R&D Efficiency Across 10 Exchanges: UK Beats FTSE by +7.22%, India Trails Sensex

We reran the R&D efficiency screen across 10 exchanges with local benchmarks. UK beats FTSE 100 (price return) by +7.22% annually — the strongest result globally. India, previously the standout vs SPY, now underperforms the Sensex by 4.65pp. Local benchmarks change everything. Pharma-heavy...

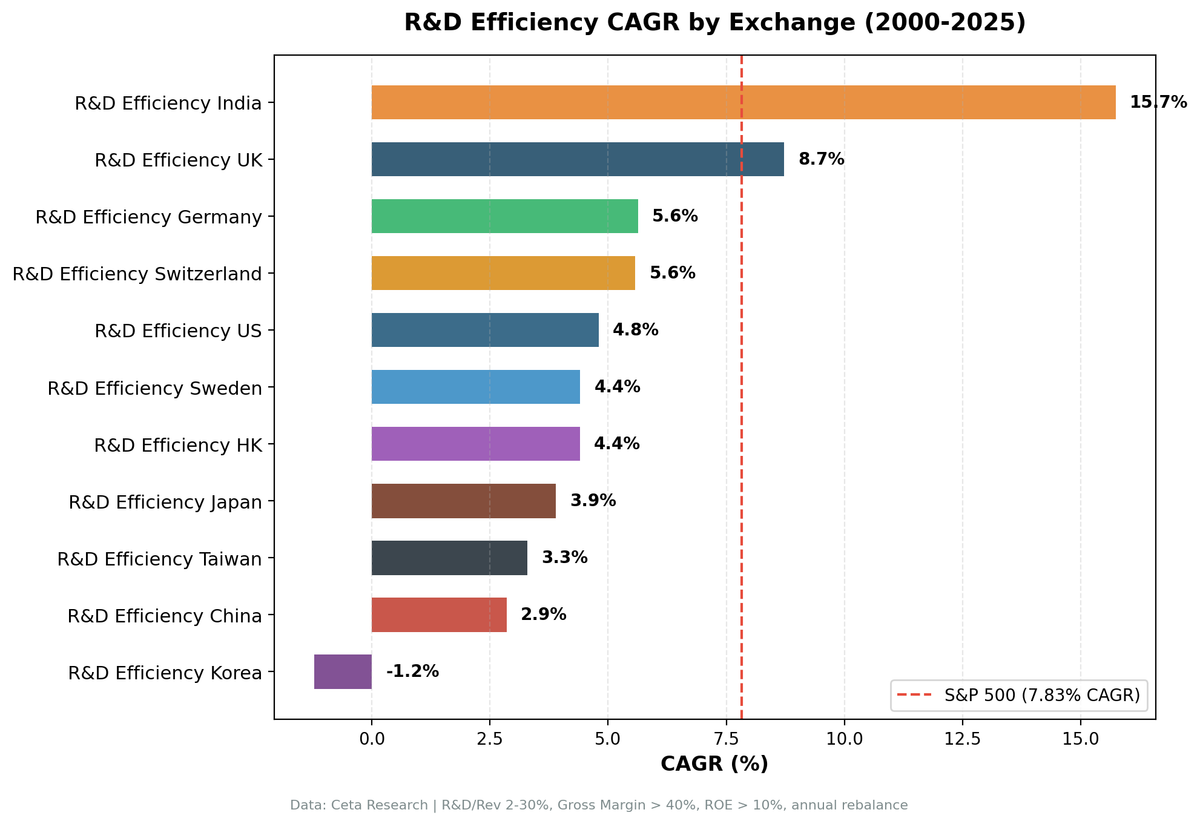

We ran the same R&D efficiency screen, gross profit per R&D dollar, filtered by R&D/Revenue 2-30%, gross margin >40%, ROE >10%, across 10 exchanges over 25 years. Previous versions of this comparison used the S&P 500 (SPY) as a uniform benchmark for all exchanges. This version uses each exchange's local index.

Contents

- Results With Local Benchmarks

- What Changed From the Previous Version

- Why Sector Composition Determines the Result

- The UK Story: FTSE 100's 25-Year Failure

- Japan: High-Quality Screen, Low Universe Coverage

- Switzerland: Notable Candidate

- The Screen

- Limitations

- Takeaway

Using SPY as the global benchmark masked two important corrections: it made India look like the standout winner (its absolute returns beat SPY), but India's own market (Sensex) returned 12.06% CAGR over this period, and the NSE-only strategy returned only 7.41%. Meanwhile, the UK (LSE) looked like it barely beat SPY, but the FTSE 100 returned only 1.23% CAGR (price-only), making the UK screen's 8.45% CAGR a significant outperformer vs its local market.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Results With Local Benchmarks

| Exchange | CAGR | Local Benchmark | Bench CAGR | Excess | Sharpe | Max DD | Cash% |

|---|---|---|---|---|---|---|---|

| UK (LSE) | 8.45% | FTSE 100 (price) | 1.23% | +7.22% | 0.320 | -17.26% | 4% |

| Switzerland (SIX) | 5.35% | SMI (price) | 1.74% | +3.61% | 0.329 | -25.81% | 0% |

| HK (HKSE) | 4.94% | Hang Seng | 1.64% | +3.29% | 0.091 | -55.82% | 16% |

| China (SHH/SHZ) | 3.35% | SSE Composite | 2.43% | +0.92% | 0.046 | -40.08% | 32% |

| Sweden (STO) | 4.40% | OMX Stockholm 30 | 2.55% | +1.85% | 0.208 | -12.57% | 68% |

| Germany (XETRA) | 5.60% | DAX | 5.04% | +0.56% | 0.204 | -42.37% | 0% |

| Japan (JPX) | 3.69% | Nikkei 225 | 3.31% | +0.38% | 0.299 | -18.11% | 52% |

| Taiwan (TAI) | 3.56% | TAIEX | 4.09% | -0.52% | 0.132 | -41.86% | 36% |

| US (NYSE/NASDAQ/AMEX) | 4.90% | S&P 500 | 7.85% | -2.95% | 0.164 | -33.74% | 0% |

| India (NSE) | 7.41% | Sensex | 12.06% | -4.65% | 0.039 | -13.70% | 56% |

| Korea (KSC) | -1.53% | KOSPI | 5.35% | -6.89% | -0.485 | -43.32% | 80% |

Period: 2000–2024. Local benchmark for each exchange.

Benchmark note: The FTSE 100 (^FTSE), SMI (^SSMI), and OMX Stockholm 30 (^OMXS30) are price-return indices, dividends excluded. The portfolio uses dividend-adjusted prices (adjClose). This creates a comparison bias that inflates portfolio excess by approximately the index's dividend yield (2-4% annually for FTSE and SMI). True excess vs total-return benchmarks for UK and Switzerland is likely 3-4pp and 1-2pp respectively.

Sorted by excess return vs local benchmark. Three markets beat their local index meaningfully (UK, Switzerland, HK), four are roughly flat or slightly positive (China, Sweden, Germany, Japan), and three underperform significantly (Taiwan, US, India, Korea).

What Changed From the Previous Version

The previous comparison (using SPY as uniform benchmark) showed: - India: +7.91% excess (highest of any exchange) - UK: +0.88% excess - US: -3.04% excess

With local benchmarks: - India: -4.65% excess (underperforms Sensex) - UK: +7.22% excess (strongest result) - US: -2.95% excess (minor change, SPY is the correct benchmark for US anyway)

The India reversal reflects two corrections: 1. Benchmark: Sensex (12.06% CAGR) vs SPY (7.85% CAGR). India's market compounded much faster than the US market over this period. 2. Universe: NSE-only vs BSE+NSE. Removing BSE eliminated dual-listing duplication and increased the cash rate from 24% to 56%.

The UK improvement reflects one correction: the FTSE 100 had a very poor 25-year run in price-return terms (1.23% CAGR). The UK market's returns came largely from dividends, not price appreciation, and the price-only index barely moved in 25 years.

Why Sector Composition Determines the Result

The gross margin filter (>40%) is the most discriminating constraint in the screen. That single filter shapes which sectors can appear in the portfolio.

Sectors that pass the 40% gross margin threshold: pharmaceuticals, software, financial data services, specialty chemicals, luxury goods. Sectors that fail: semiconductors (20-50% gross margins, highly variable), hardware (20-40%), manufacturing (10-30%), energy (variable).

UK and Switzerland outperform because their qualifying universes are concentrated in sectors with genuinely defensive demand. UK: AstraZeneca, GSK, RELX, Experian. Switzerland: Roche, Novartis, Straumann, Lonza. Both markets have large-cap pharma as the dominant R&D spender in the qualifying cohort, and pharma revenue doesn't cycle with GDP.

India underperforms despite a favorable sector mix. Indian pharma (Sun Pharma, Dr. Reddy's, Cipla) and IT services (TCS, Infosys) have exactly the right economics for this screen. The problem is universe thinness, on NSE-only, fewer than 10 companies pass all filters simultaneously in most years before 2014. When the screen does invest (2014-2024), the active-period record is volatile, with spectacular years (2014, 2023) offset by sustained underperformance (2016-2018, 2021).

US underperforms because the S&P 500 from 2013 onward was dominated by mega-cap tech companies that either fail the 30% R&D cap or rank mid-tier on efficiency. The strategy finds the right kind of company; the index moved away from those companies.

Korea fails completely. Samsung, SK Hynix, LG, semiconductors and consumer electronics. Gross margins in the 20-35% range. The 80% cash rate means the screen rarely finds qualifying Korean companies.

The UK Story: FTSE 100's 25-Year Failure

The FTSE 100's 1.23% CAGR over 25 years is a well-documented underperformance. The index is heavily weighted toward energy, mining, banks, and consumer staples, sectors that underperformed global equities from 2000-2024. The UK market's returns came from dividends, not capital appreciation.

The R&D efficiency screen's pharma and software focus naturally avoided the FTSE's weakest sectors and captured its strongest ones. AstraZeneca, the screen's probable top holding in many years, returned dramatically more than the FTSE 100 index. RELX and Experian outperformed similarly.

This creates a valid but caveat-laden conclusion: the strategy genuinely outperformed what UK investors actually experienced in their portfolios (FTSE 100 price underperformance). But comparing to total-return FTSE (including dividends) would show a smaller excess of roughly 3-4pp annually.

Japan: High-Quality Screen, Low Universe Coverage

Japan's 52% cash rate is the most interesting result in the dataset. Japan has many R&D-intensive companies, but most of them are in sectors that fail the gross margin filter: Toyota (17% gross margin), Panasonic (20%), Sony (28%). The companies that do qualify, Shiseido, some specialty pharma, certain software companies, are few enough that the screen frequently can't fill 10 positions.

When invested, Japan's Sharpe ratio (0.299) and max drawdown (-18.11%) are actually quite good. The signal finds quality. The problem is frequency of deployment.

A lower gross margin threshold (say, 35%) would expand the Japanese qualifying universe significantly but would also include lower-quality businesses. The 40% threshold is the right signal for this factor; Japan just doesn't have enough companies that pass.

Switzerland: Notable Candidate

Switzerland deserves mention. 5.35% CAGR, Sharpe 0.329, MaxDD -25.81%, +3.61% excess vs SMI price return, 0% cash periods. Roche and Novartis are among the world's largest pharma companies and both list on the SIX. They routinely pass the R&D efficiency screen.

The SMI price return (1.74% CAGR) has the same issue as the FTSE 100, it's price-only, and Swiss large-caps are known for dividends. Adjusting for dividends (roughly 3% annually for Swiss blue chips), the true excess vs total-return SMI is closer to 1-2pp. Still positive, but less dramatic than the raw number suggests.

Switzerland may be worth a dedicated backtest analysis for a future session.

The Screen

Run this globally to see today's top R&D efficiency stocks across all exchanges:

WITH inc AS (

SELECT symbol, revenue, grossProfit, researchAndDevelopmentExpenses,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY dateEpoch DESC) AS rn

FROM income_statement

WHERE period = 'FY'

AND revenue > 0

AND grossProfit > 0

AND researchAndDevelopmentExpenses > 0

)

SELECT

inc.symbol,

p.companyName,

p.exchange,

p.sector,

ROUND(inc.researchAndDevelopmentExpenses / inc.revenue * 100, 1) AS rd_ratio_pct,

ROUND(inc.grossProfit / inc.revenue * 100, 1) AS gross_margin_pct,

ROUND(inc.grossProfit / inc.researchAndDevelopmentExpenses, 2) AS rd_efficiency,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM inc

JOIN profile p ON inc.symbol = p.symbol

JOIN key_metrics_ttm k ON inc.symbol = k.symbol

WHERE inc.rn = 1

AND inc.researchAndDevelopmentExpenses / inc.revenue > 0.02

AND inc.researchAndDevelopmentExpenses / inc.revenue < 0.30

AND inc.grossProfit / inc.revenue > 0.40

AND k.returnOnEquityTTM > 0.10

AND k.marketCap > 1000000000

ORDER BY rd_efficiency DESC

LIMIT 30

Run this query on Ceta Research

Limitations

Price-return vs total-return benchmark mismatch. FTSE 100, SMI, and OMX Stockholm 30 are price-return indices. Portfolio stocks use dividend-adjusted prices. This inflates the apparent excess for UK, Switzerland, and Sweden by approximately their dividend yields. True excess vs total-return local indices is lower.

Currency effects are embedded. Returns for each exchange are in the local currency. The comparisons across exchanges absorb currency return components that may be positive or negative depending on the period. INR returns look different in USD terms after 3-4% annual depreciation.

India universe correction. The previous version used BSE+NSE (producing 15.74% CAGR vs SPY, +7.91% excess). This version uses NSE-only and Sensex as the benchmark. NSE-only has a thinner qualifying universe and more cash periods. The Sensex is the correct local benchmark. Both corrections reduce the apparent India result.

Data coverage varies by exchange. FMP's R&D data coverage varies by market and improved in some markets around 2025-2026. Earlier backtest years for Japan and LSE may have thinner stock universes, which could affect historical cash rates and results.

Cash periods are mechanically determined. High cash rates (India 56%, Sweden 68%, Japan 52%, Korea 80%) reflect genuine universe thinness for this screen's specific filter combination. They reduce the ability to draw conclusions about the signal's predictive power vs random noise.

Takeaway

With local benchmarks, the UK is the standout result: +7.22% annual excess vs FTSE 100 price return, -17.26% max drawdown, 76% win rate. Even adjusting for the price-only benchmark issue (true excess vs total-return FTSE likely 3-4pp), it's the strongest and most consistent result across all 10 markets.

India's previous top ranking was largely an artifact of comparing INR returns to USD (SPY) and using BSE+NSE instead of NSE-only. Against the Sensex on NSE-only data, the strategy underperforms by 4.65pp annually. The screen does find India's best R&D-efficient companies, and the active-period results in certain years (2014, 2023) are extraordinary. But systematic deployment against the Sensex doesn't generate consistent alpha.

The sector story holds: this screen works where the qualifying universe is naturally concentrated in pharma and software with defensive demand. UK passes that test. India's NSE has the right sector composition but not enough qualifying companies to stay consistently invested.

Full backtest code: github.com/ceta-research/backtests

Data: Ceta Research (FMP financial data warehouse). Returns are in local currencies. S&P 500 benchmark is in USD. FTSE 100, SMI, OMX S30 are price-return indices, true excess vs total-return versions would be lower. Past performance does not guarantee future results.