EV/EBITDA Sector-Relative Value on Hong Kong: Structural Discounts

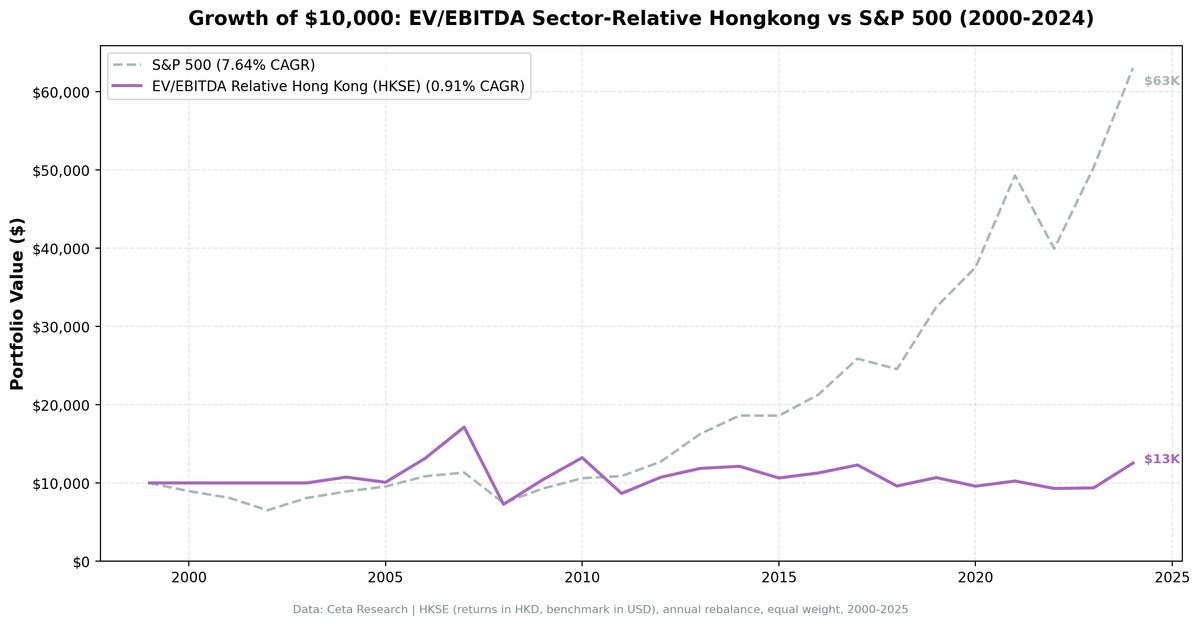

We ran a sector-relative EV/EBITDA screen on 21 years of Hong Kong stock data from HKSE. The result: 0.91% CAGR vs 7.64% SPY, a negative Sharpe ratio, and down-capture of 102.95%. When SPY falls 10%, Hong Kong loses 10.3%. This is the worst result of any exchange in this global backtest, and understanding why matters more than the number itself. Hong Kong's persistent discounts aren't anomalies waiting to be corrected. They're structural, driven by factors the signal can't distinguish from temporary mispricing.

Contents

- Method

- The Screen

- Sector-Relative EV/EBITDA Screen for HKSE (SQL)

- What We Found

- 21 invested years. Negative Sharpe. Down-capture over 100%.

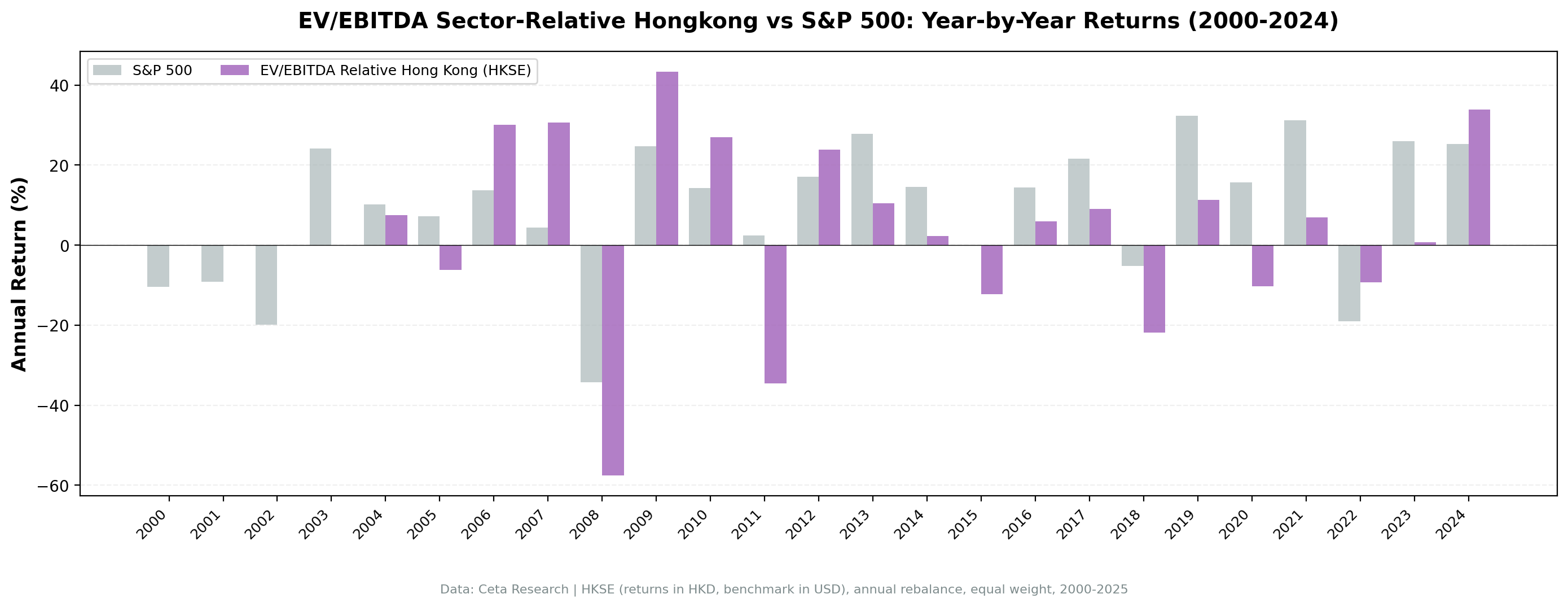

- Year-by-year returns

- 2008: -57.6% catastrophic loss

- The structural discount problem

- 2011: -34.5% from the European crisis

- 2019-2021: three consecutive damaging years

- 2024: +33.9%, the best year

- Backtest Methodology

- Limitations

- Conclusion

Method

| Parameter | Detail |

|---|---|

| Data source | Ceta Research (FMP financial data warehouse) |

| Universe | HKSE (Hong Kong Stock Exchange), MCap > HKD 2B |

| Signal | Stock EV/EBITDA < 70% of sector median (30%+ discount to peers) |

| EV/EBITDA range | 0.5-25x |

| Quality filters | ROE > 8%, D/E < 2.0 |

| Portfolio | Top 30 by deepest discount, equal weight |

| Rebalancing | Annual (January) |

| Cash rule | Hold cash if fewer than 10 stocks qualify |

| Period | 2000-2025 (25 years, 4 cash periods) |

| Benchmark | S&P 500 Total Return (SPY, USD) |

Financial data sourced from key_metrics_ttm for EV/EBITDA and market cap, financial_ratios_ttm for debt metrics, profile for sector classification. 45-day lag on all financial statements to prevent look-ahead bias.

The Screen

Sector-Relative EV/EBITDA Screen for HKSE (SQL)

WITH universe AS (

SELECT k.symbol, p.companyName, p.exchange, p.sector,

k.evToEBITDATTM AS ev_ebitda, k.returnOnEquityTTM AS roe,

fr.debtToEquityRatioTTM AS de, k.marketCap

FROM key_metrics_ttm k

JOIN financial_ratios_ttm fr ON k.symbol = fr.symbol

JOIN profile p ON k.symbol = p.symbol

WHERE k.evToEBITDATTM BETWEEN 0.5 AND 25

AND k.returnOnEquityTTM > 0.08

AND (fr.debtToEquityRatioTTM IS NULL OR (fr.debtToEquityRatioTTM >= 0 AND fr.debtToEquityRatioTTM < 2.0))

AND k.marketCap > 2000000000

AND p.sector IS NOT NULL

AND p.exchange IN ('HKSE')

),

sector_medians AS (

SELECT exchange, sector,

PERCENTILE_CONT(0.5) WITHIN GROUP (ORDER BY ev_ebitda) AS median_ev_ebitda,

COUNT(*) AS n_sector_stocks

FROM universe GROUP BY exchange, sector HAVING COUNT(*) >= 5

)

SELECT u.symbol, u.companyName, u.exchange, u.sector,

ROUND(u.ev_ebitda, 2) AS ev_ebitda_ttm,

ROUND(sm.median_ev_ebitda, 2) AS sector_median_ev_ebitda,

ROUND(u.ev_ebitda / sm.median_ev_ebitda, 3) AS ev_ratio_to_sector,

ROUND((1 - u.ev_ebitda / sm.median_ev_ebitda) * 100, 1) AS discount_pct,

ROUND(u.roe * 100, 1) AS roe_pct,

ROUND(u.de, 2) AS debt_to_equity,

ROUND(u.marketCap / 1e9, 2) AS mktcap_b

FROM universe u JOIN sector_medians sm ON u.exchange = sm.exchange AND u.sector = sm.sector

WHERE u.ev_ebitda / sm.median_ev_ebitda < 0.70

ORDER BY u.ev_ebitda / sm.median_ev_ebitda ASC LIMIT 30

Run this screen on Ceta Research

What We Found

21 invested years. Negative Sharpe. Down-capture over 100%.

| Metric | EV/EBITDA Sector-Relative (Hong Kong) | S&P 500 |

|---|---|---|

| CAGR | 0.91% | 7.64% |

| Total Return | ~24.5% (21 years) | 530.71% |

| Sharpe Ratio | -0.095 | 0.322 |

| Max Drawdown | -57.59% | -34.90% |

| Up Capture | N/A | 100% |

| Down Capture | 102.95% | 100% |

| Win Rate vs SPY | 36% | - |

| Avg Stocks per Year | 21.1 | - |

| Cash Periods | 4 of 25 (2000-2003) | - |

A negative Sharpe ratio means the strategy earned less than the risk-free rate per unit of risk over 21 invested years. In practical terms: you would have done better in cash than in this portfolio on a risk-adjusted basis.

The 4 cash periods at the start (2000-2003) happened to avoid the early bear market. When the strategy first invested in 2004, it walked into a reasonable setup. But from 2008 onward, the structural problems in HKSE-listed companies made the signal consistently unreliable.

Year-by-year returns

| Year | Strategy | S&P 500 | Excess |

|---|---|---|---|

| 2000 | 0% (cash) | -10.5% | - |

| 2001 | 0% (cash) | -9.2% | - |

| 2002 | 0% (cash) | -19.9% | - |

| 2003 | 0% (cash) | +24.1% | - |

| 2004 | +7.5% | +10.2% | -2.8% |

| 2005 | -6.2% | +7.2% | -13.3% |

| 2006 | +30.1% | +13.7% | +16.5% |

| 2007 | +30.6% | +4.4% | +26.2% |

| 2008 | -57.6% | -34.3% | -23.3% |

| 2009 | +43.4% | +24.7% | +18.6% |

| 2010 | +27.0% | +14.3% | +12.7% |

| 2011 | -34.5% | +2.5% | -37.0% |

| 2012 | +23.8% | +17.1% | +6.7% |

| 2013 | +10.5% | +27.8% | -17.3% |

| 2014 | +2.3% | +14.5% | -12.2% |

| 2015 | -12.3% | -0.1% | -12.2% |

| 2016 | +6.0% | +14.4% | -8.4% |

| 2017 | +9.0% | +21.6% | -12.6% |

| 2018 | -21.9% | -5.2% | -16.8% |

| 2019 | +11.3% | +32.3% | -21.0% |

| 2020 | -10.3% | +15.6% | -26.0% |

| 2021 | +6.9% | +31.3% | -24.3% |

| 2022 | -9.3% | -19.0% | +9.7% |

| 2023 | +0.8% | +26.0% | -25.2% |

| 2024 | +33.9% | +25.3% | +8.6% |

2008: -57.6% catastrophic loss

The global financial crisis hit HKSE-listed companies harder than most markets. Many Hong Kong-listed firms had significant mainland China exposure through real estate and banking. When Lehman collapsed and credit markets froze, those exposures became liabilities. The -57.6% single-year loss is catastrophic and impossible to recover from in any normal compounding timeline.

The structural discount problem

Several factors create persistent HKSE discounts that the signal reads as opportunity but which don't mean-revert:

Mainland Chinese listings. A large proportion of HKSE-listed companies are mainland Chinese businesses (H-shares and Red Chips). These trade at persistent discounts to their A-share or global peers for reasons that are structural: lower governance standards, related-party risk, state ownership constraints, and limited mechanisms for minority shareholder value realization.

Property developer leverage. Companies like Evergrande, Country Garden, and their peers traded at low EV/EBITDA multiples relative to sector medians for years before 2021. The signal would have included them as "cheap vs sector." The cheap multiples reflected genuine default risk, not temporary sentiment pessimism.

Political risk premium. Post-2019, Hong Kong's special administrative status became less certain. The 2019 protest movement, the 2020 National Security Law, and subsequent pressure on the independent financial market created a risk premium that rational investors applied to HKSE listings. That premium compresses multiples but doesn't revert because the underlying risk is real.

2011: -34.5% from the European crisis

The 2011 European debt crisis triggered capital flight from Hong Kong. HKSE-listed companies had significant cross-border exposure to European credit markets. The -34.5% return (vs SPY +2.5%, -37% excess) shows how quickly HK can amplify global risk events.

2019-2021: three consecutive damaging years

- 2019: +11.3% vs SPY +32.3%. The protest movement affected commercial real estate, retail, and financial services.

- 2020: -10.3% vs SPY +15.6%. COVID + National Security Law + regulatory uncertainty.

- 2021: +6.9% vs SPY +31.3%. Evergrande default contagion + China tech regulatory crackdown affected dozens of HKSE-listed names.

Each year brought a different macro event. The sector-relative signal couldn't anticipate or protect against any of them.

2024: +33.9%, the best year

Chinese government stimulus announcements drove HKSE sharply higher in 2024. The +8.6% excess return was the second-best year in the backtest. This is the pattern: occasional large positive years driven by policy announcements, surrounded by sustained underperformance. The signal can't predict when Beijing will announce stimulus.

Backtest Methodology

Full methodology: backtests/METHODOLOGY.md

| Parameter | Choice |

|---|---|

| Universe | HKSE, MCap > HKD 2B |

| Signal | EV/EBITDA < 70% of sector median, range 0.5-25x |

| Quality | ROE > 8%, D/E < 2.0 |

| Portfolio | Top 30 by deepest discount, equal weight |

| Rebalancing | Annual (January) |

| Cash rule | Hold cash if < 10 qualify |

| Benchmark | S&P 500 Total Return (SPY, USD) |

| Period | 2000-2025 (25 years) |

| Data | Point-in-time (45-day lag on FY financial statements) |

| Transaction costs | 0.1% one-way (size-tiered by market cap) |

Limitations

Negative Sharpe ratio. Over 21 invested years, the strategy produced risk-adjusted returns below the risk-free rate. This is the clearest possible signal that the strategy doesn't work in this market.

Structural discount persistence. The core assumption of sector-relative strategies, that discounts are temporary anomalies that mean-revert, is violated by HKSE's structural pricing dynamics.

MaxDD -57.59%. The second-worst max drawdown of 13 exchanges. Recovery from -57.6% requires a +134% return to break even.

Data completeness. FMP's HKSE data coverage improves post-2004. The 4 cash years at the start may partly reflect data availability rather than genuine signal failure. The invested track record starts from 2004.

Down-capture > 100%. The strategy amplifies rather than dampens SPY downturns. This is the opposite of what defensive positioning should achieve.

Conclusion

Sector-relative EV/EBITDA on HKSE produced 0.91% CAGR over 21 invested years: negative Sharpe ratio, -57.59% max drawdown, and 102.95% down-capture. This is the clearest failure in the 13-exchange study.

The failure isn't about the signal construction or the quality filters. It's about the nature of HKSE discounts. Property developer leverage, mainland listing risk premiums, political uncertainty, and governance concerns create discounts that look like value opportunities but are reflections of structural risk. The signal can't distinguish between "temporarily cheap" and "cheap for a reason that won't change."

We're publishing this result because reporting only the successes would be misleading. The discipline of running the same strategy across every market and publishing every outcome, including the clear failures, is what makes backtesting useful.

Part of a Series: Sweden | Global | US | UK | Switzerland | Japan | India | Germany

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP financial data warehouse). Returns in HKD (local currency). Benchmark S&P 500 in USD. Past performance doesn't guarantee future results. See full methodology at github.com/ceta-research/backtests.