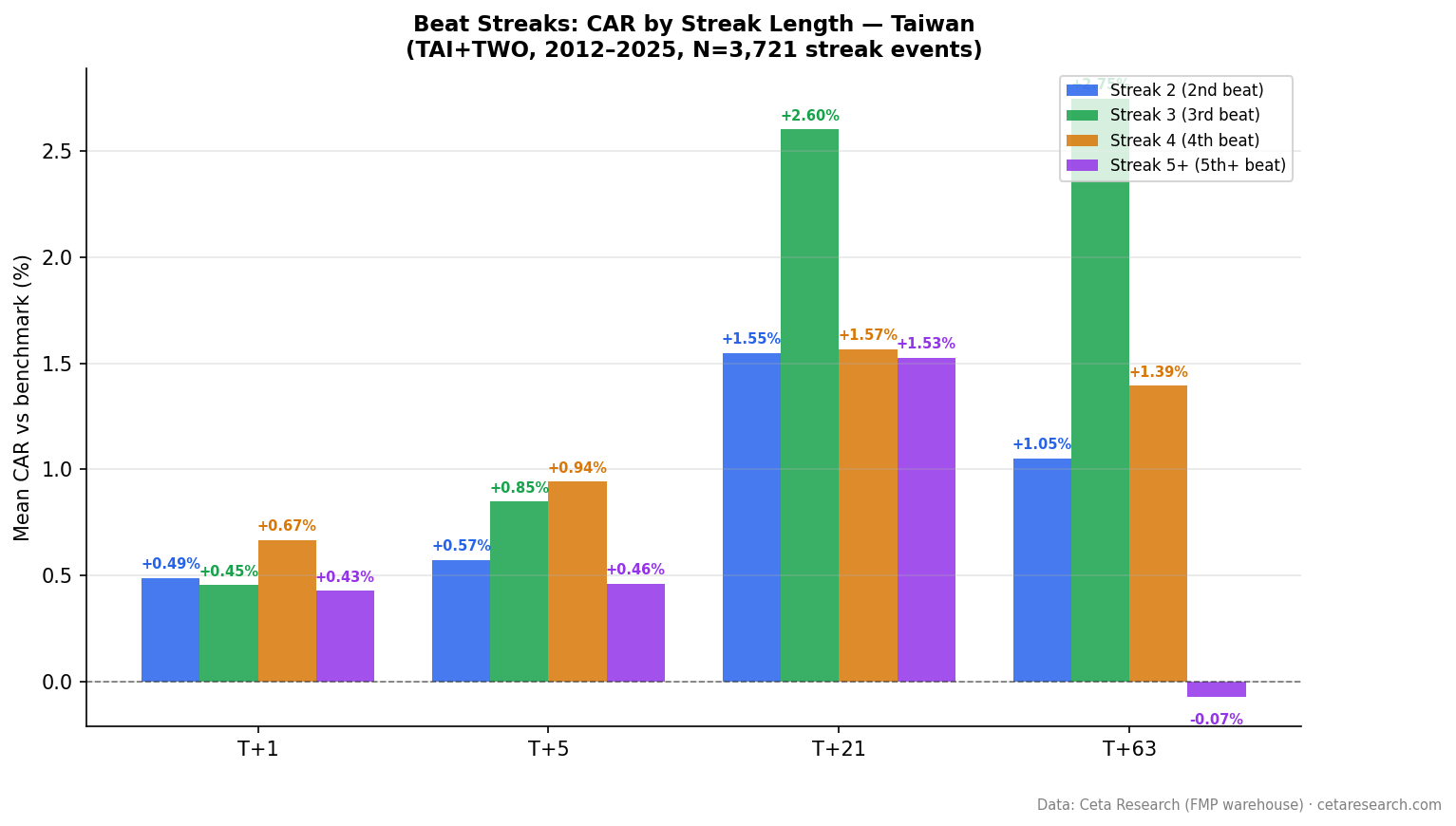

Beat Streaks in Taiwan: +1.79% T+21 in a Tech-Heavy Market

Taiwan shows delayed post-announcement drift that builds to +1.79% by day 21. Streak 3 reaches +2.60% T+21 and +2.75% T+63. 3,721 events from 2012-2025. The muted day-1 reaction followed by strong drift suggests gradual information incorporation.

Taiwan beats analyst EPS estimates and then keeps beating them. When you track what happens to stock prices after the 2nd, 3rd, and 4th consecutive beat on TWSE and TPEX, you find a market that barely reacts on day 1 but builds a +1.79% abnormal return by day 21. The drift is real, it's statistically significant, and it's concentrated in the streaks that matter most.

Contents

Method

Data source: TradingStudio (FMP earnings data) Universe: TWSE + TPEX (TAI + TWO exchanges), market cap > TWD 10B (historical key_metrics) Period: 2012–2025 Benchmark: SPY (S&P 500 ETF, see Limitations) Beat definition: epsActual > epsEstimated, with ABS(epsEstimated) > 0.01 Streak computation: Window functions (PARTITION BY symbol ORDER BY date) to count consecutive beats

Event windows: T+1, T+5, T+21, T+63 trading days after each streak-extending announcement. Abnormal return = stock return minus SPY return over the same window.

Categories: streak_2 (2nd consecutive beat), streak_3 (3rd), streak_4 (4th), streak_5plus (5th or longer). Total events: 3,721 across all streak categories.

What We Found

Taiwan's beat-streak signal is almost entirely in the drift, not the announcement reaction.

The T+1 return is +0.49%. That's meaningful (t-stat 8.67), but it's one of the more muted day-1 reactions globally. Then something interesting happens. By T+21, the cumulative abnormal return has built to +1.79%, the third-highest T+21 result of any exchange in this study, behind only India and Brazil. The market is slowly processing information that the announcement itself didn't fully price.

By T+63, the CAR slips back to +1.20%. Some of the drift reverses. This pattern, strong accumulation through 21 days followed by partial reversal, fits a market where initial under-reaction gives way to correction but overshoots slightly in the other direction.

Taiwan's tech and semiconductor concentration amplifies this dynamic. Beat streaks cluster in companies where estimate uncertainty is high, semiconductor equipment, IC design, and electronics manufacturers where quarterly results depend on order cycles that analysts struggle to model precisely.

| Window | Mean CAR | t-stat | N |

|---|---|---|---|

| T+1 | +0.49% | 8.67 | 3,721 |

| T+21 | +1.79% | 9.43 | ~3,710 |

| T+63 | +1.20% | 3.70 | ~3,680 |

All three windows are statistically significant. The t-stats don't degrade dramatically as the window extends, which means the drift is broad-based, not driven by a handful of outlier events.

Streak Length Breakdown

The streak_3 result stands out immediately.

| Streak | N | T+1 | T+21 | T+63 |

|---|---|---|---|---|

| Streak 2 | 1,618 | +0.49% | +1.55% | +1.05% |

| Streak 3 | 818 | +0.45% | +2.60% | +2.75% |

| Streak 4 | 443 | +0.67% | +1.57% | +1.39% |

| Streak 5+ | 670 | +0.43% | +1.53% | -0.07% |

Streak_3 T+21 at +2.60% is the highest third-consecutive-beat result of any major developed market in this study. The T+63 of +2.75% is similarly strong. Something about a company's third consecutive beat in Taiwan signals durable performance that the market underprices.

Streak_4 shows slightly weaker results than streak_3. This is common across markets: by the fourth beat, some portion of the market has identified the pattern and the easy money is gone.

Streak_5+ T+63 at -0.07% deserves attention. Very long streaks in Taiwan produce no cumulative abnormal return over three months. One interpretation: by streak 5, these companies are either actively sandbagging estimates or are so well-known as consistent beaters that the market prices in the next beat before it happens. The announcement itself carries less new information.

The practical implication is clear. Streak_2 and streak_3 are where the signal lives. Streak_5+ is priced out.

The SQL Screen

This query identifies companies currently on active beat streaks of 3 or more quarters on Taiwanese exchanges.

WITH ordered_earnings AS (

SELECT

symbol,

CAST(date AS DATE) AS event_date,

epsActual AS actual,

epsEstimated AS estimated,

CASE WHEN epsActual > epsEstimated THEN 1 ELSE 0 END AS is_beat,

ROUND((epsActual - epsEstimated)

/ ABS(NULLIF(epsEstimated, 0)) * 100, 1) AS surprise_pct,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY date DESC) AS recency_rank

FROM earnings_surprises

WHERE exchange IN ('TAI', 'TWO')

AND epsEstimated IS NOT NULL

AND ABS(epsEstimated) > 0.01

AND epsActual IS NOT NULL

),

streak_calc AS (

SELECT *,

SUM(CASE WHEN is_beat = 0 THEN 1 ELSE 0 END)

OVER (PARTITION BY symbol ORDER BY recency_rank

ROWS UNBOUNDED PRECEDING) AS streak_breaker

FROM ordered_earnings

),

streaks AS (

SELECT

symbol,

COUNT(*) AS current_streak,

ROUND(AVG(surprise_pct), 1) AS avg_surprise_pct,

MIN(event_date) AS streak_start,

MAX(event_date) AS latest_beat

FROM streak_calc

WHERE streak_breaker = 0 AND is_beat = 1

GROUP BY symbol

HAVING COUNT(*) >= 3

)

SELECT

s.symbol,

s.current_streak,

s.avg_surprise_pct,

s.streak_start,

s.latest_beat,

ROUND(k.marketCap / 1e9, 1) AS mktcap_bn_usd

FROM streaks s

JOIN key_metrics k ON s.symbol = k.symbol AND k.period = 'FY'

WHERE k.marketCap > 500000000

QUALIFY ROW_NUMBER() OVER (PARTITION BY s.symbol ORDER BY k.date DESC) = 1

ORDER BY s.current_streak DESC, s.avg_surprise_pct DESC

LIMIT 30

The streak_breaker column is the key mechanism. Earnings are ordered from most recent to oldest. Each time a miss appears (is_beat = 0), the running sum increments. Any row where streak_breaker = 0 means we haven't encountered a miss going backward from the most recent report, those rows form the current active streak.

The query filters to TAI and TWO exchanges and requires a market cap above $500M USD (roughly TWD 15B) to focus on companies with enough liquidity to act on.

Run this screen live on Ceta Research → (pre-loaded query, no account required)

Why It Works

Two papers provide the theoretical grounding for beat-streak effects.

Loh & Warachka (2012), "Streaks in Earnings Surprises and the Cross-Section of Stock Returns" showed that consecutive earnings surprise streaks predict future stock returns. Their central finding: investors treat each beat as a mostly independent event rather than recognizing the pattern. The streak carries information the market under-weights, producing predictable return drift in the direction of the streak. This under-reaction is larger in stocks with lower analyst coverage and higher uncertainty, precisely the conditions that describe many Taiwanese mid-caps outside the major semiconductor names.

Myers, Myers & Skinner (2007), "Earnings Momentum and Earnings Management" documented the other side of the story. Companies with long beat streaks actively manage expectations downward to maintain them. Conservative guidance ensures beatable targets. The practical implication: at short streak lengths (2–3), the signal reflects genuine fundamental momentum. At very long streak lengths (5+), expectation management increasingly contaminates the signal. This aligns well with Taiwan's data, where streak_3 outperforms streak_5+ significantly.

The Taiwan data fits the Loh & Warachka framework well. The prolonged drift (peaking at T+21, not T+1) suggests the market is slow to incorporate streak information into prices, consistent with under-reaction being the primary mechanism.

Limitations

Benchmark mismatch. SPY is used as the benchmark because no Taiwan-specific ETF is available in the framework. Abnormal returns here measure performance versus the US market, not the Taiwanese market. In periods when TWSE significantly outperforms or underperforms the S&P 500, this creates noise in the CAR estimates. A Taiwan-focused index (e.g., EWT) would be more appropriate but wasn't available for the full 2012–2025 window in a comparable daily format. Treat the CAR figures as directional, not precise.

Sample concentration. Taiwan's listed universe skews heavily toward tech, semiconductors, and electronics. Beat streaks in this data may reflect sector-specific dynamics rather than a general Taiwan market phenomenon. The results might not generalize to Taiwanese companies in other industries.

Exchange coverage. Both TAI (TWSE main board) and TWO (TPEX) are included. Coverage quality is better for larger TWSE names. Smaller TWO companies may have thinner analyst coverage, which affects both the quality of estimates and the reliability of beat/miss classifications.

Expectations management at streak_5+. The flat-to-negative T+63 return for very long streaks suggests these companies may be managing estimates actively. We can't distinguish genuine outperformance from sandbagging in the raw data.

Takeaway

Taiwan's beat-streak signal is real and statistically robust. The T+21 return of +1.79% is among the strongest globally, and it's driven primarily by post-announcement drift rather than the immediate reaction. The market prices in some of the beat on day 1 but keeps updating for three weeks.

The practical focus should be streak_3 events. A third consecutive beat in a Taiwanese company produces a +2.60% T+21 CAR and +2.75% T+63 CAR, numbers that hold up relative to other major markets. Streak_5+ events, by contrast, show no meaningful drift by T+63. The signal has already been absorbed.

For investors with Taiwan exposure, beat streaks offer a systematic signal worth monitoring, with the caveat that SPY-benchmarked abnormal returns should be interpreted relative to the US-Taiwan performance differential in any given period.

Part of a series: Beat streaks analyzed across 16 exchanges. See US, Canada, Japan, Taiwan, India, Brazil, and the global comparison.

Data: TradingStudio (FMP earnings data). Event study uses earnings_surprises + stock_eod + key_metrics tables with market cap > TWD 10B filter applied at the time of each event. Abnormal returns computed vs SPY benchmark. FMP data limitations: analyst estimate coverage varies by exchange and time period, estimate quality may be lower for smaller companies, and historical records for TAI/TWO are less complete than for US exchanges. Beat streaks depend on estimate availability. Past performance does not guarantee future results. This is educational content, not investment advice.

References

- Loh, R. & Warachka, M. (2012). "Streaks in Earnings Surprises and the Cross-Section of Stock Returns." Management Science, 58(7), 1305–1321.

- Myers, L., Myers, J. & Skinner, D. (2007). "Earnings Momentum and Earnings Management." Journal of Accounting, Auditing & Finance, 22(2), 249–284.