Revenue Acceleration in Canada: +0.29% over the S&P 500. The Real Story is Downside.

Canada is the only market where revenue acceleration outperformed in our global study. The margin is thin (+0.29%), but the down capture of 44% tells the real story.

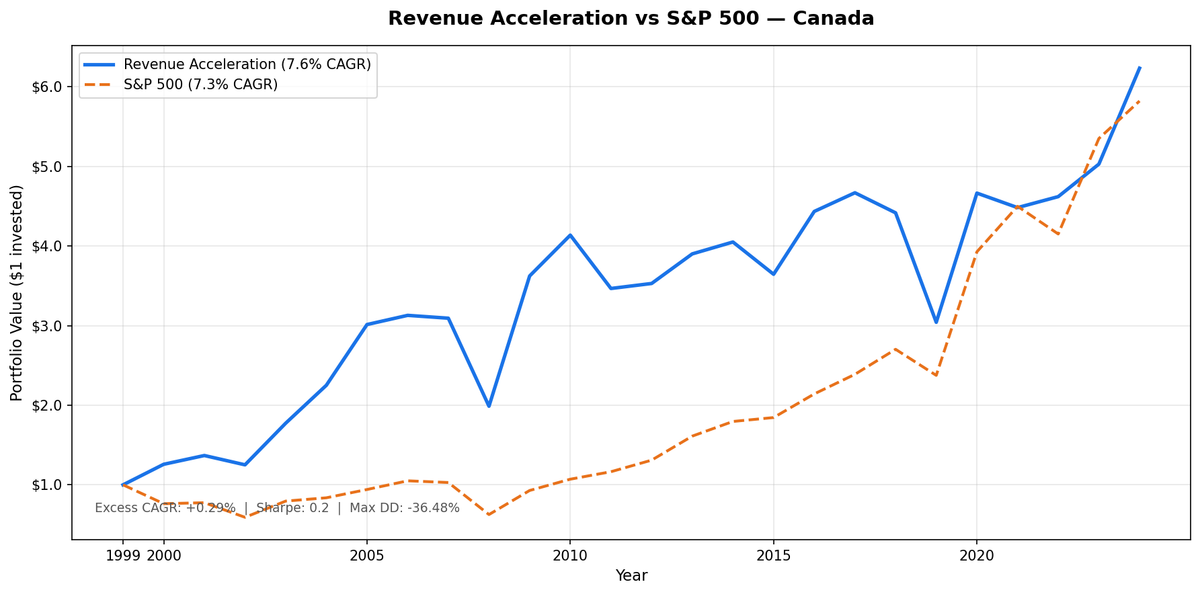

Canada is the only market in our 12-exchange study where the revenue acceleration strategy outperformed. The margin is thin: 7.60% CAGR vs 7.30% for the S&P 500, a +0.29% annual excess over 25 years. But the alpha number understates what the strategy actually did.

Contents

- Method

- What We Found

- A marginally positive result with exceptional downside protection.

- Year-by-Year Returns

- The defensive pattern is real.

- The late-cycle failure.

- What explains Canada's different profile?

- Limitations

- Takeaway

- Part of a Series

- Run This Screen Yourself

- References

The down capture ratio is 44.0%. When markets fell, Canadian revenue accelerators fell less than half as much as the S&P 500. That's the real result.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: TSX (Toronto Stock Exchange), market cap > CAD 250M Period: 2000–2025 (25 years) Rebalancing: Annual (April 1), equal weight Benchmark: S&P 500 Total Return (SPY, in USD) Cash rule: Hold cash if fewer than 10 stocks qualify Transaction costs: Size-tiered model (0.1–0.5% one-way based on market cap)

Note on returns: Canadian portfolio returns are computed in local currency (CAD). SPY returns are in USD. Currency effects are not hedged. The comparison reflects the actual experience of a Canadian investor holding domestic stocks vs a US benchmark — useful for relative analysis but not a precise currency-adjusted comparison.

Signal: revenue growth acceleration across 3 consecutive annual filings, filtered for ROE > 10%, debt/equity < 1.5, and minimum market cap. Top 30 by acceleration magnitude.

What We Found

A marginally positive result with exceptional downside protection.

| Metric | Revenue Accel (TSX) | S&P 500 |

|---|---|---|

| CAGR | 7.60% | 7.30% |

| Max Drawdown | -36.48% | -40.77% |

| Sharpe Ratio | 0.200 | 0.242 |

| Up Capture | 88.9% | — |

| Down Capture | 44.0% | — |

| Cash Periods | 0 of 25 | — |

| Avg Stocks | 23.2 | — |

The Sharpe ratio (0.200) is still below SPY (0.242), and up capture of 88.9% means the strategy misses some of the bull market gains. But a down capture of 44% is remarkable — in years when the benchmark fell, this portfolio fell less than half as much on average.

Zero cash periods and 23.2 average qualifying stocks confirm consistent coverage. Canada's revenue data quality is strong across the full 25-year period.

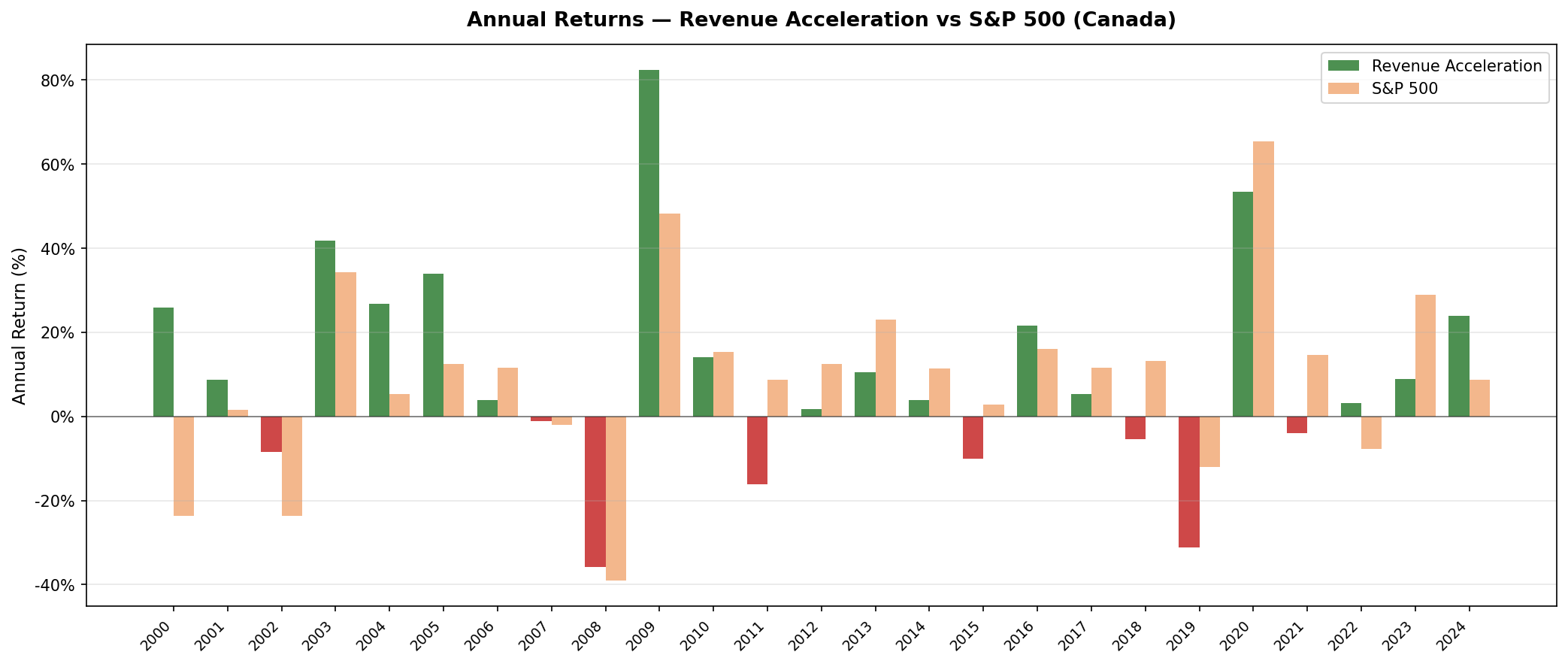

Year-by-Year Returns

| Year | Rev Accel (TSX) | S&P 500 | Excess |

|---|---|---|---|

| 2000 | +25.82% | -23.68% | +49.5% |

| 2001 | +8.75% | +1.61% | +7.1% |

| 2002 | -8.54% | -23.62% | +15.1% |

| 2003 | +41.77% | +34.33% | +7.4% |

| 2004 | +26.86% | +5.23% | +21.6% |

| 2005 | +33.90% | +12.43% | +21.5% |

| 2006 | +3.83% | +11.60% | -7.8% |

| 2007 | -1.14% | -2.03% | +0.9% |

| 2008 | -35.75% | -39.11% | +3.4% |

| 2009 | +82.33% | +48.25% | +34.1% |

| 2010 | +14.16% | +15.27% | -1.1% |

| 2011 | -16.20% | +8.77% | -25.0% |

| 2012 | +1.81% | +12.46% | -10.7% |

| 2013 | +10.54% | +23.07% | -12.5% |

| 2014 | +3.82% | +11.41% | -7.6% |

| 2015 | -10.01% | +2.74% | -12.8% |

| 2016 | +21.66% | +16.08% | +5.6% |

| 2017 | +5.29% | +11.49% | -6.2% |

| 2018 | -5.40% | +13.17% | -18.6% |

| 2019 | -31.13% | -12.12% | -19.0% |

| 2020 | +53.35% | +65.36% | -12.0% |

| 2021 | -3.91% | +14.55% | -18.5% |

| 2022 | +3.08% | -7.73% | +10.8% |

| 2023 | +8.84% | +28.90% | -20.1% |

| 2024 | +23.96% | +8.80% | +15.2% |

The defensive pattern is real.

The years where the strategy's downside protection shows up most clearly: 2000 (+49.5% excess as tech crashed), 2002 (+15.1% excess during the bear market), and 2008 (-35.75% vs SPY's -39.11%). In every major market downturn except 2011, the Canadian portfolio fell less than the S&P 500.

2022 is another clean example: the portfolio returned +3.08% in a year the S&P 500 fell -7.73%. That's not down capture — that's genuine protection.

The late-cycle failure.

The strategy's weak years follow a pattern: 2011, 2013, 2015, 2019, 2021, 2023. These are years of narrow market leadership or extended growth cycles where Canadian revenue accelerators missed the specific names driving returns. In 2019, the portfolio fell -31.13% vs SPY's -12.12% — the same late-cycle dynamic that destroyed the US version in the same year.

What explains Canada's different profile?

A plausible explanation: Canadian revenue acceleration selects heavily from energy, materials, and industrials — sectors tied to commodity cycles. When commodity prices accelerate (which shows up as revenue acceleration), these companies are genuinely cheap on fundamentals relative to their growth trajectory. They also tend to be more defensive in general market downturns because their earnings don't correlate as tightly with US tech and growth.

The US version picks more tech-heavy names. Canadian filters at the same thresholds land in a different sector mix.

This is speculation, not a proven mechanism — the backtest doesn't break down portfolio composition by sector. But the return profile is consistent with the theory.

Limitations

Currency translation not applied. Portfolio returns in CAD, benchmark in USD. In periods of significant CAD/USD movement (2002, 2016), this comparison overstates or understates true relative performance for a USD investor.

Small market effect. TSX is a smaller exchange than NYSE+NASDAQ+AMEX. With 23.2 average stocks in a concentrated exchange, idiosyncratic company risk is higher.

Survivorship bias. Current listings only. Companies that delisted during the period aren't tracked through failure.

The +0.29% excess is not statistically significant. Twenty-five annual data points with high volatility is insufficient to conclude that this strategy reliably outperforms. The excess could be noise. The downside protection is more robust — it shows up consistently across multiple down years.

Takeaway

Canada is the only market where revenue acceleration marginally outperformed — 7.60% vs 7.30% for the S&P 500. Don't overweight that number. With 25 annual observations and the volatility involved, +0.29% annual excess doesn't confirm the signal works here.

What the data does show: a 44% down capture ratio that held up consistently across multiple market downturns. That's a different result from the US (109.6% down capture) and Germany (58.5%), and it suggests the Canadian market's sector composition creates a different risk profile for revenue acceleration.

If you're looking for a portfolio that participates in bull markets while limiting crash exposure, the Canadian version of this signal produced that historically. Whether it continues to is a separate question.

Part of a Series

This post is part of our Revenue Acceleration global exchange comparison:

- [US] — Flagship result: 3.76% CAGR, -3.54% excess, 109.6% down capture

- Germany — -1.30% excess but best max drawdown in the study (-29.91%)

- [Revenue Acceleration: 12-Exchange Global Comparison] — Ranges from Canada +0.29% to Hong Kong -12.55%

Run This Screen Yourself

The current revenue acceleration screen for Canadian stocks:

WITH inc AS (

SELECT symbol, revenue, dateEpoch,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY dateEpoch DESC) AS rn

FROM income_statement

WHERE period = 'FY' AND revenue > 0

),

rev_calc AS (

SELECT r1.symbol,

(r1.revenue - r2.revenue) / NULLIF(r2.revenue, 0) AS growth_current,

(r2.revenue - r3.revenue) / NULLIF(r3.revenue, 0) AS growth_prior,

(r1.revenue - r2.revenue) / NULLIF(r2.revenue, 0)

- (r2.revenue - r3.revenue) / NULLIF(r3.revenue, 0) AS acceleration

FROM inc r1

JOIN inc r2 ON r1.symbol = r2.symbol AND r2.rn = 2

JOIN inc r3 ON r1.symbol = r3.symbol AND r3.rn = 3

WHERE r1.rn = 1

),

met AS (

SELECT symbol, returnOnEquity, marketCap,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY dateEpoch DESC) AS rn

FROM key_metrics WHERE period = 'FY'

),

rat AS (

SELECT symbol, debtToEquityRatio,

ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY dateEpoch DESC) AS rn

FROM financial_ratios WHERE period = 'FY'

)

SELECT rc.symbol,

p.companyName,

p.sector,

ROUND(rc.growth_current * 100, 1) AS current_growth_pct,

ROUND(rc.growth_prior * 100, 1) AS prior_growth_pct,

ROUND(rc.acceleration * 100, 1) AS acceleration_ppt,

ROUND(m.returnOnEquity * 100, 1) AS roe_pct,

ROUND(r.debtToEquityRatio, 2) AS de_ratio,

ROUND(m.marketCap / 1e9, 1) AS mktcap_b

FROM rev_calc rc

JOIN met m ON rc.symbol = m.symbol AND m.rn = 1

JOIN rat r ON rc.symbol = r.symbol AND r.rn = 1

JOIN profile p ON rc.symbol = p.symbol

WHERE rc.growth_current > rc.growth_prior

AND rc.growth_current > 0.05

AND m.returnOnEquity > 0.10

AND r.debtToEquityRatio >= 0

AND r.debtToEquityRatio < 1.5

AND m.marketCap > 250000000

AND p.exchange IN ('TSX')

ORDER BY rc.acceleration DESC

LIMIT 30

Run this screen on Ceta Research

References

- Chan, L., Karceski, J., & Lakonishok, J. (1996). "Momentum Strategies." Journal of Finance, 51(5), 1681–1713.

- Lakonishok, J., Shleifer, A., & Vishny, R. (1994). "Contrarian Investment, Extrapolation, and Risk." Journal of Finance, 49(5), 1541–1578.

Data: Ceta Research, FMP financial data warehouse. Universe: TSX. Annual rebalance (April), equal weight, transaction costs included, 2000–2025.

Past performance does not guarantee future results. This is educational content, not investment advice.