Compounding Equity Screen UK: 8.03% CAGR, +6.80% Excess vs FTSE 100

We backtested the Compounding Equity Screen on London Stock Exchange stocks from 2000 to 2025. 8.03% CAGR vs 1.23% for the FTSE 100, with 13.2% down capture. During the 2008 financial crisis, the portfolio fell 10% while the FTSE fell 22%.

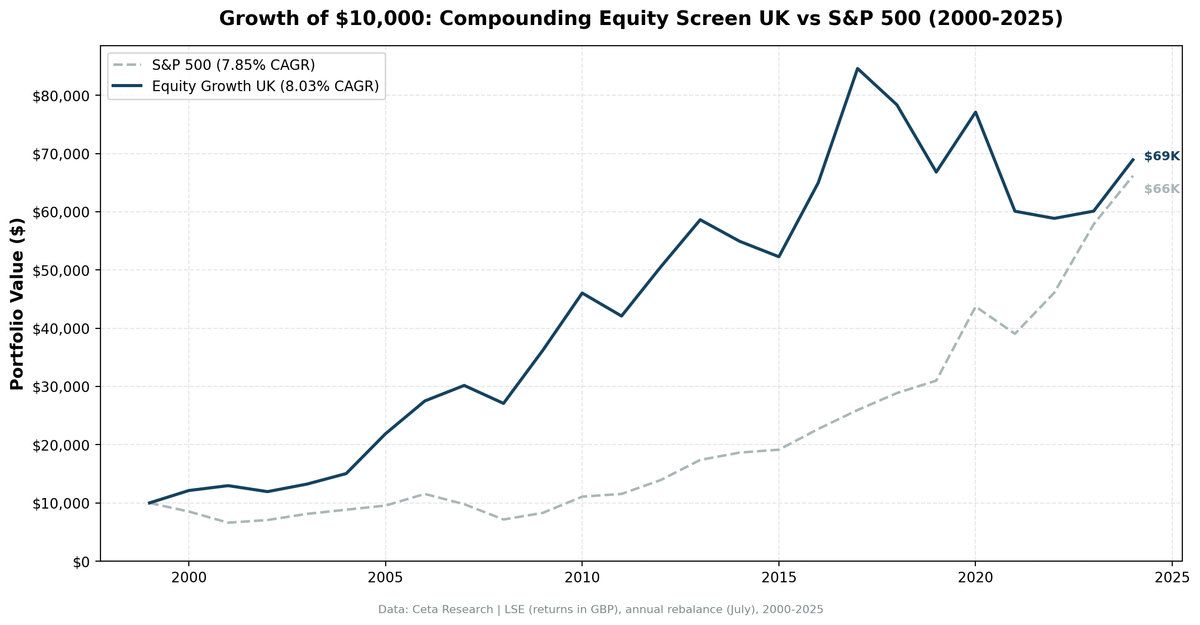

We backtested the Compounding Equity Screen on London Stock Exchange stocks from 2000 to 2025. The portfolio returned 8.03% annually vs 1.23% for the FTSE 100. That +6.80% annual excess compounds into a different outcome entirely: $10,000 grew to $68,900 vs $13,600 for the FTSE 100.

Contents

- Method

- The Signal

- What Research Shows

- The Screen

- Simple Screen (SQL)

- Advanced Screen (SQL)

- Results

- When It Works: Crisis Protection

- When It Fails

- Full Annual Returns

- Limitations

- Run It Yourself

- Backtest

- Takeaway

- References

The excess return is the story. So is the risk profile.

During the 2008 financial crisis, the portfolio fell 10% while the FTSE 100 fell 22%, a +11.8% excess. During the dot-com crash in 2000, UK equity compounders gained 21.3% while the FTSE lost 11.7%. Over 25 years, the portfolio captured only 13.2% of the FTSE's downside. A strategy that compounds book value in both good and bad markets turns out to hold up when the bad markets arrive.

Data: FMP financial data warehouse, 2000-2025. Updated July 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: London Stock Exchange (LSE), market cap > £500M Period: 2000-2025 (25 annual rebalance periods) Rebalancing: Annual (July), equal weight top 30 by highest equity CAGR Benchmark: FTSE 100 (^FTSE), returns in GBP Cash rule: Hold cash if fewer than 10 stocks qualify Transaction costs: Size-tiered model (0.1% mega-cap, 0.3% large-cap, 0.5% mid-cap) Data quality guards: Entry price > £1, single-period return capped at 200%

Financial data uses a 45-day lag from the rebalance date for point-in-time correctness. Full methodology: backtests/METHODOLOGY.md

The Signal

A company's shareholders' equity grows when it retains more earnings than it pays out. Consistent 10%+ equity CAGR over five years means the company is both profitable and disciplined about capital. It generates more than its cost of capital and deploys it back into the business.

The signal: find companies that have been compounding their own book value for five consecutive years, then buy the ones doing it fastest.

Filters:

| Criterion | Metric | Threshold | Why |

|---|---|---|---|

| Value creation | Shareholders' equity CAGR (5yr) | > 10% | Core compounding signal |

| Quality overlay | Return on Equity (TTM) | > 8% | Growth from operations, not dilution |

| Quality overlay | Operating Profit Margin (TTM) | > 8% | Pricing power, operational efficiency |

| Liquidity | Market Cap | > £500M | Investable stocks only |

Ranking: Top 30 by equity CAGR descending, equal weight. The 5-year CAGR window accepts 3.5 to 7.0 years to handle data gaps and irregular filing schedules, targeting the closest available filing to 5 years prior.

What Research Shows

Warren Buffett used book value per share CAGR as his primary metric for measuring Berkshire's intrinsic value growth for decades. The logic is direct: if retained earnings are deployed at returns above the cost of capital, book value grows and intrinsic value follows.

Asness, Frazzini and Pedersen (2019) in Quality Minus Junk show that consistent equity growth is a reliable quality signal. It separates businesses with durable competitive advantages from cyclical compounders and leveraged growers. The Gordon Growth Model formalizes it: sustainable growth rate = ROE × (1 − payout ratio). Companies compounding equity at 10%+ either have high ROE or high retention, both positive signals.

The UK market has historically been fertile ground for this signal. LSE is structurally different from US exchanges: less technology concentration, more consumer staples, industrials, and financial services. These sectors compound book value steadily rather than through burst-growth cycles. The result is a more predictable compounding profile that holds up under stress.

The Screen

Simple Screen (SQL)

WITH curr_eq AS (

SELECT symbol, totalStockholdersEquity AS eq_curr, dateEpoch AS epoch_curr,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY dateEpoch DESC) AS rn

FROM balance_sheet

WHERE period = 'FY' AND totalStockholdersEquity > 0

),

prior_5yr AS (

SELECT c.symbol,

b.totalStockholdersEquity AS eq_prior,

(c.epoch_curr - b.dateEpoch) / 31536000.0 AS years_gap,

POWER(

c.eq_curr / b.totalStockholdersEquity,

1.0 / ((c.epoch_curr - b.dateEpoch) / 31536000.0)

) - 1 AS eq_cagr,

ROW_NUMBER() OVER (

PARTITION BY c.symbol

ORDER BY ABS((c.epoch_curr - b.dateEpoch) / 31536000.0 - 5) ASC

) AS best_match

FROM curr_eq c

JOIN balance_sheet b ON c.symbol = b.symbol AND c.rn = 1

AND b.period = 'FY' AND b.totalStockholdersEquity > 0

AND b.dateEpoch < c.epoch_curr - 4 * 31536000

AND b.dateEpoch > c.epoch_curr - 7 * 31536000

)

SELECT pr.symbol, p.companyName,

ROUND(pr.eq_cagr * 100, 2) AS eq_cagr_pct,

ROUND(pr.years_gap, 1) AS years_measured,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM prior_5yr pr

JOIN profile p ON pr.symbol = p.symbol

JOIN key_metrics_ttm k ON pr.symbol = k.symbol

WHERE pr.best_match = 1 AND pr.years_gap BETWEEN 3.5 AND 7.0

AND pr.eq_cagr > 0.10

AND p.exchange = 'LSE'

ORDER BY pr.eq_cagr DESC

LIMIT 30

This returns LSE stocks ranked by 5-year equity CAGR. The problem: it includes companies that grew equity through acquisitions or share issuances rather than operational earnings.

Advanced Screen (SQL)

WITH curr_eq AS (

SELECT symbol, totalStockholdersEquity AS eq_curr, dateEpoch AS epoch_curr,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY dateEpoch DESC) AS rn

FROM balance_sheet

WHERE period = 'FY' AND totalStockholdersEquity > 0

),

prior_5yr AS (

SELECT c.symbol,

b.totalStockholdersEquity AS eq_prior,

(c.epoch_curr - b.dateEpoch) / 31536000.0 AS years_gap,

POWER(

c.eq_curr / b.totalStockholdersEquity,

1.0 / ((c.epoch_curr - b.dateEpoch) / 31536000.0)

) - 1 AS eq_cagr,

ROW_NUMBER() OVER (

PARTITION BY c.symbol

ORDER BY ABS((c.epoch_curr - b.dateEpoch) / 31536000.0 - 5) ASC

) AS best_match

FROM curr_eq c

JOIN balance_sheet b ON c.symbol = b.symbol AND c.rn = 1

AND b.period = 'FY' AND b.totalStockholdersEquity > 0

AND b.dateEpoch < c.epoch_curr - 4 * 31536000

AND b.dateEpoch > c.epoch_curr - 7 * 31536000

)

SELECT pr.symbol, p.companyName, p.sector,

ROUND(pr.eq_cagr * 100, 2) AS eq_cagr_pct,

ROUND(pr.years_gap, 1) AS years_measured,

ROUND(k.returnOnEquityTTM * 100, 2) AS roe_pct,

ROUND(f.operatingProfitMarginTTM * 100, 2) AS opm_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM prior_5yr pr

JOIN profile p ON pr.symbol = p.symbol

JOIN key_metrics_ttm k ON pr.symbol = k.symbol

JOIN financial_ratios_ttm f ON pr.symbol = f.symbol

WHERE pr.best_match = 1 AND pr.years_gap BETWEEN 3.5 AND 7.0

AND pr.eq_cagr > 0.10 AND pr.eq_cagr < 1.00

AND k.returnOnEquityTTM > 0.08

AND f.operatingProfitMarginTTM > 0.08

AND k.marketCap > 500000000

AND p.exchange = 'LSE'

AND p.isActivelyTrading = true

ORDER BY pr.eq_cagr DESC

LIMIT 30

The ROE filter removes companies that grew equity through new share issuances rather than retained earnings. The operating margin filter removes low-quality compounders with thin economics. What remains is a set of LSE companies that have been earning real returns on capital and reinvesting them for five consecutive years.

Results

| Metric | Portfolio | FTSE 100 |

|---|---|---|

| CAGR | 8.03% | 1.23% |

| Total Return | 589% | 36% |

| Max Drawdown | -30.4% | -22.0% |

| Volatility | 17.1% | -- |

| Sharpe Ratio | 0.265 | -- |

| Sortino Ratio | 0.539 | -- |

| Calmar Ratio | 0.264 | -- |

| Down Capture | 13.2% | -- |

| Up Capture | 152.1% | -- |

| Win Rate (vs FTSE) | 68% (17/25) | -- |

| Cash Periods | 0/25 | -- |

| Avg Stocks | ~11 | -- |

$10,000 invested in July 2000 grew to $68,900. The same $10,000 in the FTSE 100 grew to $13,600. The portfolio captured 152.1% of the upside and only 13.2% of the downside.

The Calmar ratio (CAGR divided by max drawdown) is 0.264 vs a FTSE 100 that barely grew at all. The Sortino ratio of 0.539 confirms the portfolio delivered meaningful return per unit of downside deviation. With 13.2% down capture, the portfolio absorbed roughly an eighth of the FTSE's declines while capturing more than 150% of its gains.

When It Works: Crisis Protection

The portfolio's most valuable property is what it does in bad markets: it falls less.

2000-2002 (Dot-Com Bust): While the FTSE 100 lost 38% cumulative over three years, UK equity compounders gained 21.3% in year one, added another 6.9% in year two, and gave back just 7.9% in year three.

| Year | Portfolio | FTSE 100 | Excess |

|---|---|---|---|

| 2000 | +21.3% | -11.7% | +33.0% |

| 2001 | +6.9% | -20.5% | +27.4% |

| 2002 | -7.9% | -11.9% | +4.0% |

Companies that had been growing book value steadily for five years had little exposure to the speculative tech expansion that was unwinding. Their earnings were real, their equity bases were solid, and their share prices reflected fundamentals rather than momentum.

2008 (Financial Crisis): The portfolio fell 10% while the FTSE 100 fell 22%. Down capture of 13.2% means the portfolio absorbed roughly an eighth of the benchmark's losses.

| Year | Portfolio | FTSE 100 | Excess |

|---|---|---|---|

| 2008 | -10.2% | -22.0% | +11.8% |

The portfolio lost ground, but much less than the market. These were businesses generating returns above cost of capital in sectors not fully exposed to leverage or financial contagion. The quality filter limited the damage.

2009 (Recovery): The portfolio then captured the full recovery and more.

| Year | Portfolio | FTSE 100 | Excess |

|---|---|---|---|

| 2009 | +33.7% | +14.3% | +19.4% |

Mid-Period Run (2004-2017): A sustained outperformance period, including standout years in 2005 and 2017.

| Year | Portfolio | FTSE 100 | Excess |

|---|---|---|---|

| 2005 | +45.5% | +13.5% | +32.0% |

| 2010 | +27.1% | +24.4% | +2.7% |

| 2012 | +20.1% | +11.8% | +8.4% |

| 2016 | +24.3% | +13.1% | +11.2% |

| 2017 | +30.2% | +2.3% | +27.9% |

When It Fails

2021-2023 (Post-COVID Rotation): The strategy's weakest period. The portfolio lost 22.1% in 2021 while the FTSE gained 1.5%, then continued to lag in 2022-2023.

| Year | Portfolio | FTSE 100 | Excess |

|---|---|---|---|

| 2021 | -22.1% | +1.5% | -23.6% |

| 2022 | -2.0% | +4.1% | -6.1% |

| 2023 | +2.1% | +7.9% | -5.8% |

All returns are July-to-July. The 2021-2023 period saw a rotation into energy and large-cap value names that dominate the FTSE 100 index. UK equity compounders, predominantly in industrials and services, didn't participate in this repricing. The portfolio generated flat-to-small gains while the FTSE rallied on commodity prices and bank earnings.

This isn't a strategy failure. It's a style rotation. A portfolio that captures only 13.2% of the FTSE's downside also misses sector-specific rallies it has no exposure to. That's the trade-off.

2014-2015 (Commodity Downturn): Broad LSE weakness weighed on quality compounders too.

| Year | Portfolio | FTSE 100 | Excess |

|---|---|---|---|

| 2014 | -6.3% | -2.7% | -3.6% |

| 2015 | -4.8% | -1.6% | -3.2% |

Fundamentals remained intact but re-rating compressed returns.

Full Annual Returns

| Year | Portfolio | FTSE 100 | Excess |

|---|---|---|---|

| 2000 | +21.3% | -11.7% | +33.0% |

| 2001 | +6.9% | -20.5% | +27.4% |

| 2002 | -7.9% | -11.9% | +4.0% |

| 2003 | +10.8% | +10.0% | +0.8% |

| 2004 | +13.7% | +17.6% | -3.9% |

| 2005 | +45.5% | +13.5% | +32.0% |

| 2006 | +25.7% | +12.0% | +13.7% |

| 2007 | +9.7% | -17.7% | +27.3% |

| 2008 | -10.2% | -22.0% | +11.8% |

| 2009 | +33.7% | +14.3% | +19.4% |

| 2010 | +27.1% | +24.4% | +2.7% |

| 2011 | -8.6% | -6.3% | -2.3% |

| 2012 | +20.1% | +11.8% | +8.4% |

| 2013 | +16.0% | +8.1% | +7.8% |

| 2014 | -6.3% | -2.7% | -3.6% |

| 2015 | -4.8% | -1.6% | -3.2% |

| 2016 | +24.3% | +13.1% | +11.2% |

| 2017 | +30.2% | +2.3% | +27.9% |

| 2018 | -7.4% | +0.2% | -7.5% |

| 2019 | -14.7% | -17.5% | +2.7% |

| 2020 | +15.4% | +14.2% | +1.3% |

| 2021 | -22.1% | +1.5% | -23.6% |

| 2022 | -2.0% | +4.1% | -6.1% |

| 2023 | +2.1% | +7.9% | -5.8% |

| 2024 | +14.7% | +8.1% | +6.6% |

Note: All returns measured July-to-July (rebalance period). FTSE 100 returns in GBP.

Limitations

Concentration in about 11 stocks. The average portfolio held roughly 11 stocks, far smaller than the 25-30 common in US screens. Equal weighting at this size means a single holding carries close to 9% weight, and in some years the screen barely cleared the 10-stock minimum. For large institutional allocations, this creates capacity constraints.

GBP returns. The screen and benchmark both run in GBP, so the comparison is clean. For USD-based investors, GBP/USD fluctuations add another layer of volatility and can compress or amplify returns by several percentage points per year.

Annual rebalancing lag. Rebalancing in July means the portfolio holds positions for a full year after formation. Companies can deteriorate between rebalances. Quarterly rebalancing would cost more in transaction fees without a clear improvement in the signal, since equity CAGR changes slowly.

No momentum tilt. The screen ranks by equity CAGR, not recent price performance. Strong momentum names may not appear. The 2021-2023 underperformance partly reflects this: sector rotations into energy and large-cap FTSE names bypassed the quality compounders in the portfolio.

Survivorship bias. Historical results are based on companies that existed and reported throughout the test period. Companies that went bankrupt or were acquired have limited impact due to data availability constraints, but this creates mild survivorship bias in early periods.

Run It Yourself

Run this screen live on Ceta Research →

Backtest

git clone https://github.com/ceta-research/backtests.git

cd backtests

# UK backtest

python3 equity-growth/backtest.py --preset uk --output results.json --verbose

# All exchanges

python3 equity-growth/backtest.py --global --output results/exchange_comparison.json

Takeaway

UK equity compounders delivered 8.03% CAGR over 25 years, outperforming the FTSE 100 by +6.80% annually. The portfolio beat the FTSE in 17 of 25 years (68% win rate) and captured only 13.2% of its downside.

The portfolio fell in bad years. It lost 10% in 2008 and 22% in 2021. But it fell less than the FTSE in most downturns and recovered faster. The signal isn't obscure: find companies that have been growing their own book value at 10%+ per year for five years, confirm the growth came from operations (not financial engineering), and hold them until next July.

Of the 14 exchanges tested, the UK showed consistent outperformance against its local benchmark. That's not a marketing claim. The other 13 exchanges are in the global comparison. UK equity structure, the dominance of non-tech quality compounders, and LSE's historical mix of sectors explain why the signal works here when it doesn't elsewhere.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Universe: London Stock Exchange (LSE). Returns in GBP. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results. This is educational content, not investment advice.

References

- Asness, C., Frazzini, A. & Pedersen, L. (2019). "Quality Minus Junk." Review of Accounting Studies, 24(1), 34-112.

- Buffett, W. (1977-2023). Berkshire Hathaway Annual Letters. Book value per share CAGR as primary performance metric.

- Gordon, M. & Shapiro, E. (1956). "Capital Equipment Analysis: The Required Rate of Profit." Management Science, 3(1), 102-110. Sustainable growth rate = ROE × (1 − payout ratio).

- Cooper, M., Gulen, H. & Schill, M. (2008). "Asset Growth and the Cross-Section of Stock Returns." Journal of Finance, 63(4), 1609-1651.