Oversold Quality Global: 16 Exchanges Tested, None Beat the Index

Contents

- Summary Table

- The Strategy

- Tier Analysis

- Tier 1: Functional (21-43% cash rate)

- Tier 2: Borderline (45-78% cash rate)

- Tier 3: Not Worth Running (67-97% cash rate)

- Why Cash Periods Drive Performance

- The Standout Exchanges

- When the Strategy Works Globally

- Limitations

- Part of a Series

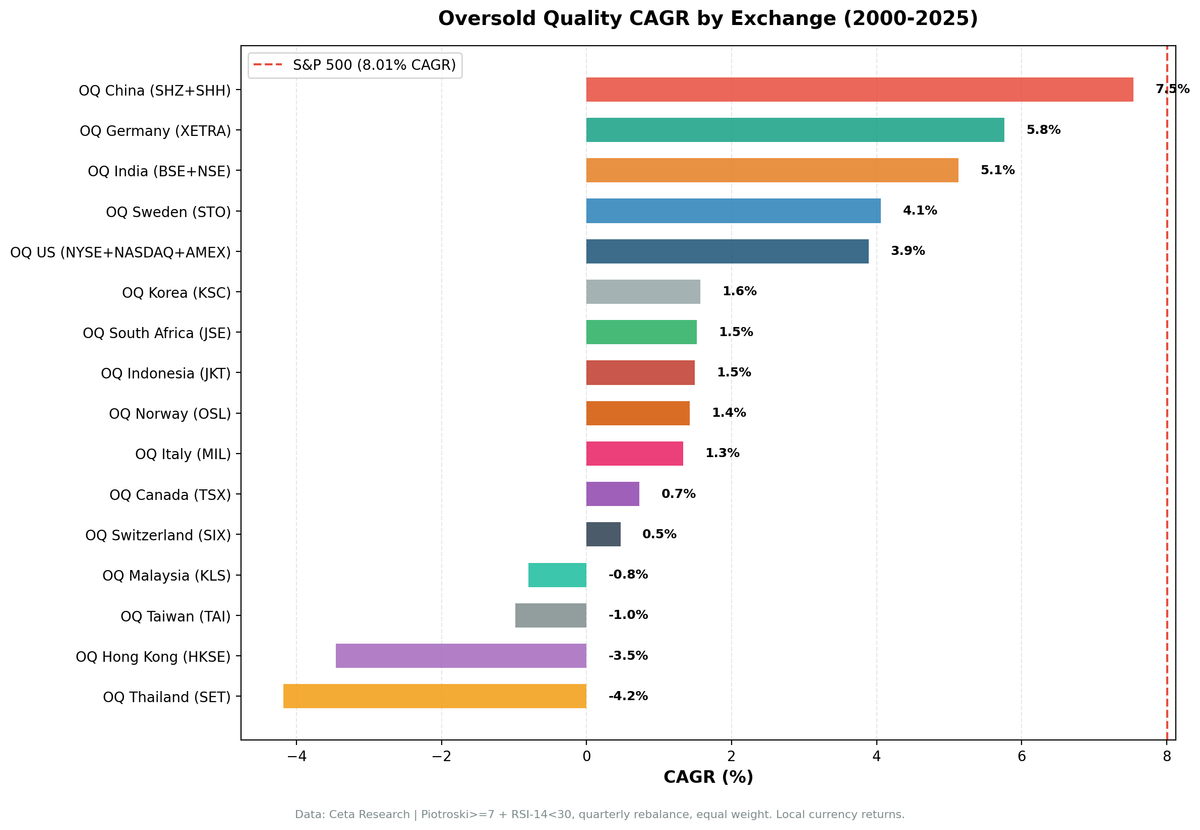

We ran the Oversold Quality strategy on 16 stock exchanges, 25 years of data, over 103 quarterly rebalance periods per exchange. The strategy didn't beat SPY on any of them. That's the honest result, and it's the right place to start.

But the variation across exchanges is large, and understanding why helps clarify what the strategy is actually doing. China trailed SPY by just -0.47% annually. Thailand trailed by -12.19%. Germany produced the best risk-adjusted return in the entire set. Most exchanges in between spent so much time in cash that the results aren't statistically meaningful. The cash rate explains most of this variation, and cash periods are themselves explained by market regime.

Summary Table

| Exchange | CAGR | Excess vs SPY | Sharpe | Max Drawdown | Cash Rate | Avg Stocks |

|---|---|---|---|---|---|---|

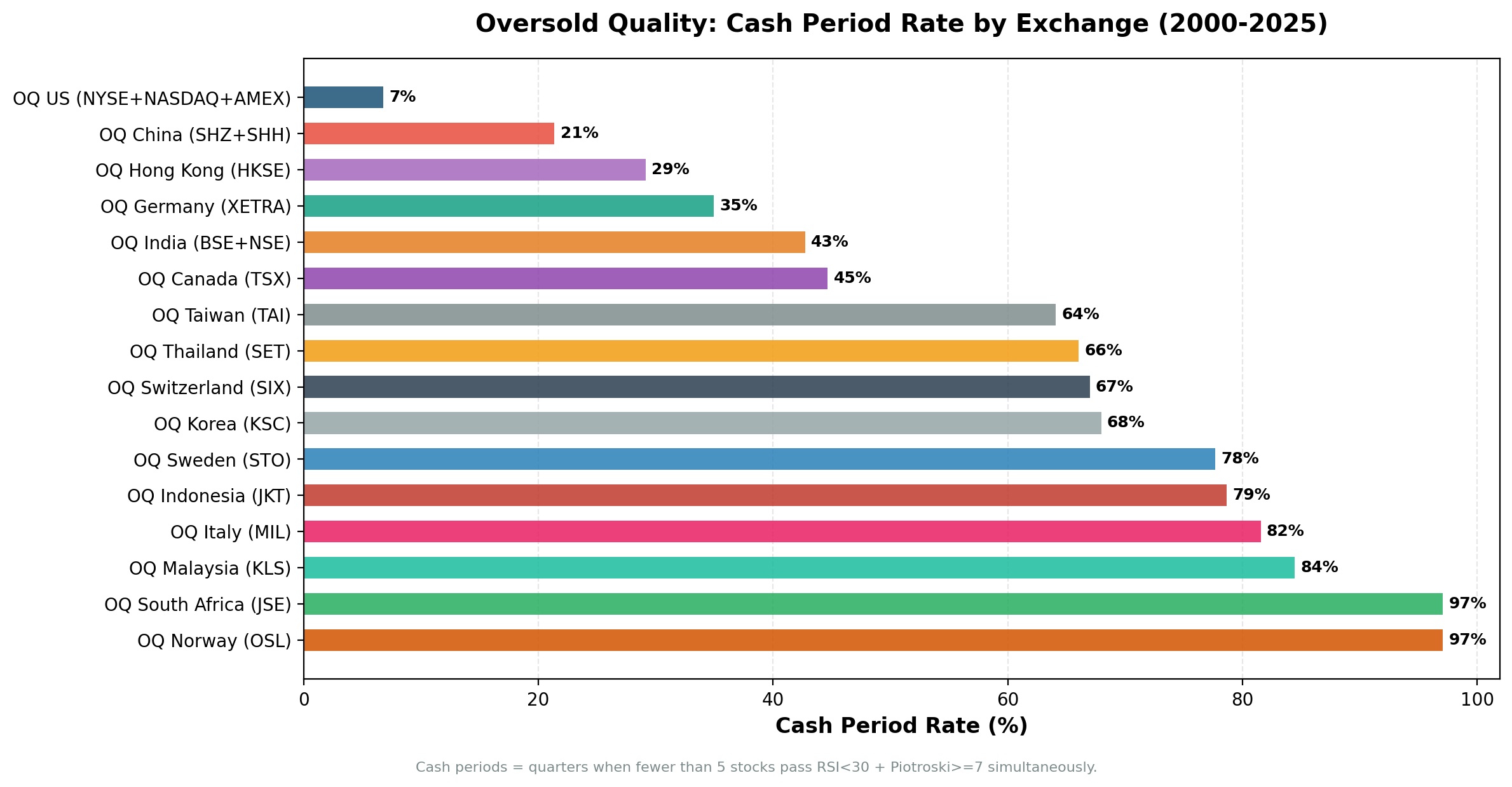

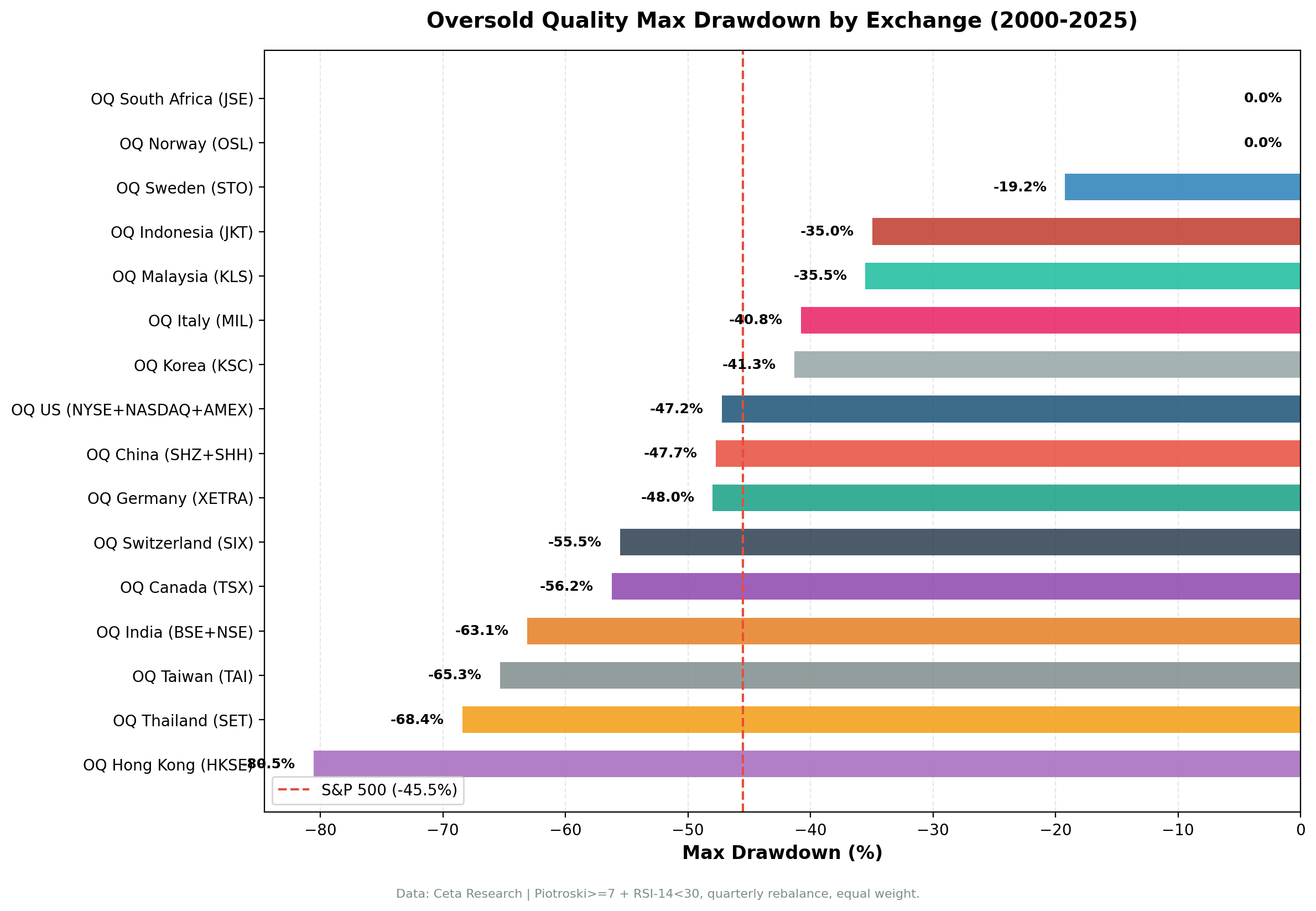

| China (SHZ+SHH) | 7.54% | -0.47% | 0.167 | -47.7% | 21% | 25.2 |

| Germany (XETRA) | 5.76% | -2.25% | 0.193 | -48.0% | 35% | 13.8 |

| India (BSE+NSE) | 5.13% | -2.88% | -0.060 | -63.1% | 43% | 20.6 |

| Sweden (STO) | 4.06% | -3.95% | 0.126 | -19.2% | 78% | 11.7 |

| US (NYSE+NASDAQ+AMEX) | 3.89% | -4.12% | 0.087 | -47.2% | 7% | 23.2 |

| Korea (KSC) | 1.57% | -6.44% | -0.111 | -41.3% | 68% | 13.8 |

| South Africa (JNB) | 1.52% | -6.49% | -1.398 | 0.0%* | 97% | 8.3 |

| Indonesia (JKT) | 1.49% | -6.52% | -0.056 | -35.0% | 79% | 8.5 |

| Norway (OSL) | 1.42% | -6.59% | -0.318 | 0.0%* | 97% | 8.3 |

| Italy (MIL) | 1.33% | -6.68% | -0.165 | -40.8% | 82% | 8.2 |

| Canada (TSX) | 0.73% | -7.29% | -0.094 | -56.2% | 45% | 11.4 |

| Switzerland (SIX) | 0.47% | -7.54% | -0.003 | -55.5% | 67% | 12.8 |

| Malaysia (KLS) | -0.80% | -8.81% | -0.350 | -35.5% | 84% | 7.2 |

| Taiwan (TAI) | -0.98% | -8.99% | -0.137 | -65.3% | 64% | 14.6 |

| Hong Kong (HKSE) | -3.46% | -11.47% | -0.259 | -80.5% | 29% | 14.0 |

| Thailand (SET) | -4.18% | -12.19% | -0.386 | -68.4% | 66% | 15.6 |

*South Africa and Norway show 0.0% max drawdown because both had 97% cash rates. With only ~3 invested quarters across 25 years, there were almost no periods where drawdown could be measured. The strategy essentially never deployed capital on these exchanges.

SPY benchmark CAGR: 8.01% (2000-2025).

The Strategy

Oversold Quality screens for stocks that are financially healthy but have been beaten down in price. The Piotroski F-Score (nine-point accounting quality test) must be 7 or higher, requiring the company to pass at least 7 of 9 criteria across profitability, leverage, and operating efficiency. The RSI-14 (Relative Strength Index over 14 periods) must be below 30, indicating the stock has sold off sharply into technically oversold territory.

Each quarter, exchanges are screened for stocks meeting both criteria. If 5 or more qualify, they're held in equal weight for the quarter. If fewer than 5 qualify, the portfolio holds cash.

For full strategy mechanics, see the US flagship post.

Tier Analysis

Tier 1: Functional (21-43% cash rate)

China, Germany, India, and US are the only exchanges where the strategy produced enough invested periods to draw conclusions. Cash rates range from 7% in the US (where the strategy almost always finds enough oversold quality names) to 43% in India.

China leads at 7.54% CAGR, trailing SPY by just -0.47% over 25 years. Germany trails by -2.25% but has the best Sharpe ratio (0.193) and lowest volatility in the set. India trails by -2.88%. The US is in this tier with only 7% cash rate, but trails by -4.12%, meaning the US market offers enough volume of quality oversold stocks but the returns haven't been strong enough to compensate for the selectivity.

These four exchanges are worth running the strategy on. The signals are frequent enough to be statistically meaningful, and the selection quality (when the strategy does invest) appears to reflect genuinely stressed but sound companies.

Tier 2: Borderline (45-78% cash rate)

Sweden, Korea, Canada, Switzerland, and Taiwan sit in an uncomfortable middle. Cash rates between 45% and 78% mean these portfolios spent roughly half to three-quarters of the time doing nothing. The strategy occasionally deployed into stocks that recovered, but not often enough to matter over a full cycle.

Sweden's Sharpe of 0.126 is positive, which is notable for a strategy spending 78% of the time in cash. When the Swedish market does produce quality oversold signals, they tend to cluster during genuine macro stress (the European debt crisis, COVID), and Swedish quality industrials can recover sharply. But 78% cash means the portfolio is essentially a cash account with occasional equity exposure.

Korea, Canada, Switzerland, and Taiwan all have negative Sharpe ratios. The invested periods didn't produce enough return to justify the selectivity. These aren't candidates for practical implementation.

Tier 3: Not Worth Running (67-97% cash rate)

Norway, South Africa, Malaysia, Indonesia, Italy, Hong Kong, and Thailand essentially never deployed meaningful capital. Norway and South Africa had 97% cash rates, meaning only about 3 quarters across the entire 25-year period had 5 or more qualifying stocks. The results are statistically meaningless.

Italy (82% cash), Malaysia (84% cash), Indonesia (79% cash), and Thailand (66% cash) are in similar territory. Hong Kong is an outlier here: it has a more reasonable 29% cash rate but still produced -3.46% CAGR and -80.5% max drawdown. HKSE's problem isn't cash rate; it's that the quality oversold stocks it selected during stress periods (2008, 2015, 2019 protests, 2020) didn't recover on the timeline of this strategy.

We note these exchanges in the table for completeness, but won't draw directional conclusions from any of them.

Why Cash Periods Drive Performance

The RSI < 30 filter is the binding constraint. Quality companies (Piotroski >= 7) are reasonably common on any large exchange. Companies that are simultaneously high-quality and trading at RSI < 30 aren't.

RSI drops below 30 only during sustained sell-offs. Not minor pullbacks. Quality companies typically don't get to RSI < 30 in healthy markets because they have steady earnings, low debt, and improving fundamentals that attract buyers on dips. They reach RSI < 30 when macro fear overrides fundamentals: market-wide crashes, sector rotations, currency crises, geopolitical shock.

This means the strategy is regime-dependent. On exchanges with frequent stress episodes and active local investor bases that sell quality stocks during those episodes, the signal fires often. On exchanges where bull markets run long and corrections are shallow, quality stocks rarely get to RSI < 30, and the portfolio stays in cash.

The cash rate pattern maps cleanly onto market structure:

- China (21% cash): A-shares have regular domestic policy-driven volatility cycles that push quality stocks into RSI < 30 independent of the US market cycle. The Chinese government's periodic tightening campaigns, sector crackdowns, and exchange circuit breakers create conditions where quality companies sell off hard.

- Germany (35% cash): XETRA quality stocks went oversold during the European sovereign debt crisis (2010-2012), the 2018 global equity selloff, and COVID. The exchange has enough genuine stress events to generate signals.

- US (7% cash): The US has the deepest and most volatile equity market. Quality US stocks routinely get beaten down during sector rotations, earnings-driven selloffs, and macro fear events, even in otherwise healthy markets. The signal fires almost every quarter.

- Nordic markets (67-97% cash): Sweden, Norway experienced long domestic bull markets with few deep corrections. Quality Nordic companies tend to attract steady institutional buying on any dip, keeping RSIs elevated.

The Standout Exchanges

China is the clearest near-success. A 7.54% CAGR against SPY's 8.01% over 25 years, with a Sharpe of 0.167, is the strongest absolute result in this series. A-share markets have genuine episodic volatility that the strategy exploits well. Quality A-share companies selected during China's own bear cycles (2008-2009, 2011, 2015, 2018) recovered strongly.

Germany has the best Sharpe ratio (0.193), lowest volatility (19.52%), and strongest down-capture protection (59.6%). The -2.25% annual excess return is real, but Germany's defensive profile means it protects capital during drawdowns better than any other exchange. Full Germany analysis here.

Sweden's Sharpe of 0.126 is worth noting as the only other exchange with a positive Sharpe besides China, Germany, and the US. The -19.2% max drawdown (lowest in the entire set) and high cash rate suggest the Swedish portfolio is almost equity-averse, but when it does invest, it tends to pick well.

Hong Kong is the cautionary example. A 29% cash rate is comparable to Germany, but -80.5% max drawdown and -3.46% CAGR. The difference: HKSE quality stocks that got oversold during the protest-era (2019) and COVID selloff didn't recover within the quarterly rebalance window. Some didn't recover at all. The combination of political risk, regulatory uncertainty, and the structural shift of Hong Kong's equity market composition in this period meant that Piotroski filtering couldn't protect against permanent capital loss in several positions.

When the Strategy Works Globally

The common thread across China and Germany (the two most defensible results) is market structure that produces genuine, isolated stress events on quality companies. Both exchanges have large domestic institutional investor bases, significant foreign investor participation, and episodic crises that are local or regional rather than global in origin.

When global crises hit (2008, COVID), every exchange saw RSI < 30 on quality stocks simultaneously. The strategy fired on most exchanges at once and generally recovered with the market. The exchanges that outperform are those that have additional local stress episodes: China's policy cycles, Germany's European crisis exposure.

The strategy's core logic is sound. Quality companies that are genuinely oversold do tend to recover. The problem is that "genuinely oversold" (RSI < 30) is rare for quality companies in normal market conditions, and when it does happen, the recovery timeline varies. 13 of 16 exchanges showed the recovery timing was insufficient to compensate for the cash drag and selection risk over a full 25-year cycle.

Limitations

Statistical significance: The bottom tier of exchanges (Norway, South Africa, most of Tier 2) have so few invested periods that results are noise. We've included them in the table for completeness, but drawing strategy conclusions from 3-6 invested quarters over 25 years isn't valid.

Look-ahead bias: Piotroski scoring uses the most recent quarterly filings available at each rebalance date. In earlier periods (2000-2005), data completeness varies by exchange, with non-US markets having larger gaps. Results from those years carry more uncertainty.

RSI threshold sensitivity: This backtest uses RSI < 30. Relaxing to RSI < 35 or RSI < 40 would increase invested periods substantially and likely improve absolute CAGR at the cost of selection quality. We haven't run those variants globally. Different RSI thresholds might improve results on Tier 2 exchanges.

Currency effects: All returns are computed in local currency. A USD-denominated investor in XETRA or HKSE would have different returns depending on EUR/USD and HKD/USD exchange rate moves over the period.

Transaction costs: Estimated at 0.1% per trade each way. Actual costs on markets like Indonesia, Malaysia, or Thailand may be higher, particularly for mid-cap names.

Part of a Series

This is the global comparison post in the Oversold Quality series:

- Oversold Quality US: Full Strategy Explanation and Results (flagship, full methodology)

- Oversold Quality China: Near-Parity with SPY on A-Shares

- Oversold Quality Germany: Best Risk-Adjusted Returns in the Series

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: FMP warehouse, 2000-2025. Backtest framework: ceta-research/backtests. TTM metrics as of backtest run date.