Defensive Quality UK: 12.63% CAGR and the Best Sharpe Ratio in a

Defensive Quality in the UK: Best Sharpe Ratio in a 16-Exchange Study

The UK result stands out on a single metric: Sharpe ratio of 0.666. That's the best risk-adjusted performance across 16 exchanges in our defensive quality study, including the US (0.608) and India (0.416).

Contents

- Method

- Why the UK Universe Is Thin

- What We Found

- Best Sharpe ratio globally

- Protection in crisis years

- Consistent compounding, no cash periods

- The Data

- Annual returns (2000–2024)

- Limitations

- Takeaway

- SQL Screen

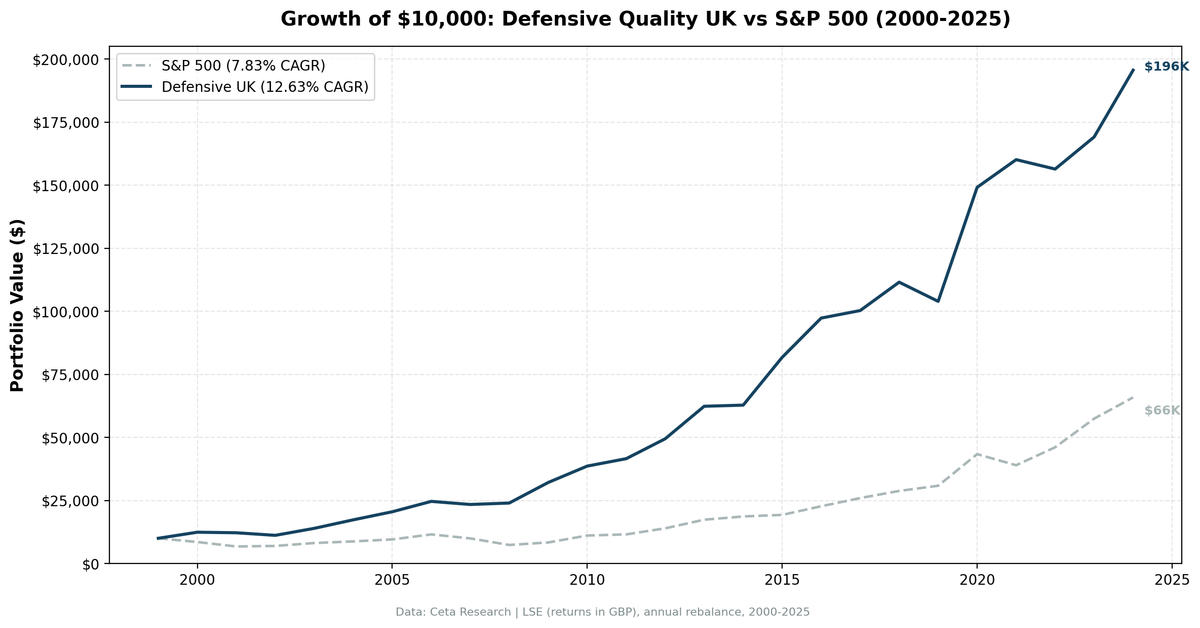

We ran the same quality screen on LSE stocks from 2000 to 2024. The portfolio returned 12.63% annually vs 7.83% for the S&P 500. Max drawdown was -9.99%. A portfolio with a Sharpe of 0.666 and a drawdown under 10% is producing exceptional risk-adjusted returns over 25 years.

One important caveat upfront: the LSE universe is thin. The portfolio averaged 13.6 stocks per period. That's borderline, and it means performance is more concentrated than a larger-universe strategy would be. We recommend the UK blog with this caveat stated clearly, not hidden.

Method

- Data source: Ceta Research (FMP financial data warehouse)

- Universe: LSE, market cap > £500M

- Period: 2000–2024 (25 annual periods, all invested, 0% cash)

- Rebalancing: Annual (July), equal weight top 30 by dividend yield (universe produced 10–20 qualifying stocks, not 30)

- Benchmark: S&P 500 Total Return (SPY, global reference)

- Cash rule: Hold cash if fewer than 10 qualifying stocks

Quality filters:

| Criterion | Threshold |

|---|---|

| Sectors | Consumer Defensive, Utilities, Healthcare |

| Return on Equity | > 6% |

| Operating Margin | > 8% |

| Debt/Equity | < 2.5 |

| Dividend Yield | > 0.5% |

| Ranking | Dividend yield, descending |

Transaction costs: size-tiered (0.1%/0.3%/0.5%), one-way. Returns in GBP. Full methodology: backtests/METHODOLOGY.md

Why the UK Universe Is Thin

The LSE has fewer companies in Consumer Defensive and Utilities relative to US or Indian exchanges. The UK consumer defensive space includes companies like Unilever, Reckitt Benckiser, and Imperial Brands. Utilities is dominated by a small set of regulated network businesses. Healthcare includes names like AstraZeneca, GSK, and Smith & Nephew.

These are high-quality, large-cap businesses. They pass the quality screen reliably. But there aren't many of them. After applying the market cap filter (> £500M), the sector constraint, and the quality/yield filters, the average period produces 13.6 qualifying stocks.

This matters for portfolio construction: the strategy is less diversified than US (22.8 stocks) or India (28.1 stocks). Single-stock volatility has more weight. The strong Sharpe ratio reflects the quality of the specific names in the screen rather than broad sector diversification.

What We Found

Best Sharpe ratio globally

| Metric | Portfolio | S&P 500 |

|---|---|---|

| CAGR (2000–2024) | 12.63% | 7.83% |

| Excess CAGR | +4.80% | — |

| Max drawdown | -9.99% | -36.27% |

| Annualized volatility | 13.7% | 16.2% |

| Sharpe ratio | 0.666 | 0.360 |

| Sortino ratio | 2.31 | 0.654 |

| Calmar ratio | 1.264 | 0.216 |

| Beta | 0.416 | 1.0 |

| Alpha | 7.33% | — |

| Down capture | -31.7% | 100% |

| Up capture | 98.7% | 100% |

| Win rate vs SPY | 64% | — |

The Sortino ratio of 2.31 means downside risk (returns below zero) is well-compensated. The -31.7% down capture, like the US (-9.5%), shows the portfolio gaining in market downturns.

Up capture of 98.7% shows the portfolio nearly matches SPY in growth years. That's different from the US portfolio's 81.6% up capture, the UK names, largely large-cap multinationals, don't lag as much in growth markets.

Protection in crisis years

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2000 | +24.1% | -14.8% | +38.9% |

| 2001 | -1.7% | -20.8% | +19.1% |

| 2007 | -5.0% | -13.7% | +8.7% |

| 2008 | +2.5% | -26.1% | +28.6% |

| 2021 | +7.4% | -10.2% | +17.6% |

2008 is the most striking: the portfolio gained 2.5% while SPY fell 26.1%. UK defensive stocks, consumer staples multinationals and regulated utilities, held their value through the global financial crisis.

2000–2001 shows similar protection during the dot-com correction. The UK portfolio's losses in 2001 were minimal (-1.7%) even as global equity markets entered a multi-year bear phase.

Consistent compounding, no cash periods

Zero cash periods across 25 years. The UK defensive universe always had 10+ qualifying stocks, even in early years when data coverage was thinner. The consistency of invested performance is a strength, the strategy never sat idle.

The Data

Annual returns (2000–2024)

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2000 | +24.1% | -14.8% | +38.9% |

| 2001 | -1.7% | -20.8% | +19.1% |

| 2002 | -8.4% | +3.3% | -11.7% |

| 2003 | +24.9% | +16.4% | +8.5% |

| 2004 | +24.2% | +7.9% | +16.3% |

| 2005 | +18.5% | +8.9% | +9.6% |

| 2006 | +20.1% | +20.9% | -0.8% |

| 2007 | -5.0% | -13.7% | +8.7% |

| 2008 | +2.5% | -26.1% | +28.6% |

| 2009 | +34.0% | +13.4% | +20.6% |

| 2010 | +20.2% | +32.9% | -12.7% |

| 2011 | +7.6% | +4.1% | +3.5% |

| 2012 | +19.0% | +20.9% | -1.9% |

| 2013 | +26.1% | +24.5% | +1.6% |

| 2014 | +0.7% | +7.4% | -6.7% |

| 2015 | +30.2% | +3.4% | +26.8% |

| 2016 | +19.0% | +17.7% | +1.3% |

| 2017 | +3.1% | +14.3% | -11.2% |

| 2018 | +11.2% | +10.9% | +0.3% |

| 2019 | -6.8% | +7.1% | -13.9% |

| 2020 | +43.5% | +40.7% | +2.8% |

| 2021 | +7.4% | -10.2% | +17.6% |

| 2022 | -2.3% | +18.3% | -20.6% |

| 2023 | +8.1% | +24.6% | -16.5% |

| 2024 | +15.7% | +14.7% | +1.0% |

Limitations

Thin universe. 13.6 stocks on average means this portfolio is concentrated. Individual company events can move performance. Compare to US (22.8 stocks) or India (28.1 stocks) for context.

GBP returns. Returns are denominated in GBP. A USD-based investor would experience USD/GBP currency effects. The pound has weakened against the dollar over parts of this period, which would reduce USD-adjusted returns.

Sector snapshot. Sector classifications come from the current FMP profile table. Companies that changed sectors or were acquired would have been classified under their current (or most recent) sector. For long-standing defensive names like Unilever or AstraZeneca, this is a non-issue.

2022 underperformance. The portfolio fell -2.3% while SPY gained 18.3%, a -20.6% excess. That year saw UK-specific market disruption (mini-budget, currency crisis). Strategies with LSE exposure faced volatility that wouldn't show up in a US-only portfolio. This is a real risk factor.

Takeaway

The UK delivers the best Sharpe ratio in the study. The combination of a small number of high-quality defensive names, consistent dividend yields, and low-beta sector exposure produced 12.63% CAGR with a -9.99% max drawdown over 25 years.

The thin universe is the honest caveat. With 13.6 stocks, this is concentrated exposure to a handful of UK defensive stalwarts. That concentration is why the Sharpe is high, these are genuinely quality businesses, but it also means single-name risk is elevated compared to a US or India portfolio.

Run the current UK screen: cetaresearch.com/data-explorer Full backtest code: github.com/ceta-research/backtests

SQL Screen

SELECT

k.symbol,

p.companyName,

p.exchange,

p.sector,

ROUND(k.returnOnEquityTTM * 100, 2) AS roe_pct,

ROUND(f.operatingProfitMarginTTM * 100, 2) AS opm_pct,

ROUND(f.debtToEquityRatioTTM, 2) AS de_ratio,

ROUND(f.dividendYieldTTM * 100, 2) AS div_yield_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM key_metrics_ttm k

JOIN financial_ratios_ttm f ON k.symbol = f.symbol

JOIN profile p ON k.symbol = p.symbol

WHERE p.sector IN ('Consumer Defensive', 'Utilities', 'Healthcare')

AND k.returnOnEquityTTM > 0.06

AND f.operatingProfitMarginTTM > 0.08

AND (f.debtToEquityRatioTTM IS NULL OR f.debtToEquityRatioTTM < 2.5)

AND f.dividendYieldTTM > 0.005

AND k.marketCap > 500000000

AND p.isActivelyTrading = true

AND p.exchange IN ('LSE')

ORDER BY f.dividendYieldTTM DESC

LIMIT 30

Part of a Series: Global | US | India

Data: Ceta Research (FMP financial data warehouse). Past performance doesn't guarantee future results. Returns in GBP.