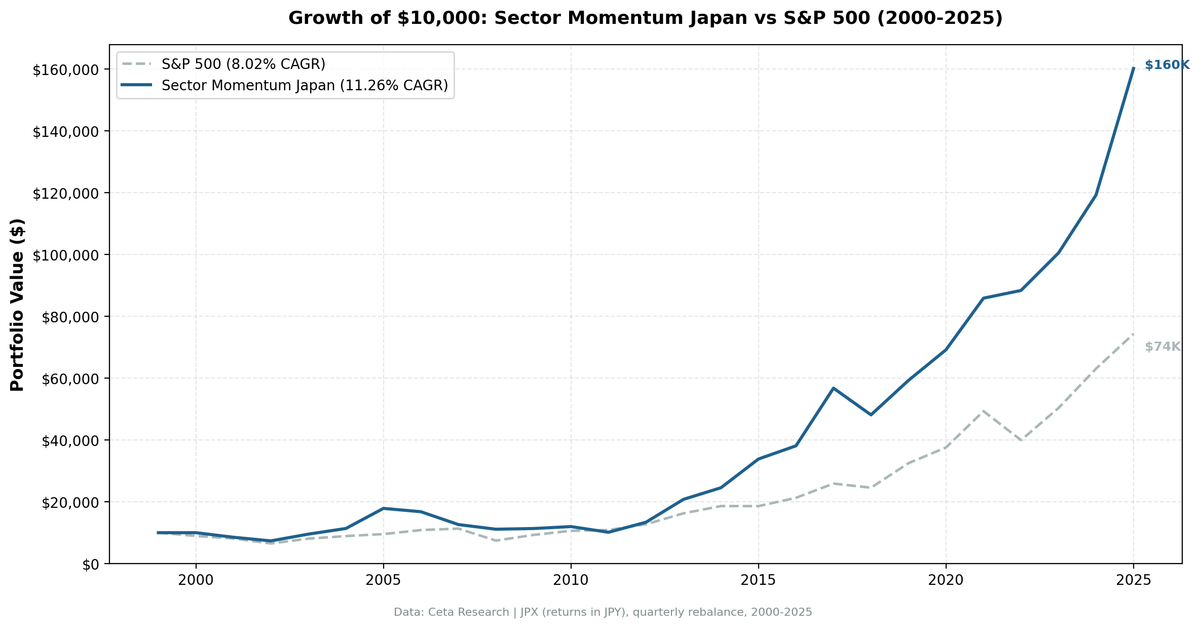

Sector Momentum in Japan: 11.26% CAGR, +22.4% Relative Return in 2008

In 2008, the global financial system nearly collapsed. SPY fell -34.31%. Japan's sector momentum portfolio fell -11.9%. That +22.4% relative return in the worst year of the century tells you most of what you need to know about how this strategy behaves in Japanese markets.

Contents

- The Strategy

- Results

- Japan's Sector Rotation Structure

- The Years That Define the Strategy

- Full Annual Returns

- Limitations

Five years later, Abenomics hit. Japan's government launched the largest domestic stimulus program in its post-war history. Real Estate and Healthcare surged. The portfolio returned +55.37% in 2013 while SPY returned +27.77%. The two years together capture the core structure of Japan's sector rotation: domestic-facing sectors (Real Estate, Healthcare) that don't move with US credit cycles and do respond to Japanese policy.

Over 26 years, the strategy produced 11.26% CAGR versus 8.02% for SPY, with a down capture of 54.68%. In JPY-denominated terms, the portfolio compounded substantially. The Sharpe of 0.605 and Sortino of 1.003 reflect a strategy that protected capital in down markets while participating meaningfully in up markets.

The Strategy

Each quarter, we rank all 11 GICS sectors by their equal-weighted 12-month trailing return across JPX-listed stocks. We hold stocks from the top 2 sectors, equal-weighted, rebalanced quarterly. Stocks must clear an exchange-specific market cap threshold. Transaction costs of 0.1% per trade are applied.

Full methodology: backtests/METHODOLOGY.md

| Parameter | Value |

|---|---|

| Universe | JPX (Japan Exchange Group) |

| Signal | Top 2 sectors by trailing 12-month equal-weighted return |

| Selection | All qualifying stocks in those sectors |

| Rebalancing | Quarterly |

| Period | 2000-2025 (26 years, 104 quarters) |

| Cash periods | 7 of 104 (7%) |

| Avg stocks held | 134.0 (when invested) |

| Benchmark | S&P 500 Total Return (SPY, USD) |

| Data source | Ceta Research (FMP financial data warehouse) |

Returns are in JPY. SPY is a USD benchmark for cross-exchange comparison. The currency difference makes excess return comparisons illustrative rather than exact.

Results

| Metric | Portfolio | S&P 500 (USD) |

|---|---|---|

| CAGR (2000-2025) | 11.26% | 8.02% |

| Excess CAGR | +3.24% | — |

| Max drawdown | -46.31% | -45.53% |

| Sharpe ratio | 0.605 | — |

| Sortino ratio | 1.003 | — |

| Calmar ratio | 0.243 | — |

| Up capture | 94.36% | — |

| Down capture | 54.68% | — |

The down capture of 54.68% is the defining number. Japan's sector momentum portfolio fell roughly half as much as SPY in down periods on average. The max drawdown of -46.31% is close to SPY's -45.53%, but that similarity masks an important difference in timing: Japan's worst drawdowns didn't coincide with the GFC, as seen in the 2008 result below.

Seven cash periods across 104 quarters (7%) is the highest cash rate in the study's major exchanges. When no sector generated sufficient momentum signal, the strategy stepped aside. That happened twice in 2000 and added to the crisis protection profile.

Japan's Sector Rotation Structure

Japan's demographic reality is built into the rotation. An aging population creates durable healthcare demand. Decades of urban density and limited supply created persistent real estate tailwinds. Technology rode Japan's export cycle with global semiconductor and electronics demand.

| Sector | Quarters in Top 2 |

|---|---|

| Real Estate | 31 |

| Healthcare | 28 |

| Technology | 28 |

| Energy | 25 |

| Basic Materials | 13 |

| Consumer Defensive | 17 |

| Utilities | 16 |

| Financial Services | 11 |

| Communication Services | 11 |

| Consumer Cyclical | 10 |

| Industrials | 10 |

Real Estate led with 31 quarters. Healthcare and Technology tied at 28 each. These three sectors together account for 84 of 104 quarters in the top-2 rotation. That's not diversified rotation. It's concentrated in Japan-specific structural themes.

Real Estate's dominance reflects the post-GFC recovery in Tokyo commercial property and residential REITs, driven by BOJ accommodation and Abenomics. Healthcare's persistence reflects Japan's demographic reality: the country has the oldest median population in the world, and the healthcare sector has sustained multi-decade demand growth. Technology tracks Japan's position in global semiconductor supply chains.

Energy appeared 25 times, often during global commodity cycles. Consumer Cyclical and Industrials, which one might expect from Japan's manufacturing base, appeared in only 10 quarters each. Japan's export industrials don't generate strong trailing momentum signals because their returns are often driven by JPY/USD exchange rate moves rather than sector fundamentals.

The Years That Define the Strategy

2000: Cash preservation during the dotcom crash. The strategy returned 0.0% while SPY fell -10.5%. Japan stepped to cash. No sectors generated a sufficient momentum signal in a market still working through its own asset bubble aftermath. The result was the preservation of capital during a global equity selloff.

2008: The standout result. The most important year in the dataset.

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2008 | -11.9% | -34.31% | +22.4% |

| 2009 | +2.02% | +24.73% | -22.7% |

In 2008, Japan's Real Estate and Healthcare sectors held up while US financial and energy sectors collapsed. Japan's property market wasn't exposed to US subprime derivatives. Japan's healthcare companies served domestic demand. The strategy was already in those sectors and didn't need to rotate mid-crisis. The -11.9% loss is still real, but in the context of -34.31% for SPY, the gap is substantial.

The 2009 follow-through is the honest caveat. Japan's market didn't recover with the US in 2009. The portfolio returned +2.02% while SPY surged +24.73%. Japan's real estate cycle was unwinding from its own 2007 peak. The strategy was positioned in sectors that recovered slowly in Japan while US cyclicals bounced hard. The 2008 protection came at the cost of 2009 participation.

2007: The Japan real estate unwind begins. Before the 2008 protection story, there's 2007.

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2007 | -24.78% | +4.4% | -29.2% |

Japan's real estate sector peaked in 2006-2007 and began unwinding. The strategy was still positioned in Real Estate based on prior momentum, and took a -24.78% loss in a year when SPY gained 4.4%. This is the clearest example of momentum lag risk: the signal held sectors that were reversing because their trailing return was still positive from prior quarters.

2013: Abenomics. The strategy's best absolute year.

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2013 | +55.37% | +27.77% | +27.6% |

Prime Minister Abe's stimulus package, monetary easing, and structural reform agenda launched in late 2012. By 2013, Japanese equities were in a broad-based rally. Real Estate benefited from BOJ buying of J-REITs. Healthcare saw expanded public spending. The strategy was already in the momentum leaders and rode the policy tailwind for the full year. +55.37% in a single calendar year.

2015: Continuation. The strategy returned +37.85% vs SPY -0.12%. Japan's domestic sectors were still running on policy momentum while US markets went flat.

2022: Defensive positioning during US rate hikes. Another year where Japan's domestic sector bias provided protection.

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2022 | +2.91% | -18.99% | +21.9% |

When the Fed raised rates aggressively and crushed US growth equities, Japan's Real Estate and Healthcare sectors, largely insulated from US rate cycles, held value. The portfolio returned +2.91% while SPY fell -18.99%. The pattern from 2008 repeated: when the US equity market faces domestic macro stress, Japan's domestically oriented rotation holds.

2025: Strong finish. +34.32% vs SPY +17.88% (+16.4% relative). Japan's recent momentum in Healthcare and Real Estate continued to compound.

Full Annual Returns

| Year | Portfolio (JPY) | SPY (USD) | Excess |

|---|---|---|---|

| 2000 | 0.0% | -10.5% | +10.5% |

| 2001 | -14.73% | -9.17% | -5.6% |

| 2002 | -13.77% | -19.92% | +6.2% |

| 2003 | +29.73% | +24.12% | +5.6% |

| 2005 | +57.2% | +7.17% | +50.0% |

| 2006 | -6.04% | +13.65% | -19.7% |

| 2007 | -24.78% | +4.4% | -29.2% |

| 2008 | -11.9% | -34.31% | +22.4% |

| 2009 | +2.02% | +24.73% | -22.7% |

| 2012 | +31.95% | +17.09% | +14.9% |

| 2013 | +55.37% | +27.77% | +27.6% |

| 2015 | +37.85% | -0.12% | +38.0% |

| 2020 | +16.7% | +15.64% | +1.1% |

| 2021 | +24.13% | +31.26% | -7.1% |

| 2022 | +2.91% | -18.99% | +21.9% |

| 2023 | +13.73% | +26.0% | -12.3% |

| 2024 | +18.65% | +25.28% | -6.6% |

| 2025 | +34.32% | +17.88% | +16.4% |

The pattern across 26 years is clear: Japan outperforms in global down years (2000, 2002, 2008, 2022) and in Japan-specific policy cycles (2013, 2015, 2025). Japan underperforms in US-driven recovery years (2009, 2021, 2023) and when Japan's own property cycle turns (2006-2007).

Limitations

Currency mismatch. Returns are in JPY. USD-based investors face JPY/USD exposure. The yen has depreciated against the dollar over parts of this period, which would reduce USD-equivalent returns materially in some years. The comparison to SPY is illustrative, not directly tradeable.

The 2007-2009 sequence. The -24.78% in 2007 followed by -11.9% in 2008 and +2.02% in 2009 represents 3 years of compounded loss while the US recovered. Investors who entered Japan's sector momentum strategy in 2006 endured a difficult multi-year stretch before the recovery in 2012-2013.

Momentum lag. The 2007 loss is the clearest example of the core risk: a sector that ran strongly can generate a positive 12-month signal even as it begins to reverse. The strategy holds until the signal flips, meaning it participates in the early phase of reversals before rotating out.

Sector concentration. Real Estate, Healthcare, and Technology together accounted for 84 of 104 quarters. Investors aren't getting broad Japanese market exposure. They're making a concentrated bet on Japan's demographic and property themes. When those themes are out of favor, the strategy underperforms.

Cash drag. Seven cash periods (7%) is the highest rate in the study's major exchanges. Those quarters earn nothing. In strong up markets, that drag reduces total compounding.

Benchmark mismatch. SPY (USD) is a cross-market comparison tool. Against TOPIX or Nikkei 225, the excess returns would differ, and the comparison would be more meaningful for a Japanese investor.

2009 recovery miss. Protecting capital in 2008 is valuable. Not participating in the 2009 recovery is the cost. Investors who held SPY through 2008-2009 ended the two-year period roughly where this strategy did, but through a different path.

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP financial data warehouse). Universe: JPX (Japan Exchange Group). Period: 2000-2025 (26 years), quarterly rebalance, returns in JPY. Past performance doesn't guarantee future results. This is educational content, not investment advice.

Part of the Sector Momentum Rotation series. US flagship blog