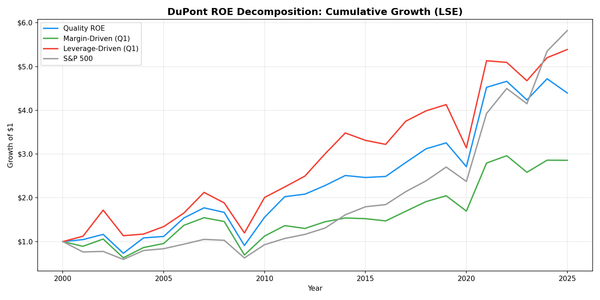

DuPont analysis

DuPont ROE on UK Stocks: +5.30% Over FTSE 100, Leverage Leads at 7.70% CAGR

DuPont ROE decomposition on LSE from 2000-2025. Leverage-driven ROE at 7.00% CAGR beat margin-driven at 4.30%. The UK reverses the US pattern: commodity-heavy sectors and dividend culture reward productive leverage.