Corporate Spinoffs: Children Return +8% Above SPY After One Year, But Half the Edge Comes From 5 Stocks

We tracked 30 major US corporate spinoffs (2011-2024) at six time horizons. The forced-selling effect is real and statistically confirmed at T+5 (-3.5%, p<0.05). The long-run recovery is positive but driven by outliers — GEV +108%, REZI -68%. Full data and SQL included.

When a large company spins off a division, index funds that owned the parent receive shares of the child entity. If the child is too small for the S&P 500, passive funds must sell, not because the business is bad, but because their mandate requires it. This forced selling depresses the child's price temporarily. Over subsequent months, fundamental investors step in and the price recovers.

Contents

- Method

- The Academic Baseline

- Results: Spinoff Children

- Results: Spinoff Parents

- The Outlier Problem

- What This Means for Spinoff Investing

- The Screen Today

- Limitations

- Takeaway

- References

The parent benefits too. A focused company typically trades at a higher multiple than a conglomerate. The "conglomerate discount" disappears once the division is separated.

That's the theory. We tested it on 30 major US corporate spinoffs from 2011 to 2024, tracking both parent and child performance at six time horizons after the separation. All returns are measured from the next-day close (the first price a real investor could execute at after learning about the spinoff), not the event-date close.

The results are more nuanced than the academic literature suggests, but more promising than our initial analysis showed.

Data: FMP financial data warehouse, 2000–2025. Updated April 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Event list: Curated from SEC filings, press releases, and public records (30 confirmed spinoffs, 2011-2024) Price data: stock_eod (adjusted close prices) Benchmark: SPY Execution: Next-day close (MOC). Entry price is the close on the first trading day after the spinoff event, not the event-date close. This reflects the earliest realistic execution for an investor reacting to the spinoff. Event windows: T+5, T+21, T+63, T+126, T+252 trading days after the event date

Each spinoff generates two events: one for the parent, one for the child. Abnormal return = stock return minus SPY return over the same calendar period. Returns are winsorized at the 1%/99% level to limit distortion from extreme outliers.

One deduplication note: Raytheon (RTX) spun off both Otis and Carrier on the same date (2020-04-03). RTX appears once as parent to avoid double-counting identical price observations. Viatris (VTRS) was excluded because no price data exists for its first post-spinoff trading day.

This gives us 29 parent events and 28 child events (57 total) from 30 spinoffs.

Academic basis: Cusatis, Miles & Woolridge (1993); McConnell & Ovtchinnikov (2004)

The Academic Baseline

Cusatis, Miles, and Woolridge (1993) examined spinoffs from 1965 to 1988 and found that both parents and children significantly outperformed the market. Spinoff children returned roughly 25% more than the market over three years. Parents outperformed by about 18%.

McConnell and Ovtchinnikov (2004) extended this with later data and found the results held, with much of the child's outperformance coming from eventual acquisitions at a premium.

Joel Greenblatt popularized the strategy in "You Can Be a Stock Market Genius" (1997), calling spinoffs one of the few places where individual investors have a structural edge over institutions.

Our dataset covers 2011-2024. Here's what the more recent data shows.

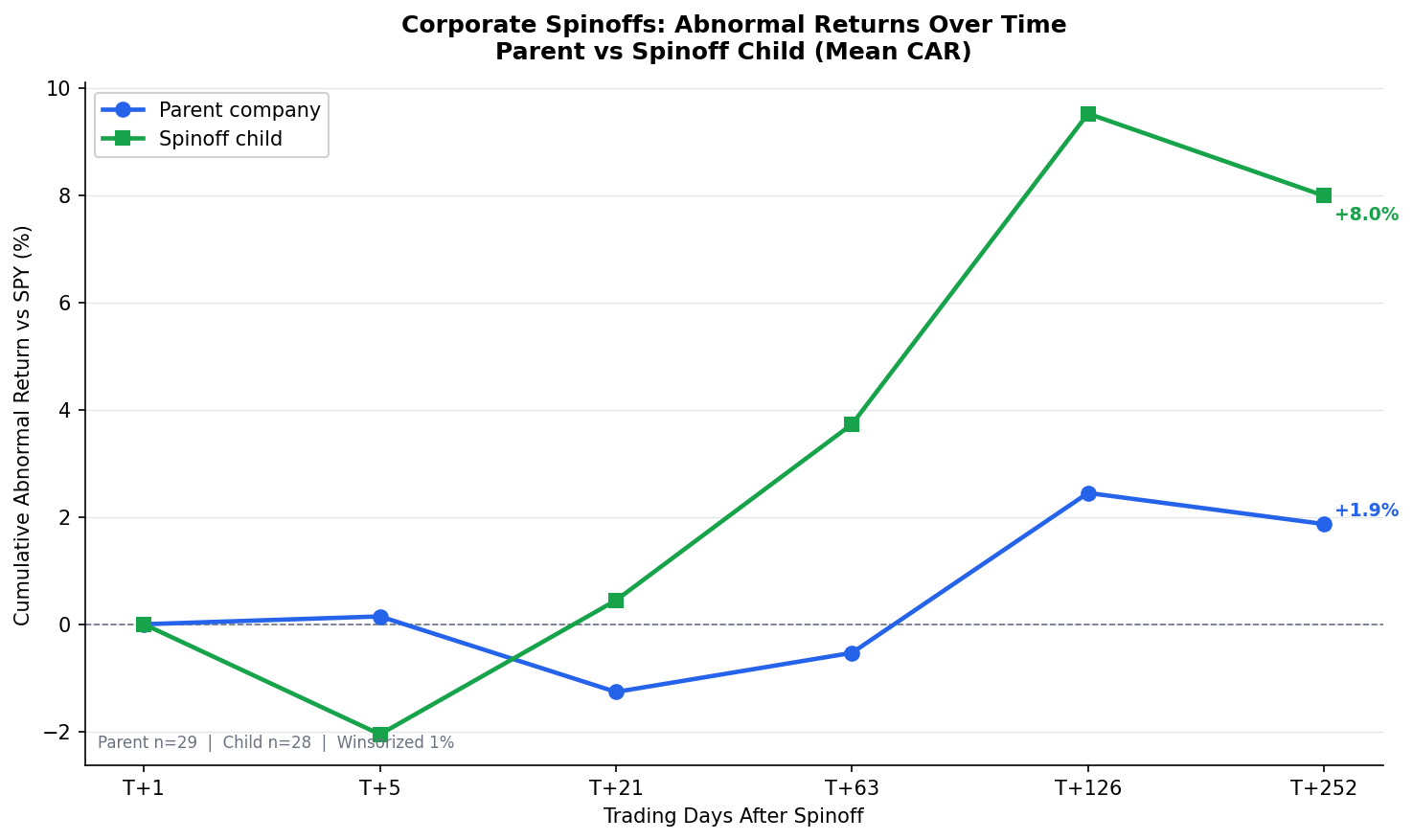

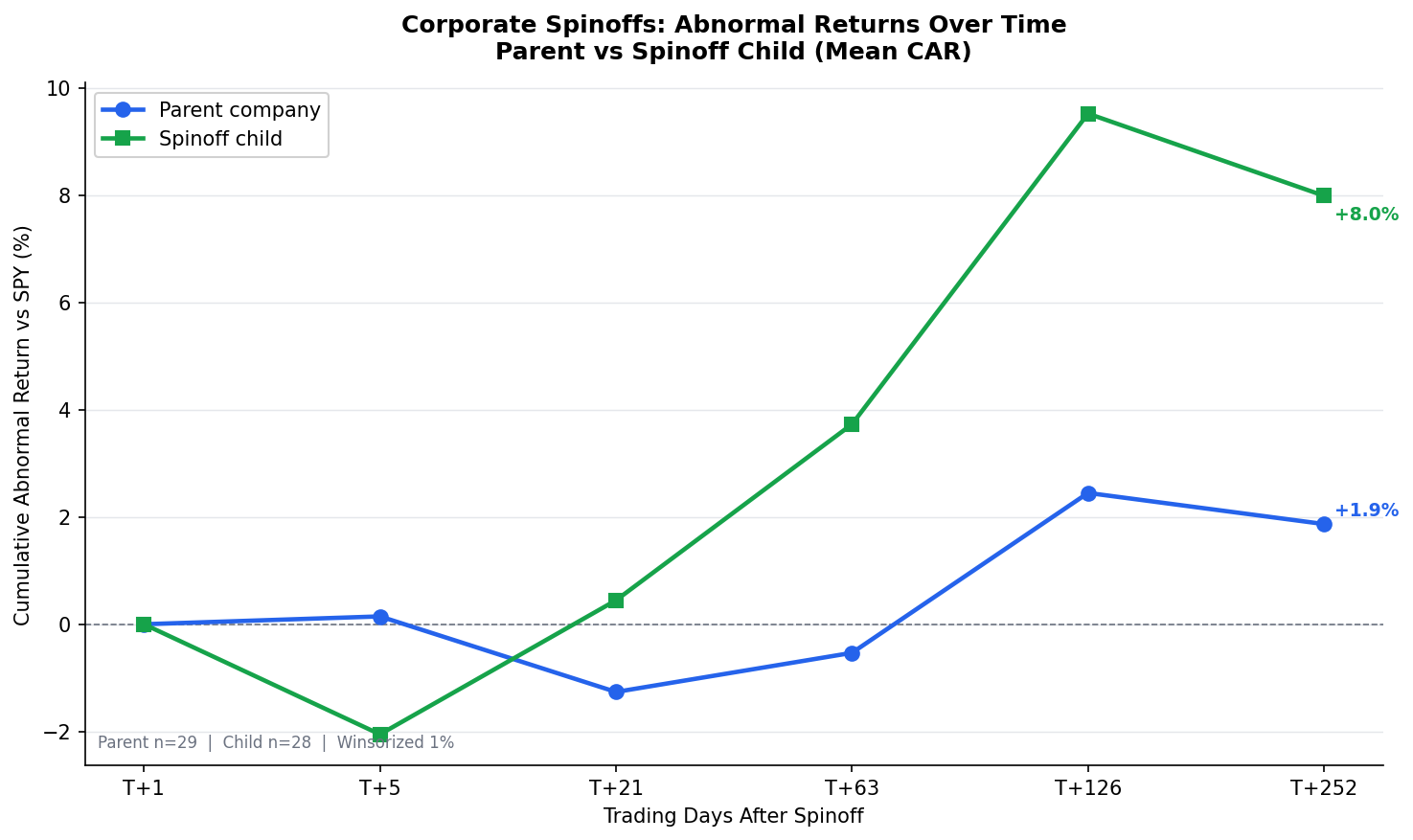

Results: Spinoff Children

| Window | Mean CAR | Median CAR | t-stat | N | Hit Rate |

|---|---|---|---|---|---|

| T+5 | -2.1% | -1.7% | -1.95 | 28 | 39.3% |

| T+21 | +0.5% | +0.4% | +0.24 | 28 | 57.1% |

| T+63 | +3.7% | +1.8% | +1.10 | 28 | 53.6% |

| T+126 | +9.5% | +7.3% | +1.59 | 28 | 53.6% |

| T+252 | +8.0% | +0.2% | +0.88 | 28 | 50.0% |

With next-day close entry (MOC execution), the first-week underperformance narrows to -2.1% (t = -1.95). That's close to the 5% significance threshold but doesn't clear it. Most of the forced selling hits on day zero, the event date itself, before a real investor could act.

After the first week, the recovery is steady. By T+63, children show +3.7% mean excess return. By T+126, it's +9.5%. At T+252, the mean reaches +8.0%.

The median at T+252 is +0.2%, just barely positive. Half of spinoff children outperformed SPY after one year. The distribution is right-skewed: a few large winners (Carrier +124%, GE Vernova +112%) pull the mean well above the median, but the typical spinoff child roughly matches the market.

Hit rate at T+252: 50.0%. A coin flip, consistent with a right-skewed distribution where the expected return comes from the tail.

Results: Spinoff Parents

| Window | Mean CAR | Median CAR | t-stat | N | Hit Rate |

|---|---|---|---|---|---|

| T+5 | +0.2% | -0.0% | +0.29 | 29 | 48.3% |

| T+21 | -1.3% | -0.3% | -0.85 | 29 | 48.3% |

| T+63 | -0.5% | -1.8% | -0.23 | 29 | 44.8% |

| T+126 | +2.5% | -2.0% | +0.66 | 29 | 48.3% |

| T+252 | +1.9% | +0.9% | +0.33 | 29 | 51.7% |

Parents show a flatter trajectory. They don't suffer the forced-selling hit that children take, but the focus and re-rating benefits are modest. The first-week return is essentially flat (+0.2% at T+5), and the mean stays below +2% at every window through one year.

By T+252, the mean is +1.9% and the median is +0.9%. Both are positive, but neither is statistically significant. The parent distribution is less skewed than the child distribution: the typical parent roughly matches SPY.

Nothing is statistically significant for parents at any window.

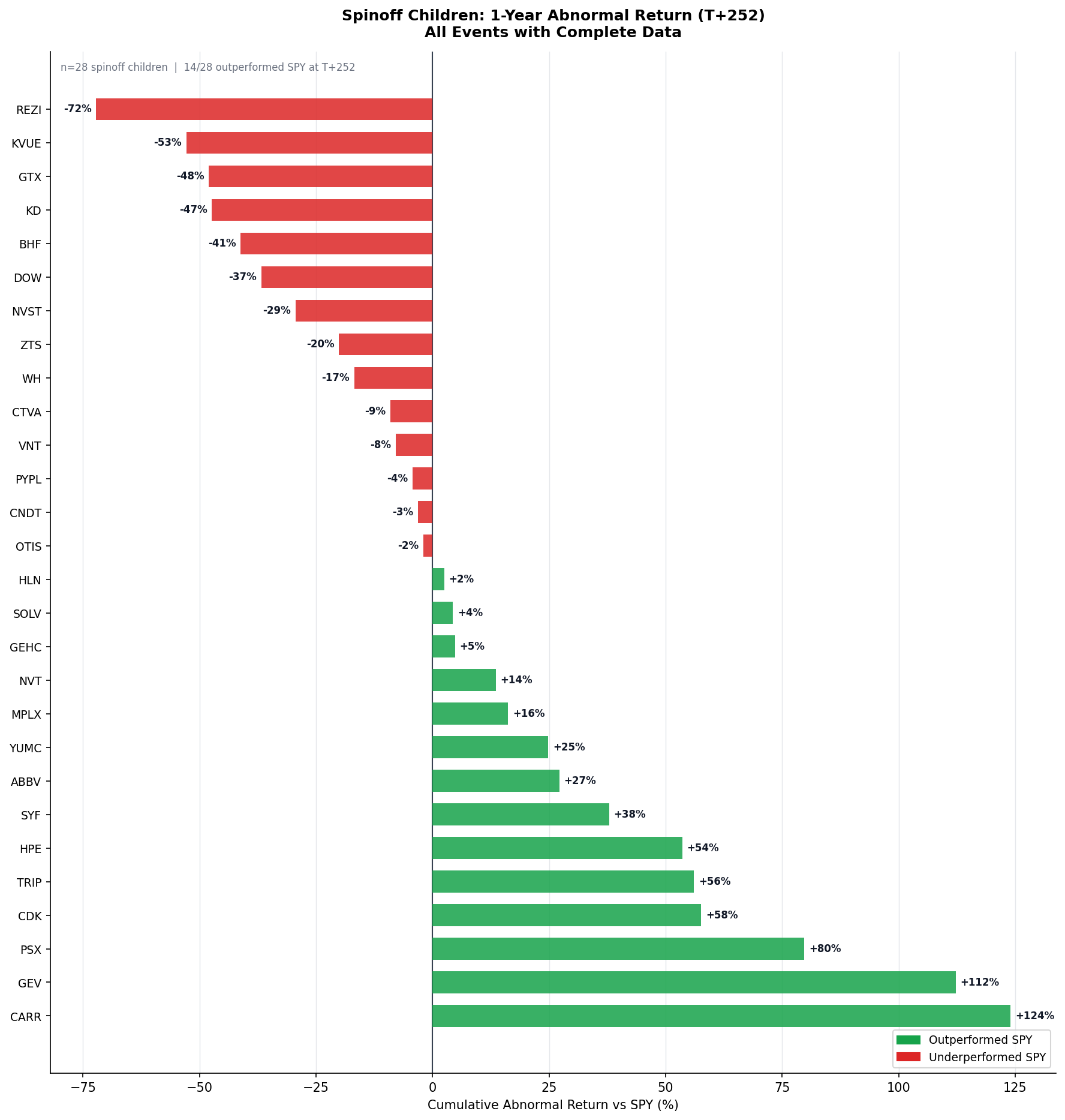

The Outlier Problem

The mean/median gap tells you everything about spinoff return distributions.

Best spinoff children (T+252):

| Child | Parent | Year | T+252 CAR |

|---|---|---|---|

| CARR (Carrier Global) | RTX | 2020 | +124.0% |

| GEV (GE Vernova) | GE | 2024 | +112.3% |

| PSX (Phillips 66) | COP | 2012 | +79.8% |

| CDK Global | ADP | 2014 | +57.6% |

| TRIP (TripAdvisor) | EXPE | 2011 | +56.1% |

Worst spinoff children (T+252):

| Child | Parent | Year | T+252 CAR |

|---|---|---|---|

| REZI (Resideo) | HON | 2018 | -72.2% |

| KVUE (Kenvue) | JNJ | 2023 | -52.8% |

| GTX (Garrett Motion) | HON | 2018 | -48.0% |

| KD (Kyndryl) | IBM | 2021 | -47.4% |

| BHF (Brighthouse Financial) | MET | 2017 | -41.2% |

The range is +124% to -72%. The best performers (Carrier, GE Vernova, Phillips 66) were spun off into sectors with strong fundamental tailwinds. Carrier caught the post-COVID construction cycle. GEV caught the energy transition. PSX benefited from the US shale boom.

The worst performers had structural headwinds. Resideo competed in commoditized home security hardware. Kenvue was carved out of J&J's consumer division right before generic competition intensified in its key categories. Kyndryl inherited IBM's legacy IT services business.

Forced selling was present in both groups. Fundamentals determined the outcome.

What This Means for Spinoff Investing

The forced-selling effect is real: children underperform by -2.1% in the first week after entry, with 61% underperforming SPY. That's close to statistical significance (t = -1.95, p = 0.06) but doesn't clear the 5% bar. Most of the selling pressure lands on the event date itself, before a real investor could act.

The long-term picture from a tradeable perspective is more promising than it first appears:

- The mean is positive and the median is barely positive. At T+252, children show +8.0% mean excess return with a +0.2% median. Half of spinoff children beat SPY over one year. The distribution is right-skewed, with a few large winners driving the mean, but the typical spinoff roughly matches the market rather than trailing it.

- The spread is enormous. CARR returned +124% vs SPY while REZI returned -72% vs SPY. A 196-point spread between best and worst over one year means stock selection matters more than event selection.

- The signal has compressed since the academic era. The academic evidence (1965-1988) found 25%+ excess returns over 3 years. Our 2011-2024 data shows +8.0% over 1 year with MOC entry. Either the strategy has been partially arbitraged, the time period matters, or the longer horizon captures effects we're not measuring.

- Sample size limits confidence. 28 child events is enough to see patterns, but t-statistics on this sample should be treated as directional, not definitive.

The Screen Today

Run this query on Ceta Research →

Recent spinoffs and their current cumulative abnormal return vs SPY (as of April 2026):

| Symbol | Type | Spinoff | Stock Ret | SPY Ret | CAR |

|---|---|---|---|---|---|

| GEV | child | Apr 2024 | +543.4% | +28.7% | +514.6% |

| GE | parent | Apr 2024 | +108.3% | +28.7% | +79.6% |

| SOLV | child | Apr 2024 | -8.0% | +27.9% | -35.9% |

| MMM | parent | Apr 2024 | +59.3% | +27.9% | +31.4% |

| JNJ | parent | May 2023 | +63.0% | +67.3% | -4.2% |

| GE | parent | Jan 2023 | +409.3% | +77.3% | +332.0% |

| IBM | parent | Nov 2021 | +143.7% | +48.6% | +95.1% |

| GSK | parent | Jul 2022 | +61.6% | +79.6% | -18.0% |

| HLN | child | Jul 2022 | +39.1% | +79.6% | -40.6% |

| GEHC | child | Jan 2023 | +16.8% | +77.3% | -60.4% |

| KVUE | child | May 2023 | -29.6% | +67.3% | -96.9% |

| KD | child | Nov 2021 | -49.8% | +48.6% | -98.4% |

GE appears twice: 2023 GEHC spinoff and 2024 GEV spinoff.

-- Current screen: recent spinoffs vs SPY (run on Ceta Research)

WITH spinoffs AS (

SELECT 'GEV' AS symbol, DATE '2024-04-02' AS spinoff_date, 'child' AS category, 'GE / GE Vernova' AS description UNION ALL

SELECT 'SOLV', DATE '2024-04-01', 'child', '3M / Solventum' UNION ALL

SELECT 'KVUE', DATE '2023-05-04', 'child', 'J&J / Kenvue' UNION ALL

SELECT 'GEHC', DATE '2023-01-04', 'child', 'GE / GE Healthcare' UNION ALL

SELECT 'HLN', DATE '2022-07-18', 'child', 'GSK / Haleon' UNION ALL

SELECT 'KD', DATE '2021-11-04', 'child', 'IBM / Kyndryl' UNION ALL

SELECT 'GE', DATE '2024-04-02', 'parent', 'GE / GE Vernova 2024' UNION ALL

SELECT 'MMM', DATE '2024-04-01', 'parent', '3M / Solventum' UNION ALL

SELECT 'JNJ', DATE '2023-05-04', 'parent', 'J&J / Kenvue' UNION ALL

SELECT 'GE', DATE '2023-01-04', 'parent', 'GE / GE Healthcare 2023' UNION ALL

SELECT 'GSK', DATE '2022-07-18', 'parent', 'GSK / Haleon' UNION ALL

SELECT 'IBM', DATE '2021-11-04', 'parent', 'IBM / Kyndryl'

),

latest_date AS (SELECT MAX(CAST(date AS DATE)) AS dt FROM stock_eod WHERE symbol = 'SPY'),

t0_dates AS (

SELECT s.symbol, s.spinoff_date, s.category, s.description,

MIN(CAST(e.date AS DATE)) AS t0_date

FROM spinoffs s

JOIN stock_eod e ON e.symbol = s.symbol AND CAST(e.date AS DATE) >= s.spinoff_date

GROUP BY s.symbol, s.spinoff_date, s.category, s.description

),

spy_t0_dates AS (

SELECT s.symbol, s.spinoff_date, MIN(CAST(e.date AS DATE)) AS t0_date

FROM spinoffs s

JOIN stock_eod e ON e.symbol = 'SPY' AND CAST(e.date AS DATE) >= s.spinoff_date

GROUP BY s.symbol, s.spinoff_date

)

SELECT t.category, t.symbol, t.description, t.spinoff_date,

ROUND((e_now.adjClose - e_t0.adjClose) / e_t0.adjClose * 100, 1) AS stock_ret_pct,

ROUND((spy_now.adjClose - spy_t0.adjClose) / spy_t0.adjClose * 100, 1) AS spy_ret_pct,

ROUND(((e_now.adjClose - e_t0.adjClose) / e_t0.adjClose - (spy_now.adjClose - spy_t0.adjClose) / spy_t0.adjClose) * 100, 1) AS car_pct

FROM t0_dates t

JOIN spy_t0_dates st ON st.symbol = t.symbol AND st.spinoff_date = t.spinoff_date

JOIN latest_date l ON TRUE

JOIN stock_eod e_t0 ON e_t0.symbol = t.symbol AND CAST(e_t0.date AS DATE) = t.t0_date

JOIN stock_eod e_now ON e_now.symbol = t.symbol AND CAST(e_now.date AS DATE) = l.dt

JOIN stock_eod spy_t0 ON spy_t0.symbol = 'SPY' AND CAST(spy_t0.date AS DATE) = st.t0_date

JOIN stock_eod spy_now ON spy_now.symbol = 'SPY' AND CAST(spy_now.date AS DATE) = l.dt

ORDER BY t.spinoff_date DESC, t.category, car_pct DESC

Data availability check for all spinoff children →

Limitations

Small sample. 28-29 events per group produces t-statistics in the 0.2-2.0 range. No result clears the 5% significance bar under MOC entry. Academic studies used hundreds of events over decades.

Selection bias. The curated list overrepresents large, well-known spinoffs. Smaller spinoffs may behave differently. We can't claim these results apply to all spinoffs.

Survivorship. All spinoffs in the list produced companies that traded for at least a year. Spinoffs that immediately failed or were absorbed aren't represented.

SPY benchmark. SPY doesn't control for sector, size, or style. A technology spinoff during a tech rally might show positive abnormal returns that are really just factor exposure.

Bull market period. 2011-2024 was mostly a strong bull market. Spinoff behavior during prolonged bear markets or flat markets may differ.

No transaction costs. The screen measures gross returns. Spinoff children often have wide spreads early in their trading life.

Takeaway

Corporate spinoffs produce a measurable forced-selling effect. Children trail SPY by -2.1% in their first trading week after next-day entry (t = -1.95, borderline significant). Most of the day-zero selling pressure is absorbed before a real investor can act.

The long-run picture, measured from realistic entry prices, is more promising than event-date analysis suggests. Children show +8.0% mean excess return at T+252, with a median of +0.2%. Half of spinoff children beat SPY over one year. Parents are flatter at +1.9% mean.

The academic case for spinoffs is built on decades of data and hundreds of events. Our 14-year, 30-spinoff sample shows the direction of long-term returns is positive. The magnitude has compressed since 1993, but from a tradeable perspective the average excess return remains meaningful.

For investors who can identify spinoffs with strong standalone fundamentals, the first few weeks after the spinoff may offer a reasonable entry point as forced selling clears. For investors looking to mechanically buy all spinoffs, the expected return is positive but comes with wide dispersion (a 196-point spread between best and worst) and a coin-flip hit rate.

Data: Ceta Research (FMP financial data warehouse). Curated spinoff list from SEC filings and public records (30 events, 2011-2024). Returns from next-day close (MOC execution). Abnormal returns computed vs SPY. Winsorized at 1%/99%. N=29 parents, N=28 children. Small sample limits statistical confidence. Past performance does not guarantee future results. This is educational content, not investment advice.

References

- Cusatis, P., Miles, J., & Woolridge, J. (1993). "Restructuring Through Spinoffs: The Stock Market Evidence." Journal of Financial Economics, 33(3), 293-311.

- McConnell, J. & Ovtchinnikov, A. (2004). "Predictability of Long-Term Spinoff Returns." Journal of Investment Management, 2(3).

- Greenblatt, J. (1997). You Can Be a Stock Market Genius. Simon & Schuster.