Oversold Quality Germany: Best Risk-Adjusted Returns in the Series

Contents

- Portfolio Summary

- The Strategy

- The 35% Cash Rate: Feature or Bug?

- Annual Returns

- The Standout Years

- Why the Risk Profile is Different

- Screener: Current XETRA Quality Stocks

- Limitations

- Part of a Series

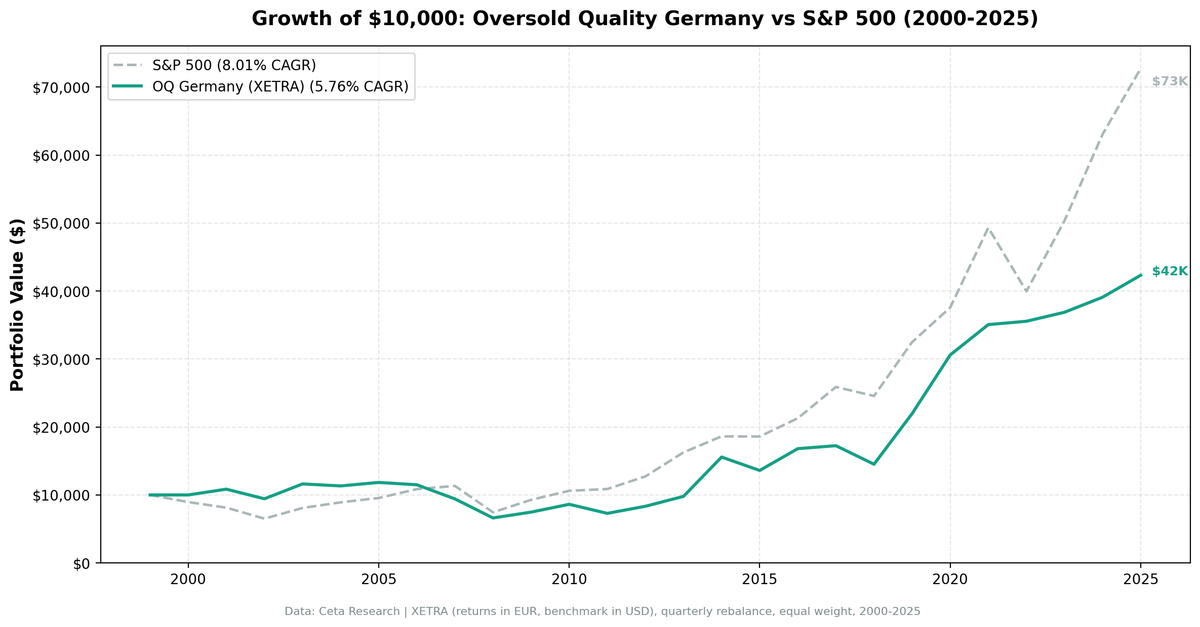

Germany produced the best risk-adjusted result of any exchange we tested. Sharpe ratio of 0.193, down-capture of 59.6%, volatility of 19.52%. On every metric that measures how well the portfolio managed risk, XETRA came out on top across all 16 exchanges in this series. The headline CAGR of 5.76% trails SPY's 8.01% over the same 25 years, but that gap looks different when you account for how the portfolio got there.

There's a caveat that belongs in the first paragraph, not buried at the end: in 36 of 103 quarters tested, this portfolio held cash. That's 35% of the time. If fewer than 5 XETRA stocks simultaneously had a Piotroski F-Score of 7 or higher and an RSI below 30, the portfolio didn't invest. It waited. That's a real cost, and we'll address it directly.

Portfolio Summary

| Metric | Value |

|---|---|

| Exchange | XETRA (Germany) |

| Period | Jan 2000 to Dec 2025 (25.8 years, 103 quarters) |

| CAGR | 5.76% |

| SPY CAGR | 8.01% |

| Excess CAGR | -2.25% |

| Total Return | 323.2% |

| SPY Total Return | 627.5% |

| Max Drawdown | -48.0% |

| Sharpe Ratio | 0.193 |

| Volatility | 19.52% |

| Up-Capture | 70.3% |

| Down-Capture | 59.6% |

| Win Rate vs SPY | 39.8% |

| Cash Periods | 36/103 (35%) |

| Avg Stocks When Invested | 13.8 |

The Strategy

Oversold Quality combines two independent filters. The first is the Piotroski F-Score, a nine-point accounting quality screen that evaluates profitability (positive ROA, positive operating cash flow, improving ROA, cash-based earnings), leverage (falling debt-to-assets, improving current ratio, no share dilution), and operating efficiency (improving gross margin, improving asset turnover). A score of 7 or higher means the company passes at least 7 of 9 criteria. These are financially healthy companies.

The second filter is the RSI-14 (Relative Strength Index over 14 periods). An RSI below 30 means the stock has dropped sharply and is in oversold territory. The combination targets companies that are strong but have been beaten down in price, which is the classic setup for mean reversion.

Portfolios rebalance quarterly. Each quarter, we screen for XETRA stocks with Piotroski >= 7 and RSI < 30. If 5 or more qualify, we hold them in equal weight for the quarter. If fewer than 5 qualify, the portfolio holds cash until the next rebalance.

For the full methodology, see our US flagship post.

The 35% Cash Rate: Feature or Bug?

This is the central question for any reader considering this strategy.

In 35% of quarters, the portfolio couldn't find 5 qualifying stocks and held cash instead. During long stretches of that 35%, German equities were rallying. Holding cash cost real returns.

But look at when the cash periods cluster. In 2000, the portfolio was fully in cash. XETRA, like most global markets, was in the tail end of a technology bubble where quality growth stocks had RSI readings well above 30. Holding cash in 2000 and early 2001 was objectively correct. In 2006, another extended cash period, Germany was in a sustained bull market. Quality blue chips had rising RSIs. The strategy correctly identified that there were no genuine deep-value opportunities and stepped aside.

The 2019, 2020, and 2022 results reinforce the framing. In 2019, when the strategy was deployed, it returned +51.28% against SPY's +32.31%, a 18.96% excess. In 2020, +39.30% vs +15.64%, a 23.66% excess. In 2022, when SPY fell -18.99%, the portfolio returned +1.40%, a 20.39% excess return in a down year. These are the quarters when fear drove quality German stocks to RSI < 30, and the strategy deployed into genuinely distressed but sound companies.

The counterargument is honest. When the portfolio is in cash, you're earning near-zero returns while equities compound. From 2013 through most of 2016, Germany had a strong equity run, and extended cash periods in those years produced drag that shows up as a -16.54% excess in 2006 and -10.26% in 2013. Over a full cycle, the cost of selectivity is real.

The honest framing: the strategy is designed to fire only when two independent signals align. RSI < 30 doesn't happen to quality stocks in normal markets. It happens during European debt crises, global selloffs, sector rotations, and moments of genuine fear. In those moments, German quality companies have historically recovered. The 35% cash rate reflects how often those moments actually occurred.

Investors need to decide whether that selectivity appeals to them. Some find it disciplined. Others find it frustrating.

Annual Returns

| Year | Portfolio | SPY | Excess |

|---|---|---|---|

| 2000 | 0.0% | -10.50% | +10.50% |

| 2001 | +8.48% | -9.17% | +17.65% |

| 2002 | -13.04% | -19.92% | +6.88% |

| 2003 | +23.17% | +24.12% | -0.96% |

| 2004 | -2.53% | +10.24% | -12.77% |

| 2005 | +4.53% | +7.17% | -2.64% |

| 2006 | -2.90% | +13.65% | -16.54% |

| 2007 | -18.10% | +4.40% | -22.50% |

| 2008 | -29.75% | -34.31% | +4.56% |

| 2009 | +12.98% | +24.73% | -11.75% |

| 2010 | +15.37% | +14.31% | +1.06% |

| 2011 | -15.45% | +2.46% | -17.91% |

| 2012 | +14.29% | +17.09% | -2.80% |

| 2013 | +17.52% | +27.77% | -10.26% |

| 2014 | +59.06% | +14.50% | +44.56% |

| 2015 | -12.65% | -0.12% | -12.53% |

| 2016 | +23.58% | +14.45% | +9.12% |

| 2017 | +2.58% | +21.64% | -19.07% |

| 2018 | -15.80% | -5.15% | -10.65% |

| 2019 | +51.28% | +32.31% | +18.96% |

| 2020 | +39.30% | +15.64% | +23.66% |

| 2021 | +14.60% | +31.26% | -16.67% |

| 2022 | +1.40% | -18.99% | +20.39% |

| 2023 | +3.72% | +26.00% | -22.28% |

| 2024 | +6.01% | +25.28% | -19.28% |

| 2025 | +8.26% | +15.34% | -7.07% |

The Standout Years

2014 is the most striking single year in the dataset. The portfolio returned +59.06% against SPY's +14.50%, a 44.56% excess. This followed the European sovereign debt crisis and its aftermath, where quality German industrials and financials had been progressively beaten down between 2011 and 2013. When the ECB's policy stance shifted, these stocks recovered fast. Companies with Piotroski scores of 7 or 8 that had been dragged down by macro fear, not operational weakness, snapped back.

2019 and 2020 form a coherent pair. In late 2018 and early 2019, trade war fears and rate hike concerns pushed quality XETRA stocks to RSI < 30. The 2019 recovery was sharp: +51.28%. Then in Q1 2020, COVID crashed markets globally and drove RSI readings below 30 on genuinely excellent German manufacturers and exporters. The 2020 result of +39.30% came from buying those companies at panic prices in March and holding through the recovery.

2022 shows the defensive character. SPY fell -18.99% in the worst bond-and-equity downturn since 2008. The portfolio returned +1.40%. The combination of quality companies and oversold entry conditions meant the portfolio was in names that had already corrected before the broader market declined, providing a natural cushion.

Why the Risk Profile is Different

The 19.52% annualized volatility is the lowest of any exchange where this strategy is worth discussing. That's not an accident. XETRA quality companies filtered at Piotroski >= 7 tend to be industrials, chemicals, and mid-cap manufacturers with stable cash flows. They're not momentum stocks. When they do get oversold, they don't move with the violent beta of tech or biotech.

The 59.6% down-capture means that when SPY fell by 10%, this portfolio typically fell by about 6%. Over 25 years with multiple bear markets, that difference compounds. It explains how a portfolio with a CAGR 2.25 percentage points below SPY can still produce a higher Sharpe ratio: it took less risk per unit of return.

The up-capture of 70.3% is the honest cost. The portfolio captures about 70% of SPY's gains in good years. That asymmetry (70% of upside, 60% of downside) is favorable, but not enough to overcome the 35% cash drag over a full cycle.

Screener: Current XETRA Quality Stocks

The query below identifies XETRA stocks that pass the quality half of this screen right now. RSI filtering requires real-time price data and isn't included here.

SELECT

k.symbol,

p.companyName,

ROUND(k.returnOnAssetsTTM * 100, 1) AS roa_pct,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(k.incomeQualityTTM, 2) AS income_quality,

ROUND(k.currentRatioTTM, 2) AS current_ratio,

ROUND(k.netDebtToEBITDATTM, 2) AS net_debt_ebitda,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM key_metrics_ttm k

JOIN profile p ON k.symbol = p.symbol

WHERE k.returnOnAssetsTTM > 0

AND k.returnOnEquityTTM > 0.10

AND k.incomeQualityTTM > 1.0

AND k.currentRatioTTM > 1.0

AND k.netDebtToEBITDATTM BETWEEN -10 AND 3.0

AND k.marketCap > 500000000 -- €500M+ for Germany

AND p.exchange IN ('XETRA')

ORDER BY k.symbol

Run this on the Ceta Research Data Explorer.

Limitations

This backtest uses point-in-time Piotroski scoring based on the most recent quarterly filings available at each rebalance date. Look-ahead bias is a risk in any backtest, and while we apply reasonable safeguards, results from the 2000-2005 period (when XETRA had fewer reporting standards in our database) should be interpreted with more caution than later periods.

The RSI threshold of 30 is strict. Looser thresholds (RSI < 40, RSI < 45) would increase invested periods and potentially improve absolute CAGR, but would capture stocks that aren't genuinely in stress territory. The 35% cash rate is a direct consequence of applying a disciplined threshold rather than a relaxed one.

Transaction costs are estimated at 0.1% per trade each way. Quarterly rebalancing with an average of 13.8 stocks per period means moderate turnover. Actual costs depend on broker and position size.

Part of a Series

This is one post in our global Oversold Quality series:

- Oversold Quality US: Full Strategy Explanation and Results (flagship)

- Oversold Quality China: Near-Parity with SPY on A-Shares

- Oversold Quality Global: 16 Exchanges Compared

Data: FMP warehouse, 2000-2025. Backtest framework: ceta-research/backtests. TTM metrics as of backtest run date.