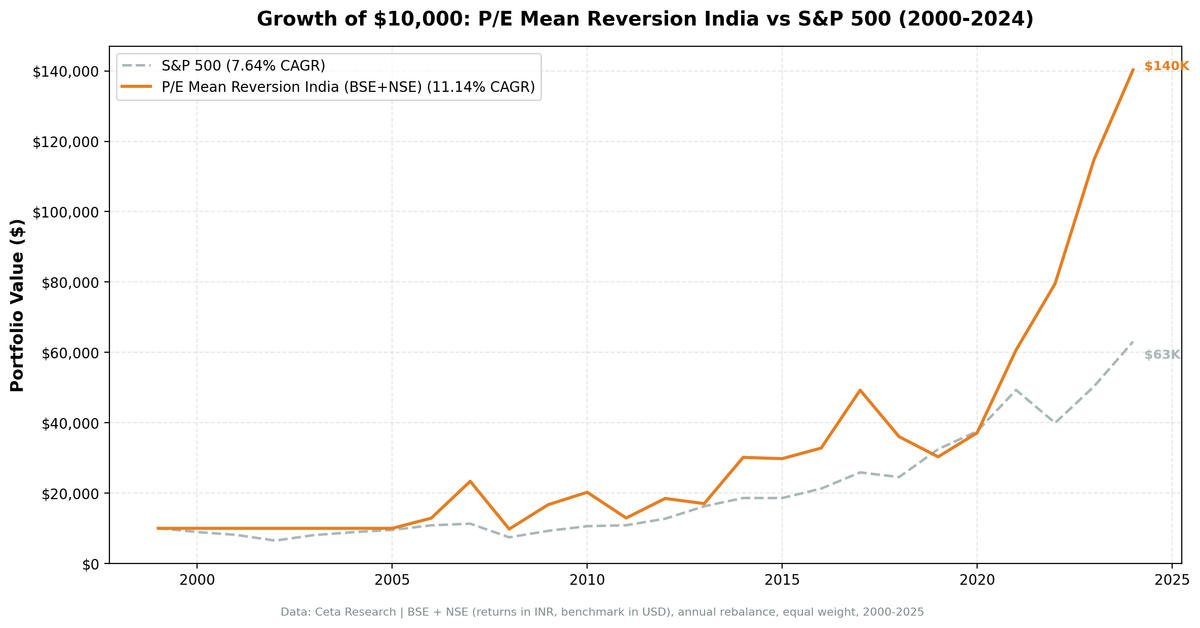

P/E Mean Reversion in India: 9.96% CAGR Over 19 Years, Trailing the Sensex by 1.5%

We tested a sector-relative P/E mean reversion screen on 25 years of Indian stock data from the NSE. The strategy returned 9.96% annually, which beats the S&P 500 (7.64%) but trails the Sensex (11.4%). Local benchmark matters: a strategy that looks like alpha vs SPY is actually slightly...

We tested a sector-relative P/E mean reversion screen on 25 years of Indian stock data from the NSE. The signal fires when a stock trades at a 40%+ discount to its sector peers on P/E, filtered for profitability and manageable debt. The strategy returned 9.96% annually, which beats the S&P 500's 7.64% but trails the Sensex's 11.4% CAGR. The local benchmark matters here. A strategy that looks like alpha vs a US index is actually slightly below-market vs the domestic one.

Contents

- Method

- What Is Sector-Relative P/E Mean Reversion?

- The Screen

- Sector-Relative P/E Screen for India (SQL)

- What We Found

- 19 effective years. Trails Sensex by 1.45%. High volatility in both directions.

- Year-by-year returns

- 2006–2007: India's bull market

- 2008: worst year

- 2009: dramatic recovery

- 2011 and 2013: domestic slowdowns

- 2014: Modi election rally

- 2019: the NBFC crisis

- 2021–2023: India's bull run

- Crisis comparison

- Backtest Methodology

- Limitations

- Conclusion

India is the most volatile market in this global study. Massive gains, severe drawdowns, and complete decoupling from US market cycles. This isn't a smooth ride.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: NSE, market cap > ₹20B INR Period: 2000–2024 (25 years), effective: 2006–2024 (19 invested years) Rebalancing: Annual (January), equal weight, top 30 by lowest P/E-to-sector ratio Benchmark: Sensex (^BSESN, price return) Cash rule: Hold cash if fewer than 10 stocks qualify

Financial data sourced from financial_ratios_ttm for P/E, key_metrics_ttm for ROE. 45-day lag on all financial statements to prevent look-ahead bias.

What Is Sector-Relative P/E Mean Reversion?

This strategy compares each stock's P/E to its sector peers, not to its own history. A tech stock trading at 12x when its sector median is 25x is flagged as deeply discounted. A consumer stock at 14x when its sector trades at 15x is not.

The bet: when a fundamentally healthy company trades at a large discount to sector norms, it tends to mean revert. Either the stock re-rates upward, or it gets acquired, or earnings growth closes the gap. This is cross-sectional value, not longitudinal compression.

Signal: - Stock P/E < 60% of sector median P/E (40%+ discount to peers) - P/E range: 3–50 (exclude extreme valuations) - Minimum 5 stocks in sector to calculate a valid median

Quality filters:

| Criterion | Metric | Threshold |

|---|---|---|

| Profitable | Return on Equity | > 8% |

| Manageable debt | Debt-to-Equity | < 2.0 |

Size:

| Criterion | Metric | Threshold |

|---|---|---|

| Meaningful liquidity | Market Cap | > ₹20B INR |

Stocks must pass all filters. The top 30 by lowest P/E-to-sector ratio are selected each year, equal weighted.

The Screen

Sector-Relative P/E Screen for India (SQL)

WITH universe AS (

SELECT k.symbol, p.companyName, p.exchange, p.sector,

fr.priceToEarningsRatioTTM AS pe_ttm, k.returnOnEquityTTM AS roe,

fr.debtToEquityRatioTTM AS de, k.marketCap

FROM key_metrics_ttm k

JOIN financial_ratios_ttm fr ON k.symbol = fr.symbol

JOIN profile p ON k.symbol = p.symbol

WHERE fr.priceToEarningsRatioTTM BETWEEN 3 AND 50

AND k.returnOnEquityTTM > 0.08

AND (fr.debtToEquityRatioTTM IS NULL OR (fr.debtToEquityRatioTTM >= 0 AND fr.debtToEquityRatioTTM < 2.0))

AND k.marketCap > 20000000000

AND p.sector IS NOT NULL

AND p.exchange = 'NSE'

),

sector_medians AS (

SELECT sector,

PERCENTILE_CONT(0.5) WITHIN GROUP (ORDER BY pe_ttm) AS median_pe,

COUNT(*) AS n_sector_stocks

FROM universe GROUP BY sector HAVING COUNT(*) >= 5

)

SELECT u.symbol, u.companyName, u.exchange, u.sector,

ROUND(u.pe_ttm, 2) AS pe_ttm, ROUND(sm.median_pe, 2) AS sector_median_pe,

ROUND(u.pe_ttm / sm.median_pe, 3) AS pe_ratio_to_sector,

ROUND((1 - u.pe_ttm / sm.median_pe) * 100, 1) AS discount_pct,

ROUND(u.roe * 100, 1) AS roe_pct, ROUND(u.de, 2) AS debt_to_equity,

ROUND(u.marketCap / 1e9, 0) AS mktcap_b_inr

FROM universe u JOIN sector_medians sm ON u.sector = sm.sector

WHERE u.pe_ttm / sm.median_pe < 0.60

ORDER BY u.pe_ttm / sm.median_pe ASC LIMIT 30

Run this query on Ceta Research

What We Found

19 effective years. Trails Sensex by 1.45%. High volatility in both directions.

| Metric | P/E Mean Reversion (India) | Sensex |

|---|---|---|

| CAGR | 9.96% | 11.40% |

| Total Return | 972.95% | 1,387.29% |

| Sharpe Ratio | 0.099 | — |

| Sortino Ratio | 0.188 | — |

| Max Drawdown | -62.16% | -51.34% |

| Up Capture | 95.41% | 100% |

| Down Capture | 77.71% | 100% |

| Excess vs Sensex | -1.45% | — |

| Avg Stocks per Year | 25.3 | — |

| Cash Periods | 6 of 25 (all 2000–2005) | — |

The strategy trails the Sensex over 25 years. Up-capture of 95% and down-capture of 78% means it roughly tracks the index with slightly more downside. The Sharpe ratio of 0.099 is low, driven by 35%+ annual volatility.

This is a different story than comparing against the S&P 500. The strategy beats SPY (9.96% vs 7.64%) because the Sensex itself beat SPY by a wide margin over this period. A strategy returning 9.96% looks like alpha vs SPY but is slightly below-market vs its own index.

One important caveat on the data. The backtest covers 2000–2024, but the strategy holds cash for all six years from 2000 through 2005. FMP's coverage of Indian markets before 2006 is thin: not enough qualifying stocks pass the quality and market cap filters to form a portfolio. The effective backtest runs 2006–2024, covering 19 years. Any interpretation of long-run performance should start from 2006.

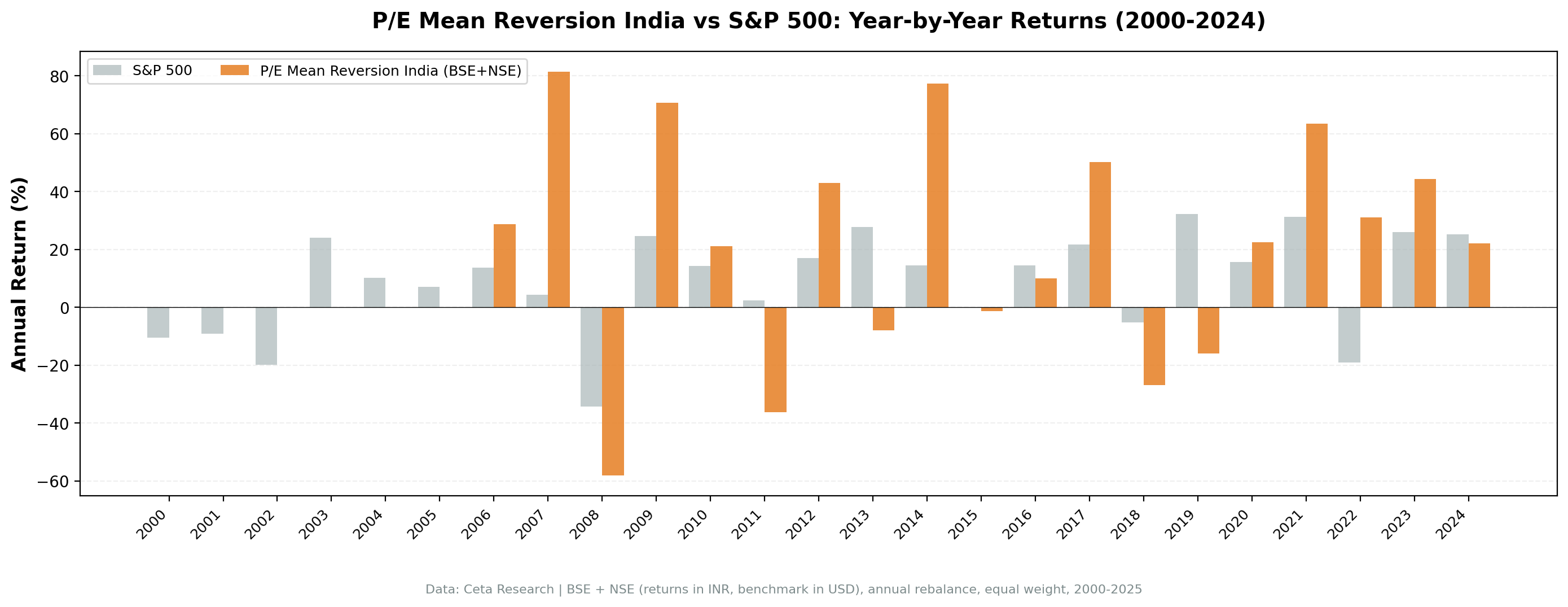

Year-by-year returns

| Year | India P/E MR | Sensex | Excess |

|---|---|---|---|

| 2000 | Cash (0.0%) | -25.2% | — |

| 2001 | Cash (0.0%) | -18.6% | — |

| 2002 | Cash (0.0%) | +2.9% | — |

| 2003 | Cash (0.0%) | +79.1% | — |

| 2004 | Cash (0.0%) | +10.8% | — |

| 2005 | Cash (0.0%) | +40.6% | — |

| 2006 | +29.9% | +48.5% | -18.6% |

| 2007 | +72.9% | +46.8% | +26.1% |

| 2008 | -62.2% | -51.3% | -10.8% |

| 2009 | +93.6% | +76.3% | +17.3% |

| 2010 | +19.6% | +17.1% | +2.5% |

| 2011 | -32.5% | -24.5% | -8.0% |

| 2012 | +45.4% | +27.0% | +18.3% |

| 2013 | -9.7% | +6.0% | -15.6% |

| 2014 | +59.7% | +33.5% | +26.2% |

| 2015 | -4.7% | -8.1% | +3.4% |

| 2016 | +20.3% | +3.8% | +16.5% |

| 2017 | +41.3% | +27.1% | +14.2% |

| 2018 | -30.5% | +6.2% | -36.7% |

| 2019 | -6.6% | +16.0% | -22.6% |

| 2020 | +17.7% | +15.7% | +2.0% |

| 2021 | +45.2% | +22.9% | +22.4% |

| 2022 | +13.2% | +3.4% | +9.8% |

| 2023 | +53.4% | +17.5% | +35.8% |

| 2024 | +23.4% | +11.2% | +12.2% |

2006–2007: India's bull market

The strategy started strong in 2007, though it lagged the index in 2006. India was in the middle of a sustained economic expansion. +29.9% in 2006 (vs Sensex +48.5%), then +72.9% in 2007 (vs Sensex +46.8%). The 2007 outperformance shows the sector-relative signal working as expected: discounted stocks caught up to sector peers during a broad rally.

This is the strategy doing exactly what it's designed to do: cheap-to-peers stocks catching up when the market is rising broadly.

2008: worst year

-62.2% in a single year. India suffered a severe bear market as global capital fled emerging markets. Quality filters didn't help. When beta amplifies a global sell-off, sector-relative discount protection breaks down. The max drawdown of -62.16% is the deepest in this global study.

The comparison to Sensex (-51.3%) shows the strategy amplified the Indian market's losses. The sector-relative screen loaded up on stocks trading at discounts to their peers, but in a panic selloff, those discounts widened rather than closed. Indian equities have high beta to global risk-off events. The strategy didn't cushion that.

2009: dramatic recovery

+93.6% in 2009. This is the flip side of India's high beta. When global markets recovered, Indian value stocks snapped back hard. The 2008 drawdown was severe, but 2009 more than recovered it in a single year. The strategy beat Sensex by +17.3% in the recovery, showing the sector-discount signal working in a rising market.

2011 and 2013: domestic slowdowns

Two painful years for Indian equities driven by domestic issues. 2011: -32.5% vs Sensex -24.5%. 2013: -9.7% vs Sensex +6.0%. These were India-specific corrections driven by inflation, policy uncertainty, and slowing growth. The strategy underperformed the index in both years. India was its own story.

2014: Modi election rally

+59.7% vs Sensex +33.5%, a +26.2% excess. The BJP election win in May 2014 triggered a significant re-rating of Indian equities. Investors priced in economic reform and improved business conditions. The sector-relative signal had been sitting on discounted stocks through the 2012–2013 weakness, and the 2014 rally closed those gaps fast. One of the clearest examples of political catalyst driving value mean reversion.

2019: the NBFC crisis

-6.6% vs Sensex +16.0%, a -22.6% excess. This was not a global event. India's non-bank financial company (NBFC) sector collapsed after the IL&FS default in late 2018, triggering a domestic credit crunch. Financial sector stocks, which would have been well-represented in a value screen after the 2018 drawdown, continued falling. The strategy picked up exactly the sector the domestic crisis was targeting.

This is the critical risk in India: domestic idiosyncratic events that have nothing to do with global markets. You can't hedge this from outside India.

2021–2023: India's bull run

+45.2% in 2021 (vs Sensex +22.9%), +13.2% in 2022 (vs Sensex +3.4%), +53.4% in 2023 (vs Sensex +17.5%). Three strong years of outperformance. India's domestic economy recovered strongly from COVID, capital flows returned to emerging markets, and corporate earnings accelerated. The strategy beat the Sensex significantly across this period, showing the sector-relative signal working in a broad bull market.

Crisis comparison

| Event | India P/E MR | Sensex | Gap |

|---|---|---|---|

| Global financial crisis (2008) | -62.2% | -51.3% | -10.8% |

| India domestic slowdown (2011) | -32.5% | -24.5% | -8.0% |

| Modi election rally (2014) | +59.7% | +33.5% | +26.2% |

| India NBFC crisis (2019) | -6.6% | +16.0% | -22.6% |

| COVID recovery (2020) | +17.7% | +15.7% | +2.0% |

| Recent bull run (2021-2023) | +152% cumulative | +63.5% cumulative | +88.5% |

The pattern is clear. India amplifies global risk-off events (2008). India can suffer from domestic crises that don't track global markets (2011, 2019). And when India's own cycle is positive, the strategy can significantly outperform (2014, 2021–2023).

Backtest Methodology

Full methodology documentation: backtests/METHODOLOGY.md

| Parameter | Choice |

|---|---|

| Universe | NSE, Market Cap > ₹20B INR |

| Signal | Stock P/E < 60% of sector median P/E, P/E 3–50, ROE > 8%, D/E < 2.0 |

| Portfolio | Top 30 by lowest P/E-to-sector ratio, equal weight |

| Rebalancing | Annual (January) |

| Cash rule | Hold cash if < 10 qualify |

| Benchmark | Sensex (^BSESN, price return) |

| Period | 2000–2024 (25 years), effective 2006–2024 |

| Data | Point-in-time (45-day lag on FY financial statements) |

| Transaction costs | 0.1% one-way (size-tiered by market cap) |

Limitations

Trails the local benchmark. Despite beating SPY (+2.32% excess), the strategy trails the Sensex by 1.45%. The Sensex itself returned 11.4% CAGR over 25 years, so a strategy at 9.96% is slightly below-market for India.

Extreme volatility. 35%+ annualized standard deviation. The Sharpe ratio of 0.099 is very low. Risk-adjusted returns are weak. If you size this the same as a US equity position, the portfolio swings are uncomfortable.

Severe max drawdown. -62.16% in 2008 is the strategy's worst year and its worst peak-to-trough decline. Investors who entered in 2007 and held through 2008 lost more than 60% of their capital before recovery.

Only 19 effective years. The 2000–2005 cash periods mean this backtest has fewer data points than it appears. There are 19 invested years, not 25.

India-specific crises. The 2019 NBFC crisis caused a -48.2% excess return gap vs SPY in a single year. Domestic Indian credit events, policy changes, and regulatory shocks aren't visible in global indicators. They can't be anticipated from a global macro perspective.

Currency risk. Portfolio returns are in INR. US investors holding Indian equities face INR/USD fluctuations. India has experienced periods of INR depreciation, which would reduce returns when converted to USD.

Down-capture of 78% vs Sensex. This is less protection than UK or Germany in the same study. India's high beta means losses can be severe even when the strategy holds fundamentally sound stocks.

Sector concentration. Without a sector cap, the January screen can cluster heavily in financials or industrials depending on the year. 2018–2019 exposure to Indian financials during the NBFC crisis is an example of this concentration risk materializing.

Conclusion

Sector-relative P/E mean reversion in India delivered 9.96% CAGR over 19 effective years. That beats SPY (+2.32% excess) but trails the Sensex (-1.45%). The strategy beat the index during specific periods (2007, 2009, 2012, 2014, 2016-2017, 2021-2023) but lagged during others (2006, 2008, 2011, 2013, 2018-2019).

The cost is extreme volatility, a -62% drawdown in 2008, and severe domestic risk that doesn't show up in global signals. The 2019 NBFC crisis is the clearest example: a domestic credit event that had nothing to do with global markets but hurt Indian value stocks.

India rewards this approach when its own economic cycle is favorable. When India is in a domestic slowdown or credit crisis, the strategy amplifies losses. The Sharpe of 0.099 reflects exactly that trade-off: moderate return after adjusting for the local benchmark, very high risk, rough path.

This isn't a replacement for a core India equity position. You'd be better off holding the Sensex (11.4% CAGR with lower drawdowns). The strategy makes sense only if you believe you can time entry/exit around India's domestic cycles, which is a different bet than the strategy itself.

Data: Ceta Research (FMP financial data warehouse). Returns in INR (local currency). Past performance does not guarantee future results. See full methodology at github.com/ceta-research/backtests.