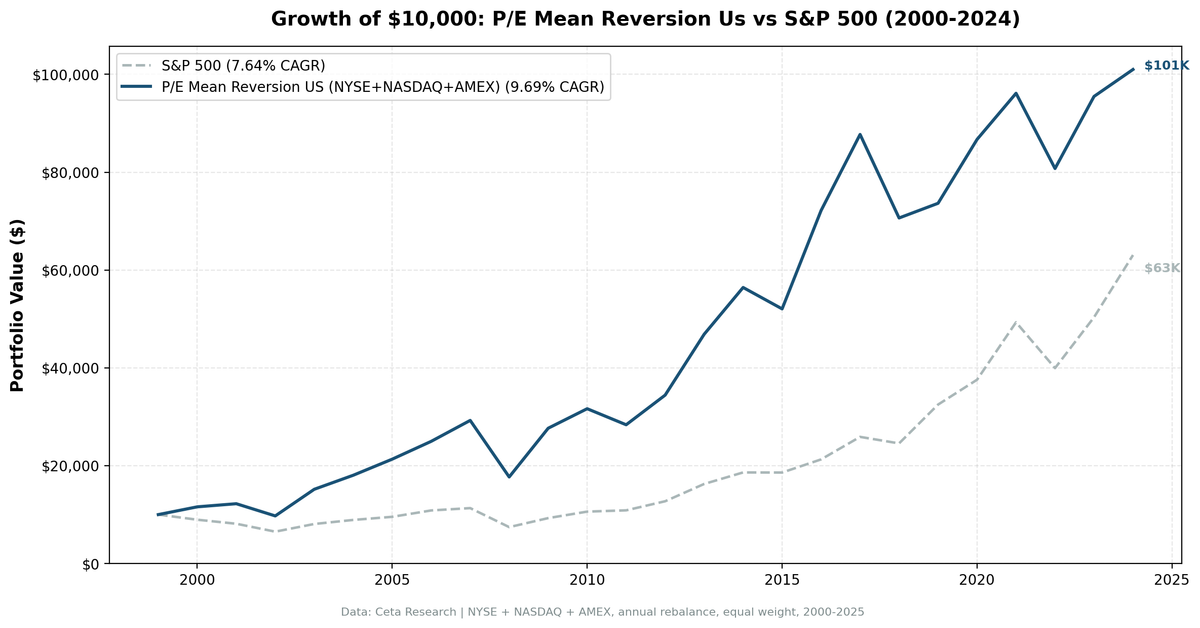

P/E Mean Reversion (Sector-Relative): 9.69% CAGR Over US Stock Data

We tested a sector-relative P/E mean reversion screen on 25 years of US stock data from NYSE, NASDAQ, and AMEX. The signal triggers when a quality stock's P/E ratio falls below 60% of its sector's current median, meaning it's trading at least 40% cheaper than its peers right now. The strategy returned 9.69% annually vs 7.64% for the S&P 500, with 2.05% excess return, zero cash periods, and consistent recovery after value selloffs.

Contents

- Method

- Why Sector-Relative P/E?

- The Screen

- P/E Mean Reversion Screen. US Stocks (SQL)

- What We Found

- 25 years. 2.05% annual alpha. Consistent value recovery.

- Year-by-year returns

- 2000-2007: the strategy's best stretch

- Crisis comparison

- 2016: post-election value rotation

- 2019, 2021, 2024: growth regime drag

- Sector-Relative vs Own-History Signals

- Geographic Pattern

- Backtest Methodology

- Limitations

- Conclusion

Method

- Data source: Ceta Research (FMP financial data warehouse)

- Universe: NYSE + NASDAQ + AMEX, market cap > $1B USD

- Period: 2000-2024 (25 years, 25 annual periods)

- Rebalancing: Annual (January), equal weight, top 30 by lowest P/E-to-sector ratio

- Benchmark: S&P 500 Total Return (SPY)

- Cash rule: Hold cash if fewer than 10 stocks qualify

Financial data sourced from financial_ratios_ttm for P/E and debt ratios, key_metrics_ttm for ROE and market cap, profile for sector classification. 45-day lag on all financial statements to prevent look-ahead bias.

Why Sector-Relative P/E?

An 8x P/E stock in Technology is probably cheap. An 8x stock in Utilities might be perfectly ordinary. Absolute P/E thresholds ignore this structural reality. Different sectors trade at different multiples for good reasons: growth rates, capital intensity, competitive dynamics, and interest rate sensitivity all push sector valuations apart.

Sector-relative P/E solves this by asking a different question: is this stock cheap relative to its own industry? Not cheap versus some universal threshold, and not cheap versus its own past, but cheap versus what similar companies trade at right now.

This is a cross-sectional signal. The sector median is computed fresh at each rebalance using all qualifying stocks in the universe. There's no historical P/E data required. If Technology stocks broadly reprice from 25x to 35x median P/E (a secular regime shift), the signal adapts. Stocks are still ranked relative to the new median.

Signal: P/E mean reversion (sector-relative) - P/E range: 3-50 (profitable, not speculative) - Stock P/E < 60% of sector median P/E (40%+ discount to peers) - Minimum 5 stocks in the sector to compute a reliable median

Quality filters:

| Criterion | Metric | Threshold |

|---|---|---|

| Profitable | Return on Equity | > 8% |

| Manageable debt | Debt-to-Equity | < 2.0 |

Size:

| Criterion | Metric | Threshold |

|---|---|---|

| Institutional grade | Market Cap | > $1B USD |

Stocks must pass all filters. The top 30 by lowest P/E-to-sector ratio are selected each year, equal weighted. No sector cap.

The Screen

P/E Mean Reversion Screen. US Stocks (SQL)

WITH universe AS (

SELECT k.symbol, p.companyName, p.exchange, p.sector,

fr.priceToEarningsRatioTTM AS pe_ttm, k.returnOnEquityTTM AS roe,

fr.debtToEquityRatioTTM AS de, k.marketCap

FROM key_metrics_ttm k

JOIN financial_ratios_ttm fr ON k.symbol = fr.symbol

JOIN profile p ON k.symbol = p.symbol

WHERE fr.priceToEarningsRatioTTM BETWEEN 3 AND 50

AND k.returnOnEquityTTM > 0.08

AND (fr.debtToEquityRatioTTM IS NULL OR (fr.debtToEquityRatioTTM >= 0 AND fr.debtToEquityRatioTTM < 2.0))

AND k.marketCap > 1000000000

AND p.sector IS NOT NULL

AND p.exchange IN ('NYSE', 'NASDAQ', 'AMEX')

),

sector_medians AS (

SELECT exchange, sector,

PERCENTILE_CONT(0.5) WITHIN GROUP (ORDER BY pe_ttm) AS median_pe,

COUNT(*) AS n_sector_stocks

FROM universe GROUP BY exchange, sector HAVING COUNT(*) >= 5

)

SELECT u.symbol, u.companyName, u.exchange, u.sector,

ROUND(u.pe_ttm, 2) AS pe_ttm, ROUND(sm.median_pe, 2) AS sector_median_pe,

ROUND(u.pe_ttm / sm.median_pe, 3) AS pe_ratio_to_sector,

ROUND((1 - u.pe_ttm / sm.median_pe) * 100, 1) AS discount_pct,

ROUND(u.roe * 100, 1) AS roe_pct, ROUND(u.de, 2) AS debt_to_equity,

ROUND(u.marketCap / 1e9, 2) AS mktcap_b

FROM universe u JOIN sector_medians sm ON u.exchange = sm.exchange AND u.sector = sm.sector

WHERE u.pe_ttm / sm.median_pe < 0.60

ORDER BY u.pe_ttm / sm.median_pe ASC LIMIT 30

Run this query on Ceta Research

What We Found

25 years. 2.05% annual alpha. Consistent value recovery.

| Metric | P/E Mean Reversion (US) | S&P 500 |

|---|---|---|

| CAGR | 9.69% | 7.64% |

| Total Return | 909.98% | 530.71% |

| Sharpe Ratio | 0.341 | 0.322 |

| Sortino Ratio | 0.673 | 0.556 |

| Max Drawdown | -39.53% | -34.90% |

| Up Capture | 117.02% | 100% |

| Down Capture | 83.33% | 100% |

| Win Rate vs SPY | 60% | - |

| Avg Stocks per Year | 21.5 | - |

| Cash Periods | 0 of 25 | - |

$10,000 grew to $100,998 vs $63,071 for the S&P 500. The Sharpe ratio improved from 0.322 to 0.341, and the Sortino ratio from 0.556 to 0.673. The down-capture of 83% is weaker than a typical value strategy, but 25 consecutive invested periods and 60% win rate against SPY are a solid foundation.

The asymmetry here is different from longitudinal P/E compression. Up-capture is 117%, meaning this screen participates strongly in bull markets. Down-capture at 83% means it doesn't shed much in downturns but also doesn't fully protect like defensive screens.

Zero cash periods means the sector-relative signal always finds eligible stocks. At any point in the cycle, some sectors are compressed relative to their peers and some stocks within them are trading at deep discounts.

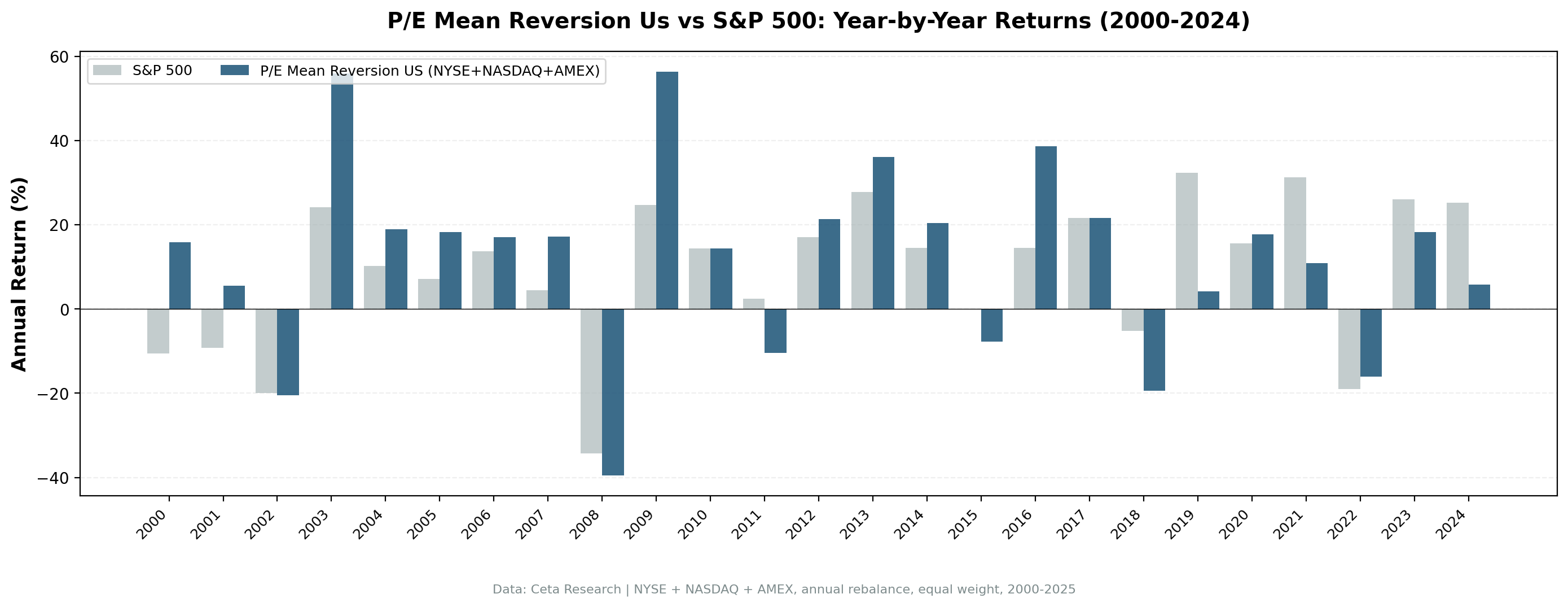

Year-by-year returns

| Year | P/E Mean Reversion | S&P 500 | Excess |

|---|---|---|---|

| 2000 | +15.9% | -10.5% | +26.4% |

| 2001 | +5.5% | -9.2% | +14.7% |

| 2002 | -20.4% | -19.9% | -0.5% |

| 2003 | +56.0% | +24.1% | +31.9% |

| 2004 | +18.9% | +10.2% | +8.7% |

| 2005 | +18.2% | +7.2% | +11.1% |

| 2006 | +17.1% | +13.7% | +3.4% |

| 2007 | +17.1% | +4.4% | +12.7% |

| 2008 | -39.5% | -34.3% | -5.2% |

| 2009 | +56.3% | +24.7% | +31.6% |

| 2010 | +14.4% | +14.3% | +0.1% |

| 2011 | -10.4% | +2.5% | -12.8% |

| 2012 | +21.4% | +17.1% | +4.3% |

| 2013 | +36.1% | +27.8% | +8.3% |

| 2014 | +20.4% | +14.5% | +5.9% |

| 2015 | -7.8% | -0.1% | -7.6% |

| 2016 | +38.6% | +14.4% | +24.2% |

| 2017 | +21.6% | +21.6% | -0.1% |

| 2018 | -19.5% | -5.2% | -14.3% |

| 2019 | +4.2% | +32.3% | -28.1% |

| 2020 | +17.7% | +15.6% | +2.1% |

| 2021 | +10.9% | +31.3% | -20.4% |

| 2022 | -16.0% | -19.0% | +3.0% |

| 2023 | +18.2% | +26.0% | -7.8% |

| 2024 | +5.8% | +25.3% | -19.5% |

2000-2007: the strategy's best stretch

The period from 2000 to 2007 generated the bulk of the long-run alpha. In 2000 and 2001, the screen avoided overvalued tech while owning sector laggards with depressed relative multiples. In the recovery from 2003 onward, those sector discounts closed and the portfolio captured the full rally.

The two standout years in this period are 2003 (+56.0% vs +24.1%) and 2009 (+56.3% vs +24.7%). Both are classic value recovery years. After a broad market selloff, the most discounted stocks in each sector bounced back hardest as investors moved down the quality-valuation stack.

Crisis comparison

| Event | P/E Mean Reversion | S&P 500 | Gap |

|---|---|---|---|

| Dot-com bust (2000-2002) | +0.1% cumulative | -35.1% | +35.2% |

| Financial crisis (2008) | -39.5% | -34.3% | -5.2% |

| COVID (2020) | +17.7% | +15.6% | +2.1% |

| 2022 bear market | -16.0% | -19.0% | +3.0% |

2008 is the weak point. When a crisis is sector-wide and correlated across all industries, sector-relative signals stop helping. If the entire Financial sector collapses together, a Financial stock that was trading at 40% below its sector median is still a Financial stock in a systemic crisis. The discount narrows but the absolute loss is severe. The -39.5% in 2008 was nearly as bad as SPY's -34.3%.

The dot-com contrast is sharp. From 2000 to 2002, the screen held up because the crash was sector-specific. Technology multiples collapsed, but the signal had already pointed away from the most inflated names toward the sector laggards trading at deep discounts. Stocks with P/E at 60% of their sector peers weren't the ones priced at 100x earnings.

2016: post-election value rotation

2016 produced the strategy's largest excess return outside of the 2003 and 2009 recoveries: +38.6% vs +14.4% for SPY. The post-election rotation into cyclicals and financials aligned perfectly with the sector-relative signal. Stocks that had been depressed relative to peers in Energy, Materials, and Financials captured a sharp rerating.

2019, 2021, 2024: growth regime drag

Three years of painful underperformance: 2019 (-28.1% excess), 2021 (-20.4% excess), 2024 (-19.5% excess). These years share a common feature: market returns were driven by a narrow group of high-multiple technology and growth stocks that the sector-relative screen structurally avoids.

A stock trading at 60x P/E doesn't qualify. Its sector peers at 80x don't either. The signal never touches those names. When those names dominate returns, the screen lags badly. This is the standard weakness of any value-oriented approach, and sector-relative P/E is no exception.

The quality filters (ROE > 8%, D/E < 2) don't prevent this underperformance. They screen for stable businesses, not for growth momentum.

Sector-Relative vs Own-History Signals

The P/E compression approach (stock vs its own 5-year average) and this sector-relative approach are measuring different things. Both are mean reversion signals, but they operate on different axes.

| Dimension | P/E Compression | P/E Mean Reversion (Sector-Relative) |

|---|---|---|

| Baseline | Stock's own history | Sector peers today |

| Data needed | 3-5 years of historical P/E | Current cross-section only |

| Adapts to regime shifts | Slowly (5-year average lags) | Immediately (median recalculated each year) |

| Catches | Stocks that de-rated vs themselves | Stocks cheap relative to current peer pricing |

| Miss risk | Stocks in permanently re-rated sectors | Entire sectors that are structurally cheap |

Neither is strictly better. A stock could qualify under both signals (compressed vs own history and vs sector peers) or under only one. A sector that has broadly re-rated upward over five years produces stocks that look expensive vs their own history but cheap relative to peers who moved the same way. The sector-relative signal catches those; the longitudinal signal misses them.

The cross-sectional approach also sidesteps a practical limitation: some companies lack enough P/E history for a reliable 5-year average. Sector-relative works for any stock with a current P/E and at least five sector peers.

Geographic Pattern

This strategy works in the US, UK, and Germany. It fails in most Asian markets.

In Japan, Korea, Taiwan, and Hong Kong, stocks that screen as cheap relative to sector peers tend to stay cheap. The mean reversion assumption breaks down. Corporate governance, capital allocation practices, and entrenched cross-shareholding structures mean that value discounts don't close on Western timelines, if they close at all.

The US result here (2.05% excess) is typical for the Western markets where this approach works. UK and Germany both show similar or stronger excess returns with reasonable cash periods. The comparison blog covers all 13 exchanges.

Backtest Methodology

Full methodology documentation: backtests/METHODOLOGY.md

| Parameter | Choice |

|---|---|

| Universe | NYSE + NASDAQ + AMEX, Market Cap > $1B USD |

| Signal | Stock P/E < 60% of sector median, P/E 3-50, ROE > 8%, D/E < 2.0 |

| Portfolio | Top 30 by lowest P/E-to-sector ratio, equal weight |

| Rebalancing | Annual (January) |

| Cash rule | Hold cash if < 10 qualify |

| Benchmark | S&P 500 Total Return (SPY) |

| Period | 2000-2024 (25 years) |

| Data | Point-in-time (45-day lag on FY financial statements) |

| Transaction costs | 0.1% one-way (size-tiered by market cap) |

Limitations

Down capture of 83%. This screen doesn't offer strong downside protection. The 83% down-capture means when SPY loses 10%, this portfolio loses about 8.3% on average. Other value screens with stricter quality filters show 70% or better. The sector-relative signal doesn't inherently select for defensive characteristics.

2008 full participation. In systemically correlated selloffs, sector-relative positioning doesn't help. The -39.5% in 2008 was nearly as bad as the index. When every sector drops together, being the cheapest stock in a sector doesn't cushion the fall.

Severe underperformance in growth regimes. 2019, 2021, and 2024 each saw 20%+ excess return gaps. An investor who held this strategy through 2019-2024 would have experienced two separate years of severe lag inside a six-year stretch. That requires patience.

Smaller portfolio. Averaging 21.5 stocks per year is reasonable but not highly diversified. Sector concentration can occur in years when one industry has an unusually large number of discounted names. There's no sector cap in this implementation.

Sector median quality. The sector median is calculated from the same filtered universe (profitable, quality-filtered stocks). If a sector has fewer than five qualifying stocks, it's excluded from the signal that year. Thin sectors drop out.

Survivorship bias. Exchange membership uses current profiles, not historical. This is a standard limitation in this backtest approach.

Conclusion

Sector-relative P/E mean reversion delivered 2.05% annual alpha over 25 years of US data, growing $10,000 to $100,998 vs $63,071 for the S&P 500. The 60% win rate against SPY and zero cash periods show it's a consistent signal, not a one-era phenomenon.

The strategy thrives in value recovery years and post-crisis rebounds. It struggles in growth-dominated markets where narrow, high-multiple leadership drives index returns. That's the structural trade-off of any sector-discounting approach.

The key advantage over absolute P/E thresholds: the signal adapts automatically to sector re-ratings and regime shifts. There's no need to decide what constitutes "cheap" for Technology vs Utilities vs Healthcare. The market's own current pricing defines the benchmark, and the screen finds the names trading far below it with quality fundamentals intact.

For investors already holding market exposure, this screen identifies names likely to mean-revert toward their sector's valuation, with the quality filters ensuring the cheapness isn't purely justified by deteriorating fundamentals.

Part of a Series: Global | UK | India | Germany

Run It Yourself

Explore the data behind this analysis on Ceta Research. Query our financial data warehouse with SQL, build custom screens, and run your own backtests across 70,000+ stocks on 20 exchanges.

Data: Ceta Research (FMP financial data warehouse). Past performance doesn't guarantee future results. See full methodology at github.com/ceta-research/backtests.