Beat Streaks Work Globally — With Exceptions: 16 Exchanges Compared

We tested earnings beat streaks across 16 exchanges covering 102,577 streak events. 12 of 16 exchanges show positive T+21 CAR. India leads at +2.10% T+21 but with recent data caveat. Thailand shows negative drift. The immediate T+1 reaction is positive on every exchange tested.

Earnings beat streaks produce statistically significant post-announcement drift in 10 of the 16 exchanges we tested. The immediate reaction is universal. The 63-day drift is not. This is an honest look at where the signal holds, where it fades, and where it runs in reverse.

Contents

- The Setup

- The Global Picture

- Winners: Where Beat Streaks Work Best

- The India Caveat

- Counter-Evidence: Thailand

- The Pattern That Holds Everywhere

- Limitations

- Takeaway

The Setup

A beat streak is a sequence of two or more consecutive quarters where a company's reported EPS exceeds analyst estimates. We define a beat as epsActual > epsEstimated where ABS(epsEstimated) > 0.01, which filters near-zero estimates that carry no real information.

For each streak-extending announcement, we measure the cumulative abnormal return (CAR) at T+1, T+21, and T+63 trading days. CAR is the stock's return minus a regional benchmark ETF return over that window. T+0 is excluded to avoid confounding intraday moves.

Exchanges covered: US, Canada, Japan, Taiwan, India, Brazil, Hong Kong, Germany, UK, Korea, Australia, Norway, Sweden, Switzerland, China, and Thailand. Market cap floors applied per exchange in local currency. Total events: roughly 108,000 across all 16 markets.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

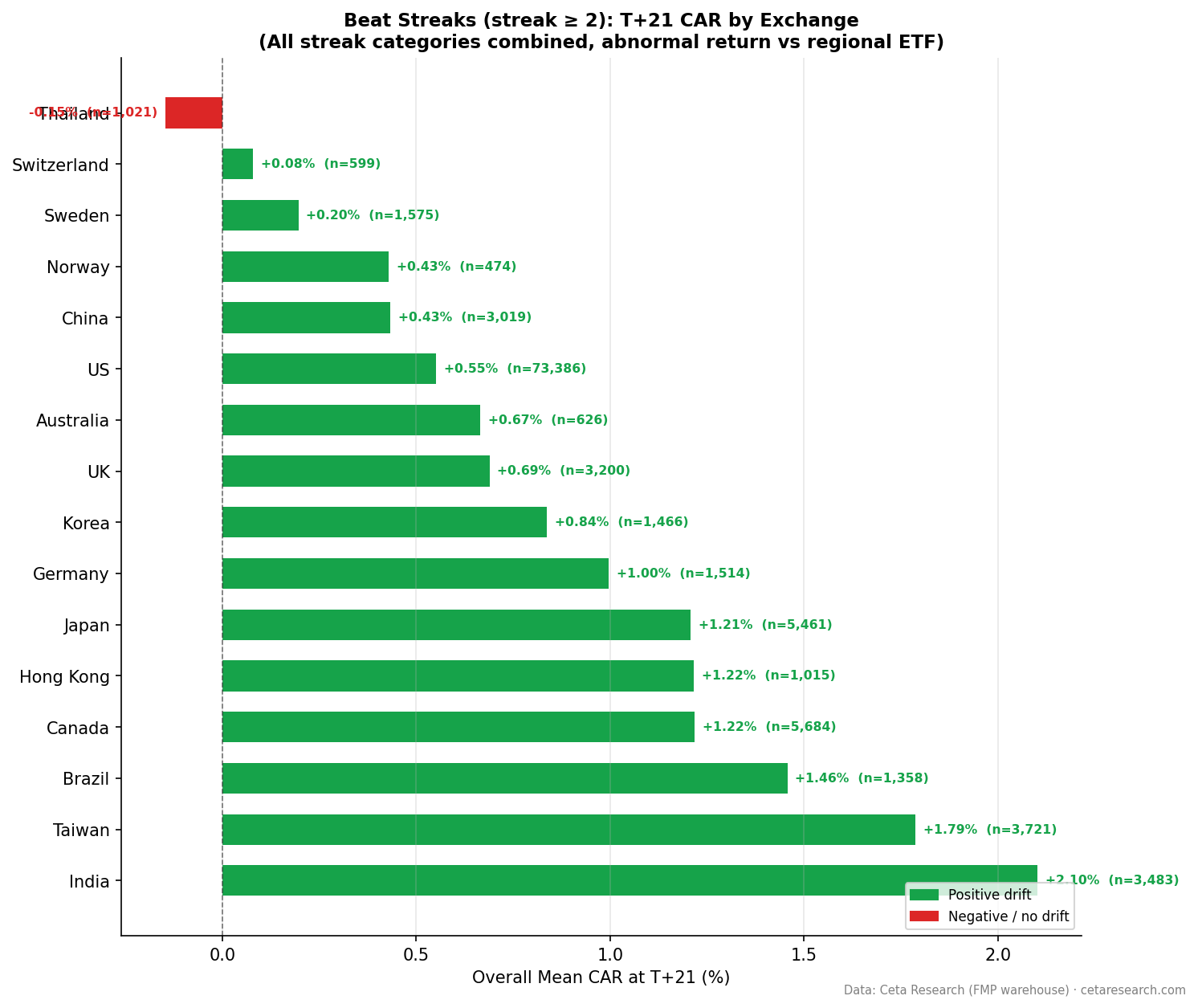

The Global Picture

The T+1 reaction is positive on every exchange we tested. Every single one. Including Thailand, where the longer-term drift runs negative. That tells you something: the market's immediate recognition that a streak has extended is a global phenomenon, not a US-specific artifact.

Beyond T+1, the picture diverges. Ten exchanges show statistically significant T+21 drift at p<0.01. Four more are significant at p<0.05 or trending. Only Thailand posts negative T+21 and T+63 drift.

The big split is between markets with 20+ years of clean data versus markets where effective coverage starts post-2020. US and Canada have 25-year records. Japan runs from 2009. Everyone else varies, and for India, Germany, UK, Australia, and Hong Kong, 88 to 98 percent of events are from 2020 onward. Those results tell you about the current regime, not a structural market property.

| Exchange | Events | T+1 CAR | T+21 CAR | T+63 CAR | t(21) | Sig | Data Quality |

|---|---|---|---|---|---|---|---|

| India | 3,483 | +0.58% | +2.10% | +5.05% | 12.59 | ** | 95% from 2022+ |

| Taiwan | 3,721 | +0.49% | +1.79% | +1.20% | 9.43 | ** | 2012+ |

| Brazil | 1,358 | +0.30% | +1.46% | +2.49% | 4.88 | ** | 2015+ |

| Canada | 5,684 | +0.83% | +1.22% | +1.76% | 10.15 | ** | 2000+ (25yr) |

| Hong Kong | 1,015 | +0.69% | +1.22% | +2.84% | 3.11 | ** | 88% from 2020+ |

| Japan | 5,461 | +0.90% | +1.21% | +1.47% | 9.85 | ** | 2009+ |

| Germany | 1,514 | +0.31% | +1.00% | +0.68% | 3.88 | ** | 96% from 2020+ |

| UK | 3,200 | +0.44% | +0.69% | +0.53% | 4.07 | ** | 93% from 2020+ |

| Korea | 1,466 | +0.57% | +0.84% | +0.60% | 2.99 | ** | 2016+ |

| US | 73,386 | +0.52% | +0.55% | +0.31% | 14.83 | ** | 2000+ (25yr) |

| Australia | 626 | +0.24% | +0.67% | +0.93% | 1.73 | NS | 98% from 2020+ |

| Norway | 474 | +0.40% | +0.43% | +1.29% | 1.15 | NS | 2021+ |

| Sweden | 1,575 | +0.30% | +0.20% | +0.22% | 0.94 | NS | 2015+ |

| Switzerland | 599 | +0.11% | +0.08% | +0.63% | 0.22 | NS | 2021+ |

| China | 3,019 | +0.75% | +0.43% | +1.28% | 2.01 | * | 2015+ |

| Thailand | 1,021 | +0.42% | -0.15% | -1.26% | -0.50 | NS | 2017+ |

Sig: ** = p<0.01, * = p<0.05, NS = not significant

Winners: Where Beat Streaks Work Best

Canada is the most credible outperformer. Five-thousand-plus events over 25 years, with T+21 drift at +1.22% and T+63 at +1.76%. The US T+63 result is +0.31%. Canada is nearly six times larger. The reason isn't mysterious: lower analyst coverage per stock, a resource-heavy sector mix where earnings are genuinely hard to forecast, and less institutional arbitrage capacity. The drift window stays open longer because fewer market participants are positioned to close it quickly.

Japan is the other long-running signal worth taking seriously. 5,461 events from 2009 onward, T+21 at +1.21%, t-stat of 9.85. Japan had a reputation for weak earnings discipline until the TSE governance reforms began in earnest. The beat streak data suggests that when Japanese companies do sustain a streak, the market is slow to reprice. Corporate governance improvements may have actually increased the signal's reliability, as genuine outperformance became easier to distinguish from managed earnings.

Taiwan stands out for a different reason: the streak length pattern. The third consecutive beat (+2.60% T+21) is the strongest single streak-length result of any exchange. That means the market under-reacts most severely at precisely the point where the streak has been confirmed multiple times. It's the opposite of what you'd expect if investors were fully extrapolating the streak forward.

| Exchange | Streak 2 | Streak 3 | Streak 4 | Streak 5+ |

|---|---|---|---|---|

| US | +0.77% | +0.56% | +0.62% | +0.42% |

| Canada | +1.33% | +1.65% | +0.43% | +1.12% |

| Japan | +1.47% | +1.34% | +0.82% | +0.92% |

| Taiwan | +1.55% | +2.60% | +1.57% | +1.53% |

| India | +2.65% | +1.99% | +1.28% | +1.66% |

| Brazil | +1.19% | +2.53% | +1.55% | +1.06% |

T+21 CAR by streak length, selected exchanges.

The streak 3 effect in Taiwan (+2.60%), Brazil (+2.53%), and Canada (+1.65%) is notable across all three markets. The first repeat is easy to explain as a beat. The third consecutive beat carries more conviction about underlying fundamentals, and the market seems to lag in recognizing that.

The India Caveat

India's numbers are extraordinary. T+21 at +2.10%, T+63 at +5.05%, t-stat of 12.59. If those numbers are right, this is the strongest beat streak signal in the world by a wide margin.

The caveat is substantial. Ninety-five percent of India's 3,483 events are from 2022 onward. The Indian market had a prolonged bull run during that period. The +5.05% T+63 result almost certainly reflects, at least in part, the broader market tailwind rather than a clean beat-streak effect. The abnormal return calculation subtracts a benchmark, but if the benchmark itself underrepresents the domestic bull market dynamics for specific stock categories, the residual looks larger than it is.

This isn't a reason to dismiss the India result. The t-stat is 12.59. Something real is happening. But extrapolating this as a 25-year structural property of the Indian market would be wrong. It's a finding about how beat streaks behaved during one of India's strongest recent bull periods. As longer time-series data accumulates, the picture will sharpen.

For now: India is a promising signal with a data quality asterisk that matters.

Counter-Evidence: Thailand

Thailand has positive T+1 drift (+0.42%). Then the signal dies. T+21 is -0.15%. T+63 is -1.26%. The t-stat at T+21 is -0.50, which is not significant, but the direction is consistent: beat streaks in Thailand have produced negative subsequent returns in our sample.

The most likely explanation is benchmark mismatch. No liquid Thai equity ETF with sufficient history was available, so SPY was used as the benchmark for Thailand, as it was for Taiwan. For Taiwan, US tech correlation made SPY a reasonable proxy. For Thailand, which is more domestically driven and less correlated with US markets, SPY is a poor benchmark. The "abnormal return" calculation may be stripping out a genuine return that should be there because the benchmark is wrong.

The alternative explanation: the Thai market genuinely doesn't respond to beat streaks in the expected direction. This could reflect analyst estimate quality, earnings management practices, or market microstructure that leads to price reversals after the initial reaction.

We don't have enough data to distinguish these explanations. What we can say is that Thailand doesn't belong in a beat-streak strategy without further investigation, and that SPY is probably the wrong benchmark for it.

The Pattern That Holds Everywhere

T+1 is positive across all 16 exchanges. This is the one universal result.

It means the initial market reaction to a streak-extending beat is consistently positive regardless of exchange, region, market structure, or data quality. Even in Thailand, where longer-term drift is negative, the one-day reaction is +0.42%. Even in Sweden and Switzerland, where T+21 and T+63 show almost no signal, T+1 is +0.30% and +0.11%.

This matters for two reasons. First, it suggests the immediate price response is driven by a behavioral mechanism that applies across markets: investors are positively surprised when a streak extends, and that surprise gets priced in quickly. Second, it means short-term traders have a more reliable signal than longer-term investors, but the edge window is narrow. Earnings are announced after hours. The open the next morning is often where the move happens, and getting a fill at favorable prices is harder than the T+1 CAR implies.

The T+63 drift is where markets diverge. The US has +0.31%, compressed by institutional arbitrage. Canada has +1.76%, still building. India shows +5.05% in a regime-specific sample. And Thailand reverses. The longer you hold, the more the local market structure and data quality determine your outcome.

Limitations

Recent-regime dominance: India, Germany, UK, Australia, and Hong Kong all have 88 to 98 percent of events from 2020 or later. Their results reflect post-COVID market conditions, not multi-decade structural properties. Treat them as current-regime estimates.

Benchmark mismatches: SPY is used for Taiwan and Thailand. For Taiwan, this is a reasonable approximation given tech sector correlation. For Thailand, it's a poor fit. The Thailand result should be treated skeptically for this reason. Regional ETFs were used where available (EWC for Canada, EWJ for Japan, EWT for Taiwan where SPY is the fallback).

Sample sizes in non-US markets: Several exchanges have 500 to 1,500 events in total. Subcategory analysis (by streak length) within those samples carries real uncertainty. The t-stats at T+21 for Australia (1.73) and Norway (1.15) are below conventional significance thresholds. More data would sharpen the picture.

Coverage periods: Effective start dates vary from 2000 (US, Canada) to 2021 (Norway, Switzerland). Markets with shorter histories may look better or worse than they would over a full cycle.

Survivorship bias: Stocks that delisted due to failure are underrepresented across all exchanges. CARs are biased upward as a result.

Takeaway

The global evidence on beat streaks is cleaner than expected. Ten of 16 exchanges show statistically significant T+21 drift at p<0.01. The mechanism appears to be global: markets consistently under-react to the information embedded in continuing beat streaks.

The practical implications differ by context. For investors in US markets, the T+21 signal is real but compressed to +0.55%. For Canadian and Japanese markets, the same event produces 2x the drift with comparable statistical reliability and much longer histories. For Taiwan and Brazil, streak 3 is the highest-conviction entry point.

Markets with recent-only data (India, Germany, UK, Hong Kong) show strong signals, but those signals haven't been tested through a full cycle. Take them seriously as current-regime findings, not confirmed structural properties.

Sweden and Switzerland produced no reliable signal despite adequate sample sizes. Not every developed market responds to beat streaks. The signal requires a particular combination of analyst coverage levels, market microstructure, and information dissemination speed. Those conditions don't exist everywhere.

Thailand is the clearest counter-evidence. Something is wrong there, either the benchmark or the market itself. Don't build a strategy on it without investigating the benchmark problem first.

The T+1 result, though, is as reliable as anything in this data. If you can execute around earnings announcements efficiently, the one-day signal is the cleanest and most universal finding in this study.

This is the global comparison blog. See dedicated analyses for US, Canada, Japan, Taiwan, India, and Brazil.

Data: Ceta Research (FMP warehouse). Beat streaks computed on earnings_surprises table using DuckDB window functions. Abnormal returns vs regional ETF benchmarks (SPY for Taiwan and Thailand where regional ETF unavailable). Market cap filters applied per exchange in local currency. Analysis period: 2000–2025 (exchange-specific effective start dates in table).

Past performance does not guarantee future results. This is educational content, not investment advice.