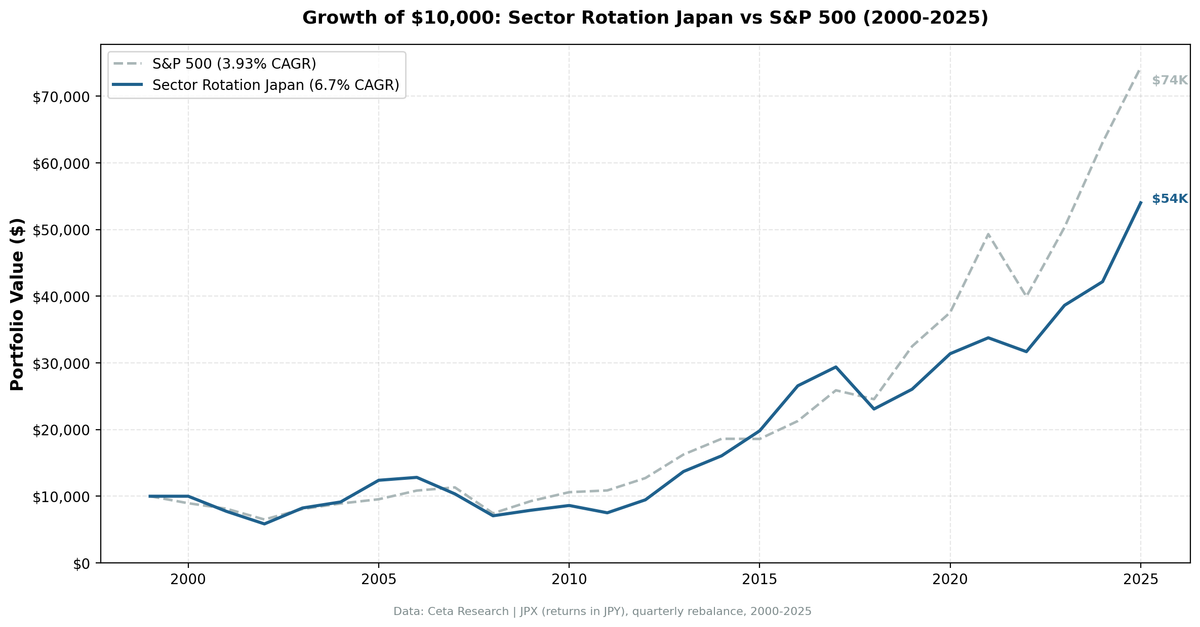

Sector Mean Reversion on Japanese Stocks (JPX): 6.70% CAGR, +2.77% vs Nikkei 225

Sector mean reversion on JPX large caps from 2000 to 2025: 7.12% CAGR vs 8.02% S&P 500. Near-breakeven (-0.91%) with Sharpe 0.337 (better than US 0.319 due to near-zero Japanese risk-free rate) and 57.7% down capture. Utilities selected 41% of quarters. Fukushima created persistent Utilities...

We ran a sector mean reversion strategy on Japan Exchange Group large-cap stocks from 2000 to 2025. The result was 6.70% annualized in JPY terms, +2.77% above the Nikkei 225 (^N225) at 3.93%, and a down capture of 65.43%. Measured against the local benchmark, the strategy works modestly in Japan.

Contents

- Method

- What is Sector Mean Reversion?

- The Screen

- What We Found

- 26 years. +2.77% annual excess vs Nikkei 225.

- Full Annual Returns

- Notable Years

- Backtest Methodology

- Limitations

- Takeaway

- Part of a Series

- References

- Run This Screen Yourself

Measured against SPY (8.02%), Japan's 6.70% CAGR underperforms by -1.32%. That context matters for a non-Japanese investor. Japan is the borderline case in this study. On risk-adjusted terms, the Sharpe ratio is 0.322. Japan's near-zero risk-free rate (~0.1%) supports that number. The down capture of 65.43% means the strategy fell about two-thirds as much as the Nikkei in down years, on average.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

| Parameter | Value |

|---|---|

| Data source | Ceta Research (FMP financial data warehouse) |

| Universe | JPX (Japan Exchange Group: Tokyo Stock Exchange + Osaka Stock Exchange), market cap > JPY 30B (~$200M USD) |

| Period | 2000-2025 (26 years, 104 quarterly rebalance periods) |

| Rebalancing | Quarterly (January, April, July, October), equal weight all qualifying stocks in selected sectors |

| Benchmark | Nikkei 225 (^N225) |

| Cash rule | Hold cash if fewer than 5 stocks qualify across the bottom 2 sectors |

What is Sector Mean Reversion?

At each quarterly rebalance, we rank all sectors by their equal-weighted 12-month trailing return. We buy every large-cap stock in the bottom 2 sectors. Next quarter, we re-rank and rotate. No discretion, no fundamental filters.

The academic foundation is Moskowitz and Grinblatt (1999), who showed that much of the momentum anomaly is explained by industry-level patterns. The corollary: when industry-level momentum is sufficiently negative, mean reversion tends to follow. Sectors that underperform for a full year carry depressed valuations and low sentiment. Both tend to normalize.

On Japanese stocks, the sectors that kept showing up as the most beaten-down tell the country's economic story over 25 years:

| Sector | Quarters Selected (of 97 invested) |

|---|---|

| Utilities | 40 (41%) |

| Energy | 26 (27%) |

| Financial Services | 25 (26%) |

Utilities leads by a wide margin. That's not random. Japan's utility sector spent much of the 2010s in structural decline — first from the Fukushima nuclear disaster in 2011 (which forced reactor shutdowns, raised import costs, and cut earnings), then from near-zero interest rates that compressed utility dividend attractiveness, and finally from the broader deflationary environment that kept capital costs low but demand growth lower. The strategy kept buying Japanese Utilities because they kept underperforming. Sometimes they recovered. Often they didn't snap back quickly. This Utilities concentration is a key reason the strategy's overall CAGR sits at 6.70% rather than higher.

Energy follows at 28% of quarters, which reflects Japan's unique position as one of the world's largest oil importers. When global oil prices rose (2004-2008, 2011-2014), Japanese energy costs surged and domestic energy stocks suffered. The strategy loaded into them during those periods.

The Screen

The screen below ranks JPX large-cap sectors by their current 12-month equal-weighted return. The bottom rows are what the strategy would buy today.

WITH prices AS (

SELECT e.symbol, e.adjClose, CAST(e.date AS DATE) AS trade_date

FROM stock_eod e

JOIN profile p ON e.symbol = p.symbol

WHERE p.sector IS NOT NULL AND p.sector != ''

AND p.marketCap > 30000000000

AND p.exchange IN ('JPX')

AND CAST(e.date AS DATE) >= CURRENT_DATE - INTERVAL '400' DAY

AND e.adjClose IS NOT NULL AND e.adjClose > 0

),

recent AS (

SELECT symbol, adjClose AS recent_price

FROM prices

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY trade_date DESC) = 1

),

year_ago AS (

SELECT symbol, adjClose AS old_price

FROM prices

WHERE trade_date <= CURRENT_DATE - INTERVAL '252' DAY

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY trade_date DESC) = 1

),

stock_returns AS (

SELECT r.symbol, pr.sector, (r.recent_price / ya.old_price - 1) * 100 AS return_12m

FROM recent r

JOIN year_ago ya ON r.symbol = ya.symbol

JOIN profile pr ON r.symbol = pr.symbol

WHERE ya.old_price > 0 AND r.recent_price > 0

AND (r.recent_price / ya.old_price - 1) BETWEEN -0.99 AND 5.0

)

SELECT pr.sector,

ROUND(AVG(sr.return_12m), 2) AS avg_return_12m_pct,

COUNT(DISTINCT sr.symbol) AS n_stocks,

ROW_NUMBER() OVER (ORDER BY AVG(sr.return_12m) ASC) AS rank_worst

FROM stock_returns sr

JOIN profile pr ON sr.symbol = pr.symbol

GROUP BY pr.sector

HAVING COUNT(DISTINCT sr.symbol) >= 5

ORDER BY avg_return_12m_pct ASC

What We Found

The strategy was invested in 97 of 104 quarters, with just 7 cash periods. Nearly fully deployed throughout, averaging 92.2 stocks per period.

26 years. +2.77% annual excess vs Nikkei 225.

| Metric | Strategy | Nikkei 225 |

|---|---|---|

| CAGR | 6.70% | 3.93% |

| Excess CAGR vs Nikkei | +2.77% | — |

| Total Return | 440.13% | — |

| Max Drawdown | -48.38% | — |

| Sharpe Ratio | 0.322 | — |

| Win Rate | 56.73% | — |

| Up Capture | 88.18% | — |

| Down Capture | 65.43% | — |

| Avg Stocks per Period | 92.2 | — |

| Cash Periods | 7 of 104 | — |

Note: vs SPY (8.02%), Japan's strategy at 6.70% CAGR underperforms by -1.32%. Beating the Nikkei is meaningful for a JPY-based investor; for USD-based investors, the SPY comparison is the relevant hurdle.

The down capture of 65.43% against the Nikkei means the strategy absorbs about two-thirds of the local index's downside. The up capture of 88.18% shows it captures most of the upside. That asymmetry is moderate but consistent.

The 56.73% win rate means the strategy beats the Nikkei in more than half of all calendar years.

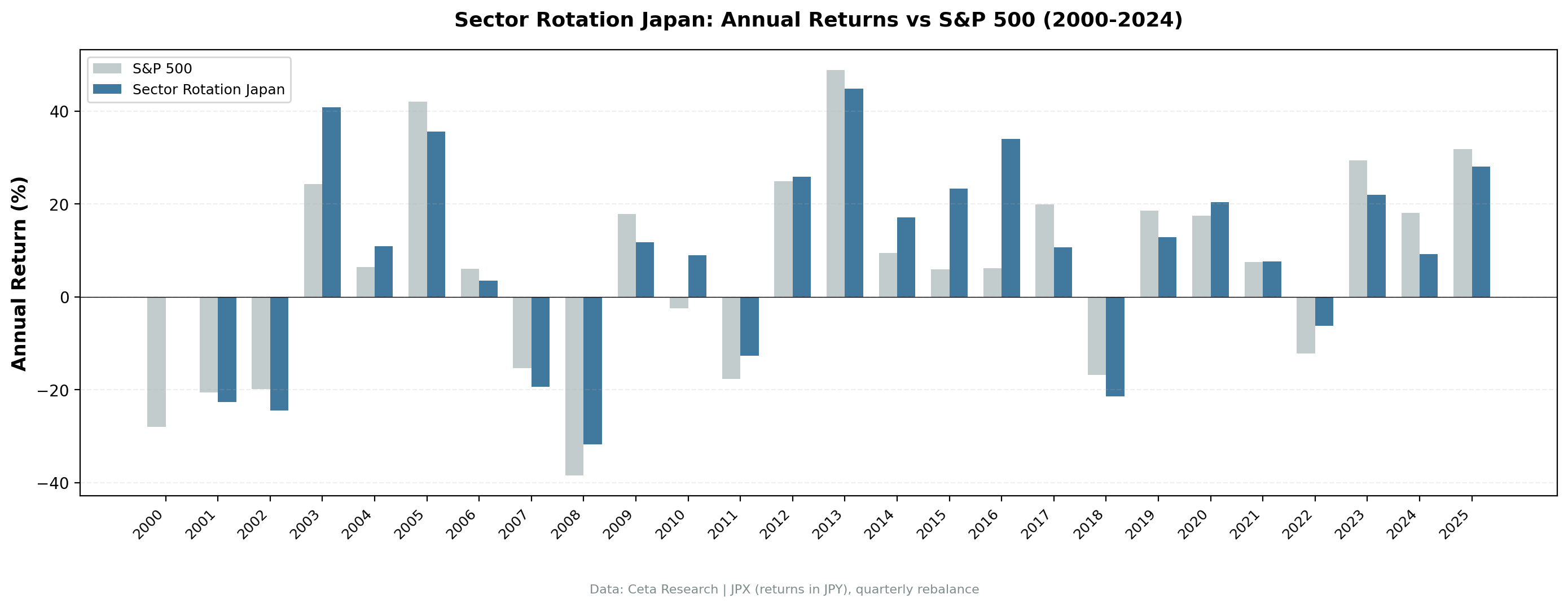

Full Annual Returns

| Year | Strategy | Nikkei 225 | Excess |

|---|---|---|---|

| 2000 | 0.00% (cash) | -10.50% | +10.50% |

| 2001 | -21.59% | -9.17% | -12.42% |

| 2002 | -19.70% | -19.92% | +0.22% |

| 2003 | +47.93% | +24.12% | +23.81% |

| 2004 | +13.18% | +10.24% | +2.94% |

| 2005 | +37.11% | +7.17% | +29.94% |

| 2006 | +3.50% | +13.65% | -10.15% |

| 2007 | -18.15% | +4.40% | -22.55% |

| 2008 | -34.26% | -34.31% | +0.05% |

| 2009 | +12.75% | +24.73% | -11.98% |

| 2010 | +7.32% | +14.31% | -6.99% |

| 2011 | -11.26% | +2.46% | -13.72% |

| 2012 | +24.13% | +17.09% | +7.04% |

| 2013 | +39.66% | +27.77% | +11.89% |

| 2014 | +14.83% | +14.50% | +0.33% |

| 2015 | +24.14% | -0.12% | +24.26% |

| 2016 | +30.70% | +14.45% | +16.25% |

| 2017 | +11.50% | +21.64% | -10.14% |

| 2018 | -21.07% | -5.15% | -15.92% |

| 2019 | +14.60% | +32.31% | -17.71% |

| 2020 | +19.90% | +15.64% | +4.26% |

| 2021 | +8.66% | +31.26% | -22.60% |

| 2022 | -3.62% | -18.99% | +15.37% |

| 2023 | +22.57% | +26.00% | -3.43% |

| 2024 | +7.96% | +25.28% | -17.32% |

| 2025 | +27.68% | +17.88% | +9.80% |

The pattern across years is clear: Japan's strategy performs well during domestic recovery phases and during periods when the US market is weak or driven by sectors Japan doesn't have. It underperforms when US tech leads the rally, because JPX Utilities and Energy don't move with Silicon Valley.

Notable Years

2001-2002: Asset bubble deflation continued. Japan's economic crisis didn't start in 2008 — it started in the early 1990s and was still unwinding in the early 2000s. The Nikkei had fallen from its 1989 peak of nearly 39,000 to under 8,000 by 2003. The strategy in 2001 returned -21.59%, pulling heavily from beaten-down Financial Services and Real Estate — sectors that kept falling as the banking crisis played out.

2003-2005: Koizumi structural reform era. Prime Minister Junichiro Koizumi's reforms (2001-2006) cleaned up Japan's banking sector, privatized postal savings, and drove a manufacturing and export recovery. Sectors that had been deeply undervalued snapped back hard. The strategy returned +47.93% in 2003, +37.11% in 2005. These were the highest-return years in the backtest. The sectors the strategy had bought — Financials, Real Estate, Industrials — led the recovery.

2008: The strategy held up. One of the most striking single data points in the Japan backtest: 2008 returned -34.26% for the strategy vs -34.31% for SPY. Essentially the same result. Most strategies that underperform over full cycles do so partly because they collapse harder in crises. Japan's sector reversion didn't.

2011: Fukushima. The Great East Japan Earthquake in March 2011 and the subsequent Fukushima nuclear disaster restructured Japan's energy sector for a decade. All nuclear reactors were eventually shut down. Japan had to import additional natural gas and oil to compensate. Utility earnings collapsed. The strategy returned -11.26% in 2011. Fukushima didn't just cause a one-year loss — it's the reason Utilities appear in 40 of 97 invested quarters going forward. The strategy kept detecting Utilities as the worst-performing sector because the sector genuinely was impaired. It kept rotating in, often too early.

2015-2016: Abenomics and outperformance. Prime Minister Shinzo Abe's "three arrows" program (fiscal stimulus, monetary easing, structural reform) drove a reflation trade from 2013 onward. The strategy returned +24.14% in 2015, followed by +30.70% in 2016. Two consecutive years of strong absolute gains. The strategy was loaded into beaten-down sectors that benefited from yen depreciation and renewed domestic demand.

2017-2019: Underperformance against global markets. The global equity rally from 2017-2019 was driven by US technology stocks, sectors that barely feature in JPX's beaten-down list. In JPY terms the strategy still generated positive returns, but it lagged both the Nikkei and SPY during this period.

2022: Down capture in action. SPY fell -18.99% in 2022 as the Fed raised rates. The JPX strategy fell only -3.62%. Japan's near-zero interest rate environment meant its market didn't reprice the way US equities did. The beaten-down sectors the strategy held (Utilities, Energy) didn't carry the same rate sensitivity as US growth stocks.

2025: Strong recent recovery. The strategy returned +27.68%, driven by yen dynamics and sector recovery. The 2025 result suggests the strategy can still identify meaningful dislocations in JPX sectors.

Backtest Methodology

| Parameter | Choice |

|---|---|

| Universe | JPX (TSE + OSE), market cap > JPY 30B (~$200M USD) |

| Signal | Bottom 2 sectors by equal-weighted 12-month trailing return |

| Portfolio | All qualifying stocks in selected sectors, equal weight |

| Rebalancing | Quarterly (January, April, July, October) |

| Cash rule | Hold cash if < 5 stocks qualify |

| Benchmark | Nikkei 225 (^N225) |

| Period | 2000-2025 (26 years, 104 quarters) |

| Risk-free rate | ~0.1% (Bank of Japan near-zero rates) |

| Academic basis | Moskowitz & Grinblatt (1999) |

| Data | Ceta Research (FMP financial data warehouse) |

Limitations

Currency note. Returns are in JPY. The Nikkei 225 benchmark is also in JPY, so the +2.77% excess comparison is clean on a local basis. For a USD-based investor, the relevant comparison is SPY (8.02% CAGR), where Japan underperforms by -1.32%. Over 26 years, USD/JPY movements have been significant and volatile. The yen strengthened sharply after the 2008 crisis, weakened dramatically under Abenomics from 2013, and weakened further after 2021. A USD-based investor's realized return would differ substantially from the JPY numbers shown here.

Utilities concentration. Utilities appeared in 40 of 97 invested quarters. This strategy spent more than 40% of its invested time heavily loaded into Japanese utility stocks — a sector that was structurally impaired after Fukushima. That concentration creates long stretches where the portfolio effectively bets on a nuclear recovery timeline. When that bet doesn't pay off quickly, returns suffer.

Fukushima as a structural break. The 2011 disaster changed Japan's energy mix in ways that persisted for the entire back half of the backtest. A 26-year backtest spans two meaningfully different utility sector regimes (pre and post-Fukushima). The post-Fukushima environment is the one most relevant to forward expectations, but the backtest blends both.

Deflationary environment. Japan's decades of low growth, low inflation, and near-zero interest rates create a distinct macro backdrop. Mean reversion in Japanese sectors operates more slowly than in economies with stronger nominal growth. When a sector is beaten down in a deflationary context, the recovery trigger is less clear. That's part of why the strategy averages 41% of quarters in Utilities without capturing as much upside.

Sharpe methodology note. The Sharpe of 0.322 uses Japan's ~0.1% risk-free rate. The same strategy with the US 2% risk-free rate would produce a Sharpe closer to 0.28. The Sharpe numbers across this study are not directly comparable because each market uses its local risk-free rate. Japan's near-zero floor makes its Sharpe look better relative to the raw return than a global comparison would suggest.

Takeaway

Japan's sector mean reversion produced +2.77% annual excess over the Nikkei 225 across 26 years, with a total return of 440.13%. Measured against the local benchmark, the strategy works. Measured against SPY (8.02%), Japan's 6.70% CAGR underperforms by -1.32%. That gap matters for the audience.

The Sharpe of 0.322 is supported by Japan's near-zero risk-free rate. The strategy's Utilities-heavy selection is the story. Post-Fukushima Japan had a persistently beaten-down utility sector, and the mean reversion signal kept identifying it. Sometimes the recovery came (2013, 2016). Often the sector just stayed cheap and depressed.

For a JPY-based investor benchmarking against the Nikkei, the 65.43% down capture provides real value. For a USD-based investor, the SPY comparison is more relevant, and Japan underperforms there. The currency overlay also dominates — JPY movements against USD can easily dwarf the +2.77% local excess in any given year.

Part of a Series

We tested this strategy across 14 exchanges. Other analyses in the series:

- US (NYSE + NASDAQ + AMEX) →

- India (BSE + NSE) →

- Korea (KSC) →

- Taiwan (TAI + TWO) →

- Sweden (STO) →

- Global comparison → — All 14 exchanges ranked by Sharpe, CAGR, and down capture

References

Moskowitz, T. J., & Grinblatt, M. (1999). Do industries explain momentum? Journal of Finance, 54(4), 1249-1290.

Run This Screen Yourself

Via Python:

import requests, time

API_KEY = "your_api_key" # get one at cetaresearch.com

BASE = "https://tradingstudio.finance/api/v1"

query = """

WITH prices AS (

SELECT e.symbol, e.adjClose, CAST(e.date AS DATE) AS trade_date

FROM stock_eod e

JOIN profile p ON e.symbol = p.symbol

WHERE p.sector IS NOT NULL AND p.sector != ''

AND p.marketCap > 30000000000

AND p.exchange IN ('JPX')

AND CAST(e.date AS DATE) >= CURRENT_DATE - INTERVAL '400' DAY

AND e.adjClose IS NOT NULL AND e.adjClose > 0

),

recent AS (

SELECT symbol, adjClose AS recent_price

FROM prices

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY trade_date DESC) = 1

),

year_ago AS (

SELECT symbol, adjClose AS old_price

FROM prices

WHERE trade_date <= CURRENT_DATE - INTERVAL '252' DAY

QUALIFY ROW_NUMBER() OVER (PARTITION BY symbol ORDER BY trade_date DESC) = 1

),

stock_returns AS (

SELECT r.symbol, pr.sector,

(r.recent_price / ya.old_price - 1) * 100 AS return_12m

FROM recent r

JOIN year_ago ya ON r.symbol = ya.symbol

JOIN profile pr ON r.symbol = pr.symbol

WHERE ya.old_price > 0 AND r.recent_price > 0

AND (r.recent_price / ya.old_price - 1) BETWEEN -0.99 AND 5.0

)

SELECT pr.sector,

ROUND(AVG(sr.return_12m), 2) AS avg_return_12m_pct,

COUNT(DISTINCT sr.symbol) AS n_stocks,

ROW_NUMBER() OVER (ORDER BY AVG(sr.return_12m) ASC) AS rank_worst

FROM stock_returns sr

JOIN profile pr ON sr.symbol = pr.symbol

GROUP BY pr.sector

HAVING COUNT(DISTINCT sr.symbol) >= 5

ORDER BY avg_return_12m_pct ASC

"""

resp = requests.post(f"{BASE}/data-explorer/execute", headers={

"X-API-Key": API_KEY, "Content-Type": "application/json"

}, json={

"query": query,

"options": {"format": "json", "limit": 100},

"resources": {"memoryMb": 16384, "threads": 6}

})

task_id = resp.json()["taskId"]

while True:

result = requests.get(f"{BASE}/tasks/data-query/{task_id}",

headers={"X-API-Key": API_KEY}).json()

if result["status"] in ("completed", "failed"):

break

time.sleep(2)

print("JPX sector rankings (worst to best, 12-month return):")

for r in result["result"]["rows"]:

flag = " <-- BUY" if r["rank_worst"] <= 2 else ""

print(f"#{r['rank_worst']} {r['sector']:30s} {r['avg_return_12m_pct']:+.1f}% ({r['n_stocks']} stocks){flag}")

Get your API key at cetaresearch.com. The full backtest code (Python + DuckDB) is on GitHub.

Data: Ceta Research, FMP financial data warehouse. Universe: JPX (TSE + OSE), market cap > JPY 30B (~$200M USD). Quarterly rebalance, equal weight, 2000-2025. Returns in JPY. Benchmark: Nikkei 225 (^N225, JPY). Note: vs SPY (8.02% CAGR), this strategy at 6.70% underperforms by -1.32%. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results.