R&D Efficiency Backtest (US): 4.90% CAGR, Two Regimes, One Regime Shift

From 2000 to 2012, buying stocks with the highest gross profit per R&D dollar beat the S&P 500 consistently. Then mega-cap tech took over, and the strategy spent the next twelve years giving money back. 25-year backtest, full data, SQL included.

From 2000 to 2012, buying stocks with the highest gross profit per R&D dollar beat the S&P 500 consistently. Dot-com crash: the strategy held. GFC: it held again. Then the market structure changed, mega-cap tech took over, and the strategy spent the next twelve years giving money back.

Contents

- Method

- What We Found

- Two regimes, one backtest

- The regime shift

- Why mega-cap tech kills this screen

- Overall performance metrics

- The Screen

- Annual Performance

- Limitations

- Takeaway

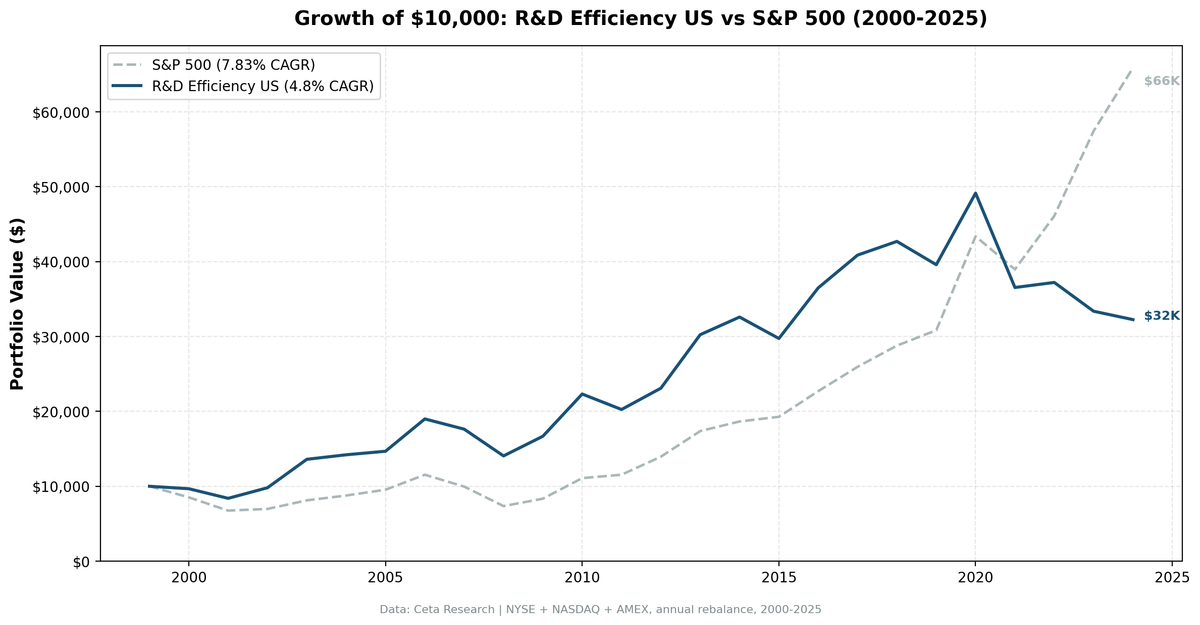

This is the story of a signal that has a real economic rationale, works in the right market environment, and fails in a specific way that's entirely explainable. The 25-year CAGR is 4.90% vs 7.85% for SPY. But that headline buries the more interesting finding: for the first thirteen years, this was alpha. For the last twelve, it wasn't.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: NYSE, NASDAQ, AMEX, market cap above $1B USD Period: 2000–2024 (25 annual rebalance periods) Execution: Next-day close (MOC, signal from prior close, entry at following close) Rebalancing: Annual (July), equal weight top 30 by R&D efficiency Benchmark: S&P 500 Total Return (SPY) Cash rule: Hold cash if fewer than 10 stocks qualify

Filters:

| Criterion | Threshold | Rationale |

|---|---|---|

| R&D / Revenue | 2–30% | Real R&D investment, not negligible or excessive |

| Gross Margin | > 40% | Excludes hardware, manufacturing, commodity companies |

| ROE | > 10% | Quality floor |

| Ranking signal | Gross Profit / R&D Expenses | Higher = more output per R&D dollar |

Transaction costs: size-tiered (0.1% for market cap > $10B, 0.3% for $2–10B, 0.5% below $2B), one-way. Historical data with 45-day point-in-time lag to prevent look-ahead bias. Full methodology: backtests/METHODOLOGY.md

What We Found

Two regimes, one backtest

The 25-year chart shows a strategy that tracked with SPY through 2012, then diverged sharply downward. That split point is not arbitrary. 2013 is when FAANG companies began dominating S&P 500 returns in a way they hadn't before. Meta went public in 2012. Amazon's market cap crossed $100B. Google's revenue growth reaccelerated. The composition of what drove SPY returns changed permanently.

Here's what that looked like in the first regime (2000–2012):

| Year | Portfolio | S&P 500 | Excess |

|---|---|---|---|

| 2000 | -3.3% | -14.8% | +11.5% |

| 2001 | -15.9% | -22.4% | +6.6% |

| 2002 | +21.4% | +6.9% | +14.5% |

| 2003 | +33.6% | +14.9% | +18.6% |

| 2004 | +5.8% | +8.9% | -3.1% |

| 2005 | +3.1% | +8.0% | -4.8% |

| 2006 | +29.4% | +20.9% | +8.4% |

| 2007 | -8.9% | -15.2% | +6.3% |

| 2008 | -20.7% | -26.9% | +6.2% |

| 2009 | +22.1% | +16.0% | +6.1% |

| 2010 | +34.4% | +33.5% | +0.8% |

| 2011 | -9.2% | +4.2% | -13.4% |

| 2012 | +13.6% | +20.7% | -7.1% |

From 2000 to 2010, the strategy beat SPY in nine out of eleven years. The two losses (2004, 2005) were modest. The wins in 2002 (+21.4% vs +6.9%), 2003 (+33.6% vs +14.9%), and 2006 (+29.4% vs +20.9%) were large.

The economic logic held: companies that extract maximum gross profit per R&D dollar tend to be in pharmaceuticals, software, and specialty chemicals, businesses where R&D translates directly to product pricing power. In the 2000s, that cohort competed against each other. The winners were genuinely better businesses.

The regime shift

Post-2012 returns tell a different story:

| Year | Portfolio | S&P 500 | Excess |

|---|---|---|---|

| 2013 | +32.6% | +24.7% | +7.8% |

| 2014 | +7.6% | +7.2% | +0.5% |

| 2015 | -9.5% | +2.7% | -12.2% |

| 2016 | +24.6% | +18.6% | +6.0% |

| 2017 | +12.0% | +14.3% | -2.4% |

| 2018 | +5.1% | +11.2% | -6.1% |

| 2019 | -6.9% | +7.4% | -14.3% |

| 2020 | +24.3% | +41.0% | -16.7% |

| 2021 | -25.3% | -10.7% | -14.6% |

| 2022 | +1.5% | +18.1% | -16.6% |

| 2023 | -10.1% | +25.4% | -35.6% |

| 2024 | -2.8% | +14.4% | -17.2% |

The pattern flips. 2019 through 2024 is particularly stark. Six consecutive years where the strategy trails SPY, often by double digits. 2023 alone: portfolio -10.1%, SPY +25.4%.

Why mega-cap tech kills this screen

The R&D efficiency filter has a structural blind spot for the companies that dominated market returns from 2013 onward.

Google (Alphabet) spends roughly 15% of revenue on R&D, within the 2–30% filter range, but its gross margin has historically been 55-60%, which passes the 40% threshold. However, its R&D spending as a percentage of gross profit is high, meaning it doesn't rank at the top of the efficiency screen. Amazon's AWS segment would pass the gross margin filter, but Amazon's consolidated gross margin fluctuates, retail pulls it down.

Meta and Apple are in and out of the filter depending on the year. When they're in, they often rank mid-tier on gross profit per R&D dollar because their absolute R&D spending is enormous.

The real issue: the 30% R&D cap excludes companies during their highest-growth phases. Biotechs and early-stage platforms that spend 40-60% of revenue on R&D, the companies generating the biggest returns, never enter the screen. The filter is designed to find companies with established R&D productivity, not companies building future productivity. That distinction costs alpha in a market where growth at scale commanded ever-higher valuations.

Overall performance metrics

| Metric | Portfolio | S&P 500 |

|---|---|---|

| CAGR (2000–2024) | 4.90% | 7.85% |

| Total return | 231% | ~562% |

| Max drawdown | -33.74% | -38.01% |

| Avg stocks held | 25.2 | , |

| Cash periods | 0% | , |

| Sharpe ratio | 0.164 | ~0.35 |

$10,000 invested in 2000 grew to $33,100 in the portfolio vs approximately $66,200 in SPY.

The max drawdown of -33.74% is better than SPY's -38.01%, which reflects the quality filter's function. But the risk-adjusted returns (Sharpe 0.164) are poor because the CAGR doesn't compensate for the volatility incurred.

The Screen

Run this screen on the current universe to see today's top R&D efficiency stocks on US exchanges:

WITH inc AS (

SELECT symbol, revenue, grossProfit, researchAndDevelopmentExpenses,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY dateEpoch DESC) AS rn

FROM income_statement

WHERE period = 'FY'

AND revenue > 0

AND grossProfit > 0

AND researchAndDevelopmentExpenses > 0

)

SELECT

inc.symbol,

p.companyName,

p.exchange,

p.sector,

ROUND(inc.researchAndDevelopmentExpenses / inc.revenue * 100, 1) AS rd_ratio_pct,

ROUND(inc.grossProfit / inc.revenue * 100, 1) AS gross_margin_pct,

ROUND(inc.grossProfit / inc.researchAndDevelopmentExpenses, 2) AS rd_efficiency,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM inc

JOIN profile p ON inc.symbol = p.symbol

JOIN key_metrics_ttm k ON inc.symbol = k.symbol

WHERE inc.rn = 1

AND inc.researchAndDevelopmentExpenses / inc.revenue > 0.02

AND inc.researchAndDevelopmentExpenses / inc.revenue < 0.30

AND inc.grossProfit / inc.revenue > 0.40

AND k.returnOnEquityTTM > 0.10

AND k.marketCap > 1000000000

AND p.exchange IN ('NYSE', 'NASDAQ', 'AMEX')

ORDER BY rd_efficiency DESC

LIMIT 30

Run this query on Ceta Research

Annual Performance

Full 25-year annual returns are in the tables above. The summary pattern: the strategy beat SPY in 12 out of 25 years. It won the early period decisively and lost the post-2013 period almost as decisively. The 2021 year (-25.3%) is an outlier, that was a mean-reversion year within the portfolio's own picks, not a broad market decline (SPY that year was -10.7%, itself a weaker year).

2022 shows the strategy's occasional resilience: +1.5% when SPY returned +18.1%. Note: the backtest rebalances annually in July, so "2022" covers July 2022 to July 2023. SPY rising 18.1% over that window makes sense, July 2022 was near the market trough after the 2022 drawdown.

Limitations

The regime issue is real. Post-2013 US market returns concentrated in mega-cap tech. Any factor strategy that doesn't own that cohort will underperform SPY. This isn't unique to R&D efficiency, value, momentum, and most quality screens have had the same problem in the US since roughly 2016.

The 30% R&D cap is a deliberate constraint. It filters out companies in high R&D intensity phases (biotech, growth-stage software). Those exclusions hurt US performance because many of the best-returning US stocks in the past decade were high-R&D-intensity names.

Look-ahead bias is mitigated but not eliminated. The 45-day point-in-time lag prevents use of financial data before it was publicly reported. But the survivorship bias from sector classification in the current profile table is partially present.

Annual rebalancing is coarse. R&D efficiency is a slow-moving signal. Companies don't typically change their R&D ratios quarter to quarter. Annual rebalancing is appropriate for this signal, but it misses intra-year deterioration.

Cash rule is conservative. If fewer than 10 stocks qualify, the strategy holds cash. For the US, this never triggered (0% cash periods). The universe is large enough.

Takeaway

R&D efficiency worked in the US before mega-cap tech dominated the market. The economic logic is sound: companies extracting maximum gross profit from their R&D spending have genuine competitive advantages. The problem is structural, not fundamental. The US market from 2013 onward rewarded a different kind of company than the one this screen finds.

Two questions worth discussing: Would adding a market-cap ceiling (to exclude mega-caps from SPY but not from the portfolio) change the result? And does R&D efficiency work better in markets where tech isn't also the dominant sector weight?

The India and UK results below suggest the answer to the second question is yes.

Full backtest code: github.com/ceta-research/backtests

Data: Ceta Research (FMP financial data warehouse). Returns are in USD. Past performance does not guarantee future results.