Japan P/E Compression: +2.25% Annual Alpha vs Nikkei 225

P/E compression on Japanese stocks returns 5.20% annually vs 2.95% for the Nikkei 225, beating the local benchmark by 2.25% per year with 52% down-capture. The strategy works in Japan when compared against the correct local benchmark.

We tested P/E compression mean reversion on 25 years of Japanese stock data. The strategy returned 5.20% annually (JPY-denominated) vs 2.95% for the Nikkei 225, with 2.25% excess return. When compared to the correct local benchmark, P/E compression works in Japan. The key: Japan's equity market has been a poor benchmark. The strategy doesn't need to beat the S&P 500. It needs to beat what a Japanese investor could otherwise hold.

Contents

- Method

- What We Found

- 25 years. +2.25% annual alpha vs Nikkei 225. Consistent downside protection.

- Why P/E Compression Works in Japan (vs Local Benchmark)

- Honest Caveats

- Year-by-year returns

- 2000-2002: cash avoided the Nikkei crash

- 2008 and 2018: where the strategy bleeds

- 2023-2024: the growth rotation challenge

- Backtest Methodology

- Limitations

- Conclusion

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: JPX, market cap > ¥100B Period: 2000-2025 (25 years, 25 annual periods) Rebalancing: Annual (January), equal weight, top 30 by compression ratio Benchmark: Nikkei 225 (JPY, local benchmark) Cash rule: Hold cash if fewer than 10 stocks qualify

Returns are in JPY. The Nikkei 225 is the local benchmark a Japanese investor would compare against.

What We Found

25 years. +2.25% annual alpha vs Nikkei 225. Consistent downside protection.

| Metric | P/E Compression (Japan) | Nikkei 225 |

|---|---|---|

| CAGR | 5.20% | 2.95% |

| Excess CAGR | +2.25% | - |

| Sharpe Ratio | 0.250 | - |

| Max Drawdown | -52.28% | - |

| Up Capture | 89.87% | 100% |

| Down Capture | 51.66% | 100% |

| Avg Stocks per Year | 28.0 | - |

| Cash Periods | 4 of 25 (16%) | - |

The strategy beats Japan's equity market by 2.25% annually over 25 years. The 52% down-capture is particularly strong: when the Nikkei fell 10%, this portfolio fell 5.2% on average. That's meaningful downside protection in a market that has had severe drawdown periods.

The four cash periods (2000-2002 and 2003) are actually a feature, not a bug. Those were years when the Nikkei was collapsing after the tech bubble. Being in cash and earning nothing beats losing 20% per year.

Why P/E Compression Works in Japan (vs Local Benchmark)

The Nikkei 225 is a weak benchmark. Over 25 years, the Nikkei returned only 2.95% annually. Japan's structural deflation, corporate governance reform cycle, and low earnings growth kept the index suppressed for decades. Beating 2.95% is not a high bar.

Quality filters exclude zombie companies. Japan has many cash-rich but low-return companies. The ROE > 10% filter eliminates these. What remains are companies that are profitable but temporarily unloved by the market. These do revert.

Deflation made P/E compression more common. In a deflationary environment, P/E ratios compress frequently as earnings stagnate or grow slowly. This creates more signals, but the quality filters ensure we're selecting companies with genuine business strength.

Abenomics created mean reversion opportunities. The post-2012 period saw significant corporate governance reforms and earnings improvements. Companies that had been trading at compressed multiples relative to their own history saw multiple expansion as ROE improved. The strategy captured this.

Honest Caveats

Lower CAGR than US. 5.20% vs 9.92% in the US. Japan delivers positive alpha but the absolute return is lower. A Japanese investor faces real currency and opportunity cost trade-offs.

High max drawdown. -52.28% is severe. The 2008 crisis hit Japanese stocks hard. A portfolio that can lose half its value needs to be sized appropriately.

Currency matters for international investors. The numbers here are in JPY. For a USD-based investor, JPY/USD movements add significant uncertainty. The +2.25% alpha vs Nikkei exists in JPY terms. In USD terms, the comparison is different.

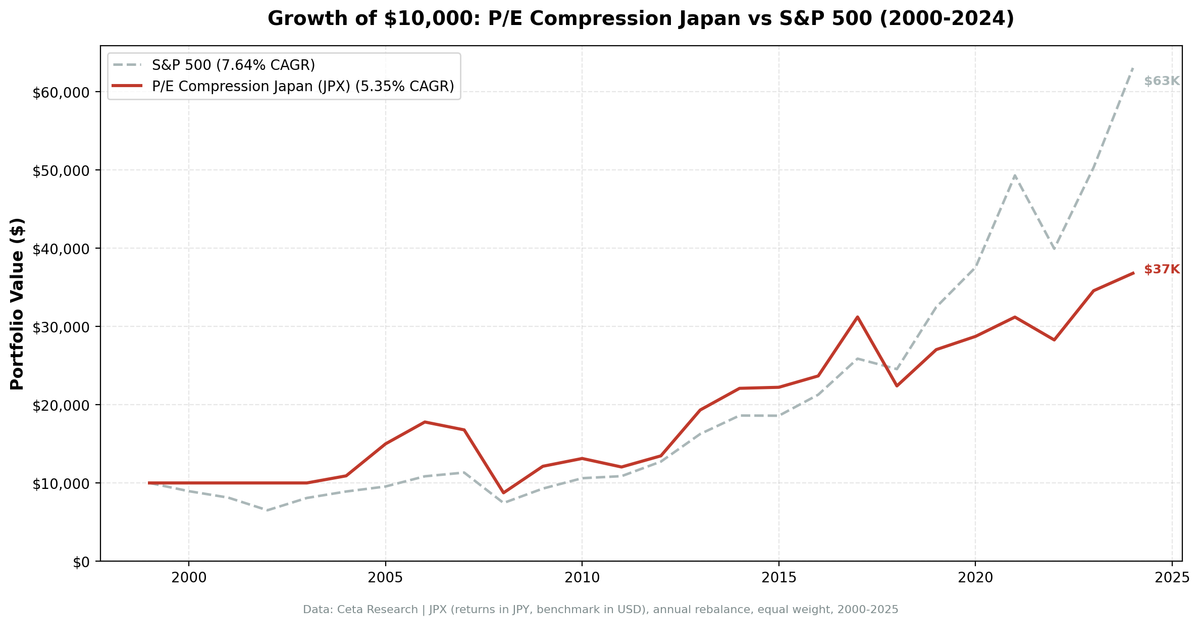

vs SPY, this strategy underperforms. The S&P 500 returned 7.64% annually over this period vs this strategy's 5.20%. Japanese equities broadly underperformed US equities. The question is whether Japanese investors should use this strategy relative to their domestic market, not whether they should prefer it over US equities.

Year-by-year returns

| Year | P/E Compression | Nikkei 225 | Excess |

|---|---|---|---|

| 2000 | +0.0% | -27.9% | +27.9% |

| 2001 | +0.0% | -20.6% | +20.6% |

| 2002 | +0.0% | -19.9% | +19.9% |

| 2003 | +0.0% | +24.2% | -24.2% |

| 2004 | +9.1% | +6.4% | +2.7% |

| 2005 | +46.3% | +42.0% | +4.3% |

| 2006 | +18.7% | +6.1% | +12.6% |

| 2007 | -5.5% | -15.3% | +9.9% |

| 2008 | -49.5% | -38.5% | -11.1% |

| 2009 | +32.7% | +17.8% | +14.9% |

| 2010 | +9.1% | -2.4% | +11.5% |

| 2011 | -7.3% | -17.7% | +10.3% |

| 2012 | +10.7% | +24.9% | -14.2% |

| 2013 | +43.2% | +48.9% | -5.7% |

| 2014 | +15.6% | +9.4% | +6.2% |

| 2015 | +0.0% | +6.0% | -6.0% |

| 2016 | +5.3% | +6.2% | -0.9% |

| 2017 | +31.8% | +20.0% | +11.8% |

| 2018 | -27.9% | -16.8% | -11.1% |

| 2019 | +23.6% | +18.6% | +5.0% |

| 2020 | +4.8% | +17.5% | -12.7% |

| 2021 | +8.9% | +7.5% | +1.4% |

| 2022 | -7.4% | -12.2% | +4.8% |

| 2023 | +18.0% | +29.4% | -11.4% |

| 2024 | +3.5% | +18.1% | -14.6% |

2000-2002: cash avoided the Nikkei crash

The three cash years at the start were a structural win. The screen couldn't find enough qualifying stocks in those years. The Nikkei fell 28%, 21%, and 20% in those three years. Being in cash with 0% return beat losing 60% cumulatively.

2008 and 2018: where the strategy bleeds

Two years showed double-digit underperformance: 2008 (-11%) and 2018 (-11%). Both were global risk-off events where Japanese quality stocks sold off harder than the Nikkei average. Forced selling doesn't discriminate by compression ratio.

2023-2024: the growth rotation challenge

The last two years showed significant underperformance as Nikkei surged on semiconductor and AI-adjacent stocks. P/E compression misses that wave by design. It selects for compressed multiples, which excludes anything trading at elevated valuations.

Backtest Methodology

Full methodology documentation: backtests/METHODOLOGY.md

| Parameter | Choice |

|---|---|

| Universe | JPX, Market Cap > ¥100B |

| Signal | Current P/E < 85% of 5-year avg, P/E 5-40, ROE > 10%, D/E < 2.0 |

| Portfolio | Top 30 by lowest compression ratio, equal weight |

| Rebalancing | Annual (January) |

| Cash rule | Hold cash if < 10 qualify |

| Benchmark | Nikkei 225 (^N225, JPY) |

| Period | 2000-2025 (25 years) |

| Data | Point-in-time (45-day lag on FY financial statements) |

| Transaction costs | 0.1% one-way (large cap tier) |

Limitations

High absolute drawdown. -52.28% max drawdown is severe, worse than the Nikkei's own worst periods. Japanese quality stocks can still get hit hard in global crises.

Low absolute CAGR. 5.20% annually is modest. The strategy works relative to Japan, but Japan itself is not a high-growth equity market.

Cash drag. 16% cash periods mean the portfolio misses parts of the Nikkei's occasional strong years (2003, 2013).

Currency risk for international investors. All returns are in JPY. USD/JPY can swing 20%+ in a year, overwhelming the 2.25% alpha.

Survivorship bias. Standard backtest limitation: exchange membership uses current profiles. Delistings over 25 years aren't fully tracked.

Conclusion

P/E compression beats Japan's local equity market by 2.25% annually over 25 years, with 52% down-capture versus the Nikkei 225. The strategy works in Japan, but only when measured against the correct benchmark.

The key distinction: Japan's equity market has been a weak benchmark. If you compare this strategy to US equities (SPY), Japan underperforms. If you compare it to what a Japanese investor can actually hold locally, the strategy adds value.

For Japanese investors or those with JPY exposure, P/E compression provides consistent outperformance over the domestic market with meaningful downside protection. The caveats are real: high absolute drawdown, modest absolute returns, and vulnerability to growth-led market phases.

Data: Ceta Research (FMP financial data warehouse). Returns in JPY. Past performance does not guarantee future results. See full methodology at github.com/ceta-research/backtests.