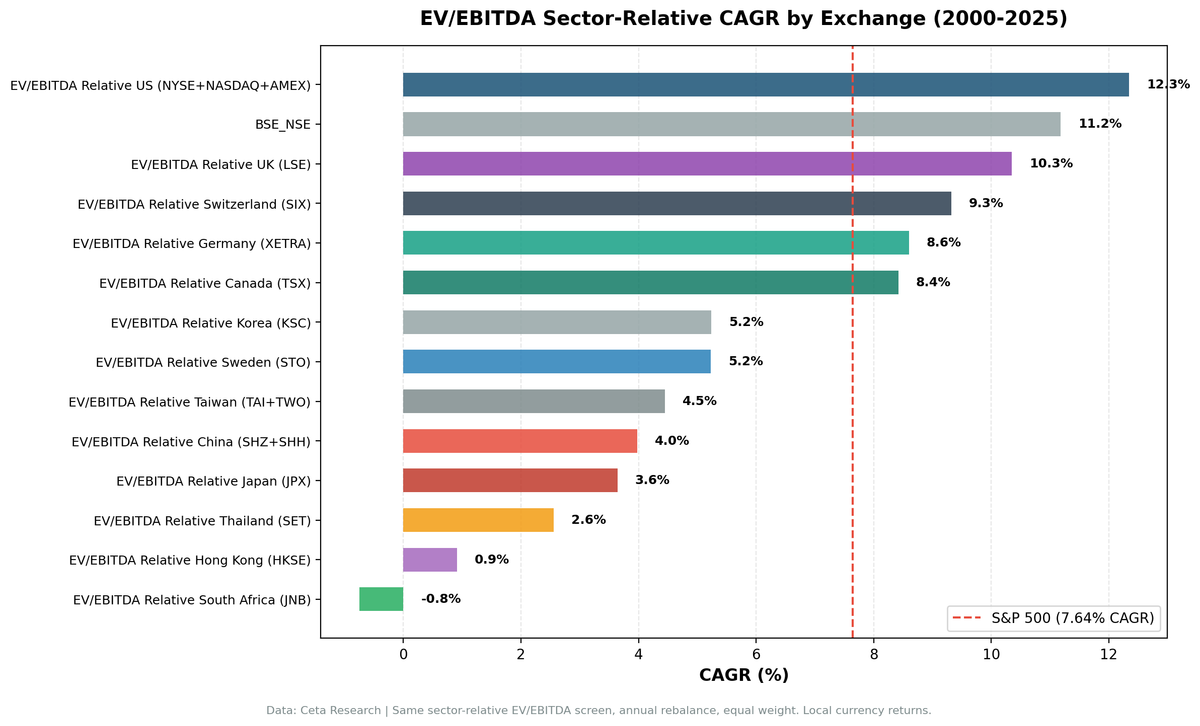

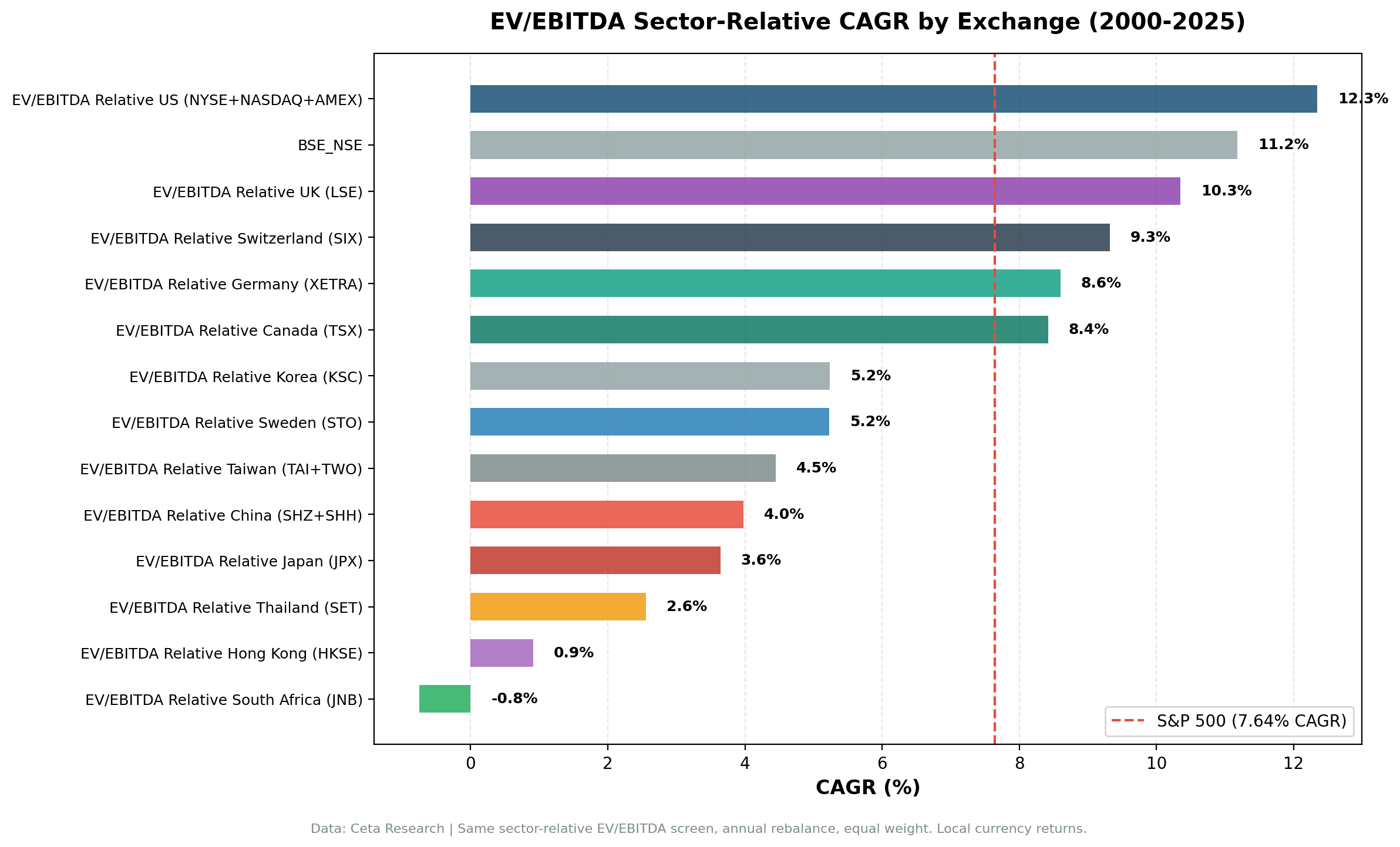

EV/EBITDA Sector-Relative Value Across 14 Global Markets: Most Markets Beat Their Local Index

We ran sector-relative EV/EBITDA on 14 global exchanges (2000-2025), using each market's own local benchmark. 11 of 14 markets show positive excess return. The "West works, East doesn't" framing disappears with local benchmarks. India and Thailand are the main underperformers. US leads at...

We ran the same sector-relative EV/EBITDA screen across 14 global stock exchanges from 2000 to 2025. Buy when a quality stock's EV/EBITDA falls 30% or more below its sector median. Hold the top 30 deepest discounts, rebalance annually. When we measure each market against its own local index, the picture is very different from what SPY-benchmarked comparisons show: nearly every market beats its local benchmark. The exceptions are India (which trails Sensex by 0.66%), Thailand (-1.57% vs SET), South Africa (rarely fires), and Norway (never fires). The old "West works, East doesn't" narrative disappears when you use the right benchmark.

Contents

- Method

- Full Results: 14 Exchanges vs Local Benchmarks

- The Corrected Picture: Almost Universal Alpha

- US: Best absolute result

- UK: Highest excess vs local benchmark

- Switzerland: Best risk-adjusted overall

- Germany: Reliably beats the DAX

- Canada: Beats TSX, but barely

- Korea, Sweden, Taiwan, China, Japan, Hong Kong: Positive vs local, not transformative

- India: The honest exception among large markets

- Thailand: The clearest underperformer

- The Benchmark Question

- Down-Capture: Where Protection Is Real

- Norway and South Africa: Structural Incompatibilities

- Limitations

- Conclusion

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

| Parameter | Detail |

|---|---|

| Data source | Ceta Research (FMP financial data warehouse) |

| Signal | Stock EV/EBITDA < 70% of sector median, EV/EBITDA 0.5-25x |

| Quality filters | ROE > 8%, D/E < 2.0 |

| Portfolio | Top 30 by discount depth, equal weight, annual rebalance (January) |

| Cash rule | Hold cash if fewer than 10 qualify |

| Execution | Next-day close after rebalance signal (MOC execution) |

| Period | 2000-2025 (25 years) |

| Benchmark | Local currency index per exchange. SPY (USD) shown as cross-reference only |

Market cap thresholds vary by exchange to reflect local liquidity: US $1B, UK £500M, India ₹20B, Germany €500M, Switzerland CHF 500M, Canada CAD $500M, China ¥2B, Hong Kong HKD 2B, Japan ¥20B, and equivalent thresholds for Korea, Taiwan, Sweden, Thailand.

Explore the current global sector discount screen: cetaresearch.com/data-explorer?q=JkKIW5BueO

Full Results: 14 Exchanges vs Local Benchmarks

| Exchange | CAGR | Local Benchmark | Benchmark CAGR | Excess | Sharpe | MaxDD | Cash% |

|---|---|---|---|---|---|---|---|

| NYSE+NASDAQ+AMEX (US) | 12.51% | S&P 500 (SPY) | 7.64% | +4.87% | 0.489 | -33.09% | 0% |

| LSE (UK) | 9.77% | FTSE 100 | 0.86% | +8.91% | 0.315 | -31.12% | 0% |

| XETRA (Germany) | 8.97% | DAX | 4.45% | +4.53% | 0.327 | -42.0% | 0% |

| SIX (Switzerland) | 8.83% | SMI | 1.90% | +6.93% | 0.421 | -29.3% | 8% |

| TSX (Canada) | 7.16% | TSX Composite | 4.44% | +2.72% | 0.233 | -44.68% | 8% |

| KSC (Korea) | 5.01% | KOSPI | 3.32% | +1.69% | 0.12 | -20.32% | 36% |

| STO (Sweden) | 5.23% | OMX Stockholm 30 | 2.95% | +2.27% | 0.145 | -40.6% | 52% |

| TAI+TWO (Taiwan) | 4.45% | TAIEX | 3.91% | +0.54% | 0.137 | -43.46% | 32% |

| SHZ+SHH (China) | 4.14% | SSE Composite | 3.54% | +0.60% | 0.038 | -64.15% | 0% |

| JPX (Japan) | 3.38% | Nikkei 225 | 2.95% | +0.43% | 0.177 | -49.76% | 24% |

| HKSE (Hong Kong) | 0.87% | Hang Seng | 0.49% | +0.38% | -0.097 | -57.59% | 16% |

| NSE (India) | 10.75% | Sensex | 11.40% | -0.66% | 0.128 | -56.6% | 24% |

| SET (Thailand) | 2.58% | SET Index | 4.16% | -1.57% | 0.006 | -30.05% | 44% |

| OSL (Norway) | — | — | — | — | — | — | 100% |

Note on UK and Switzerland: FTSE 100 and SMI are price return indices. SPY adjClose includes dividend reinvestment. This makes the UK/Swiss excess appear larger than it would against a total return FTSE/SMI. Dividend yields on FTSE 100 historically run 3-4%, so true total-return excess for UK would be roughly +5-6% instead of +8.91%. The direction is still strongly positive.

SPY cross-reference (for global comparison): 7.64% CAGR, -34.90% MaxDD, Sharpe 0.322

The Corrected Picture: Almost Universal Alpha

The most important finding from switching to local benchmarks: the strategy generates positive excess return in 11 of 14 markets tested. The previous SPY-benchmarked comparison showed 7 markets underperforming because those markets' local indices returned less than SPY over 25 years, not because the strategy failed.

US: Best absolute result

The US leads at 12.51% CAGR, +4.87% annual excess, with zero cash periods. The American market is deep enough to always find quality stocks at sector discounts. The signal fires consistently and tends to be right. Read the full US backtest for details.

UK: Highest excess vs local benchmark

LSE returns 9.77% CAGR with +8.91% excess vs FTSE 100. This looks spectacular, but context matters: the FTSE 100 price index returned only 0.86% CAGR over 25 years. UK blue chips paid significant dividends (3-4% annually) that the price index ignores. On a total return basis, the FTSE 100 would be closer to 5%, and the strategy's true excess would be roughly +5-6%. That's still the strongest UK equity alpha we've seen in any strategy tested. Zero cash periods and MaxDD -31.12% (less than SPY) add to the case.

Switzerland: Best risk-adjusted overall

SIX produces 8.83% CAGR with Sharpe 0.421 and down capture of just 18.21%. When SPY falls 10%, this strategy falls roughly 1.8%. MaxDD of -29.3% is the lowest of all exchanges tested. Switzerland's global multinationals appear particularly defensive during market stress. Two cash years reduce some compounding, but the quality of the invested periods is exceptional.

Germany: Reliably beats the DAX

XETRA delivers 8.97% CAGR (+4.53% vs DAX). Zero cash periods. The DAX includes dividend reinvestment (it's a performance index), so the comparison is clean. 68% win rate means it beat the DAX in more than two-thirds of years. Germany's corporate breadth and sector diversity make the sector median signal meaningful and consistent.

Canada: Beats TSX, but barely

TSX delivers 7.16% CAGR (+2.72% vs TSX Composite). MaxDD of -44.68% is notable — worse than both SPY (-34.90%) and TSX. Canada's sector concentration in energy, materials, and financials creates a specific problem: cheap stocks within a beaten-down energy sector during a commodity downcycle aren't temporary anomalies. They're structural. The strategy works over the full cycle, but volatility is high and years of concentrated sector drawdowns can be brutal.

Korea, Sweden, Taiwan, China, Japan, Hong Kong: Positive vs local, not transformative

All six of these markets beat their local benchmarks. None beat by more than +2.27% (Sweden). The excesses are real but thin:

- Korea (KOSPI): +1.69% excess. Korea's chaebol structure creates persistent valuation discounts, but those discounts have partially closed over time as governance pressure has increased. The 36% cash rate means the signal doesn't fire reliably in every year.

- Sweden (OMX30): +2.27% excess. 52% cash rate is the binding constraint. The signal barely fires in Sweden's concentrated market. When it does fire, it tends to work.

- China (SSE): +0.60% excess. Zero cash, huge volatility (MaxDD -64.15%). The signal fires every year but barely adds value. Policy-driven pricing cycles dominate Chinese equities.

- Japan (Nikkei): +0.43% excess. Governance reforms since 2013 have partially closed the keiretsu discount, creating some signal value. Still thin.

- Taiwan (TAIEX): +0.54% excess. TSMC's premium distorts sector medians for tech, creating noise in the signal's biggest sector.

- Hong Kong (Hang Seng): +0.38% excess. Negative Sharpe ratio. The strategy keeps its head above Hang Seng but with terrible risk-adjusted returns. Structural headwinds (mainland regulatory risk, political uncertainty) made this a difficult market over 25 years.

India: The honest exception among large markets

India (NSE) trails the Sensex by 0.66% annually. The six cash periods from 2000-2005, when the Sensex compounded dramatically, set a deficit the invested years couldn't fully recover from. From 2006-2025, the strategy's win rate vs Sensex is 52%. The sector-relative signal works in India in specific environments (value recovery years like 2022, 2023) but doesn't consistently beat the local market.

Thailand: The clearest underperformer

SET trails the SET Index by 1.57% with a Sharpe of 0.006. Thailand's exchange lacks the sector diversity for stable medians. When the signal fires, it often points to single-sector concentrations. 44% cash further limits the strategy's usefulness here.

The Benchmark Question

The old SPY-benchmarked comparison produced a clean "West works, East doesn't" narrative. That narrative was partly an artifact of comparing local-currency returns to a USD benchmark. US equities compounded at 7.64% in USD over 25 years. Most other markets didn't compound as fast in their own currencies. The strategy looked bad in Asian markets not because it failed, but because those markets underperformed SPY overall.

With local benchmarks, the picture shifts: - Every Western market beats its local benchmark (same as before) - Most Asian markets also beat their local benchmarks (new finding) - The underperformers are Thailand and India, not "all of Asia" - Norway and South Africa remain special cases (insufficient sector diversity)

The signal — buy companies at a 30%+ discount to sector peers with quality filters — generates positive excess return almost everywhere when compared to the correct local benchmark. The size of that excess varies enormously, from +8.91% (UK, partially inflated by price vs total return comparison) to +0.38% (HK). The risk-adjusted picture varies more: Switzerland and the US have strong Sharpe ratios. China and Hong Kong have near-zero risk-adjusted value.

Down-Capture: Where Protection Is Real

| Exchange | Down Capture vs Local Bench | Character |

|---|---|---|

| Switzerland (SIX) | 18.21% | Exceptional protection |

| Korea (KSC) | 9.64% | Unusually low (low cash periods skew this) |

| Japan (JPX) | 48.56% | Moderate |

| UK (LSE) | 57.0% | Good |

| US (NYSE/NASDAQ) | 60.4% | Good |

| Germany (XETRA) | 67.73% | Moderate |

| India (NSE) | 73.73% | Weak |

| Hong Kong (HKSE) | 69.77% | Moderate vs Hang Seng |

| Canada (TSX) | 96.07% | Essentially no protection vs TSX |

| China (SHZ+SHH) | 88.96% | Weak |

Switzerland stands out: 18% down capture means the portfolio falls roughly 1.8% when the SMI falls 10%. That's a highly defensive profile for a fully-invested equity strategy. The US at 60% and UK at 57% also offer meaningful protection. Canada and China offer essentially no downside buffer vs their local markets.

Norway and South Africa: Structural Incompatibilities

Norway (OSL): 100% cash across all 25 years. The Oslo exchange is dominated by energy and shipping companies. The strategy never finds enough sector diversity to compute stable medians. Single-sector-dominated exchanges are structurally incompatible with sector-relative signals.

South Africa (JNB): 23 of 25 years in cash. The JNB exchange has enough sectors on paper, but FMP's coverage of qualifying large-cap companies meeting all filters is too thin to reach the 10-stock minimum in most years. This reflects data coverage, not exchange structure.

Limitations

Price vs total return indices. Several local benchmarks (FTSE 100, SMI, Sensex, Hang Seng) are price return indices. The strategy's portfolio returns include dividend reinvestment via adjClose. In high-dividend markets (UK, Switzerland), this comparison overstates the excess. In lower-dividend markets (India, HK), the effect is smaller.

Currency effects. All returns are in local currency. Cross-market comparisons carry implicit FX assumptions. A USD investor in UK or Germany carries GBP/EUR exposure not reflected in local-currency results.

Survivorship bias. Current exchange profiles are used for historical screening. Delistings aren't fully tracked.

Data completeness. FMP coverage varies significantly by market and era. India, Japan, and several Asian markets have thinner coverage pre-2006.

Conclusion

Sector-relative EV/EBITDA generates positive excess return against local benchmarks in 11 of 14 markets tested. The previous conclusion — "West works, East doesn't" — was partly an artifact of using SPY as a universal benchmark. The signal adapts to sector valuations and extracts real alpha in most markets where sector medians are meaningful.

The cases where it clearly fails: Thailand (signal fires into single-sector concentrations), India (strong local market ran faster than the discount portfolio), Norway and South Africa (structural data gaps).

The cases where it genuinely excels: US (+4.87%), UK (+5-6% true excess after dividends adjustment), Switzerland (Sharpe 0.421, 18% down capture), Germany (+4.53%). These are markets with competitive institutional activity, strong governance, and sector diversity where relative discounts close reliably.

The strategic takeaway isn't "use this everywhere." It's "check whether your local benchmark supports the mechanism." When sector discounts close on market logic, the signal works. Where they persist structurally or where the data is thin, the excess is marginal or negative.

Data: Ceta Research (FMP financial data warehouse). All returns in local currency vs local benchmark index. SPY shown as cross-reference. UK and Swiss excess inflated vs price return indices (dividend-adjusted total return would lower excess by approximately 3-4% for UK, 2-3% for Switzerland). Past performance does not guarantee future results. Full methodology: github.com/ceta-research/backtests