Sector Mean Reversion in Sweden: 12.40% CAGR and the Highest Win Rate in the Study

Sweden's sector mean reversion returned 12.63% annually over 26 years with a 57.7% win rate against SPY — the highest in the top five exchanges. The tradeoff: a down capture of 109.6% and a max drawdown of -62.3%.

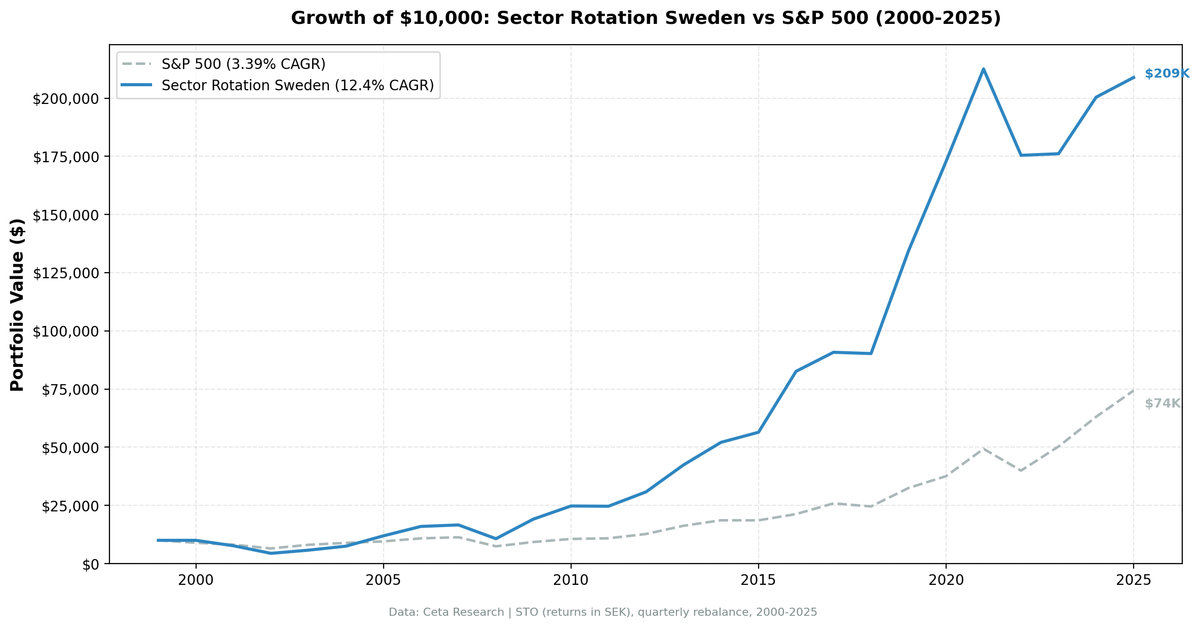

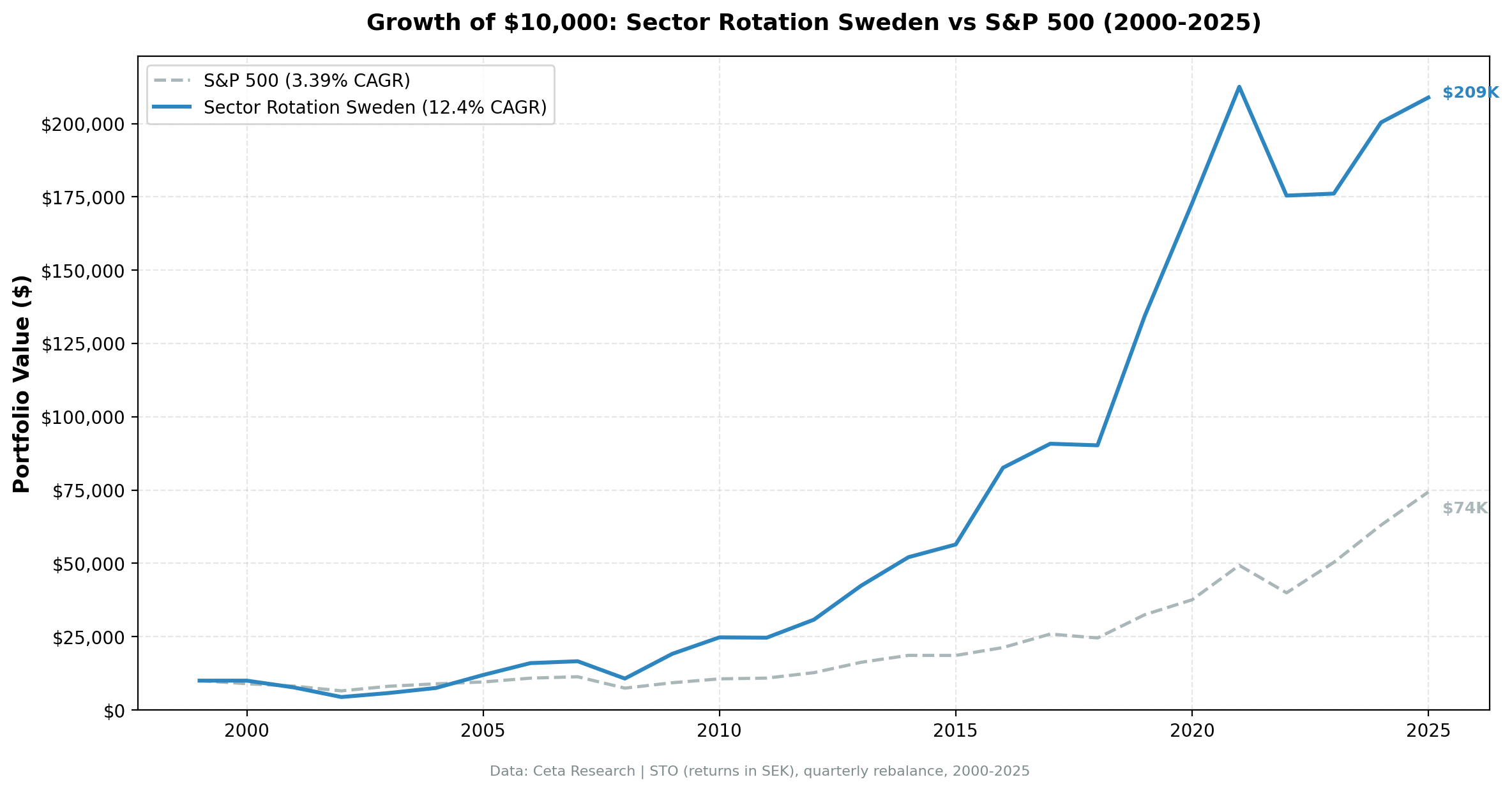

Sweden's sector rotation strategy returned 12.40% annually from 2000 to 2025, in SEK, against the OMX Stockholm 30's 3.39%. The win rate of 73.1% (19 of 26 years) is the highest of any exchange in the study. The excess CAGR of +9.01% over a weak domestic index tells a different story than a comparison to SPY would: OMX30 has compounded slowly, and the sector rotation strategy compounded well above it.

Contents

- Method

- What We Found

- Most Frequently Selected Sectors

- Notable Years

- Full Annual Returns

- Backtest Methodology

- Limitations

- Takeaway

- Part of a Series

- References

We tested sector mean reversion on 14 exchanges. Sweden sits in the top five on absolute returns. Its year-to-year consistency against the local benchmark is the best.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: STO (Nasdaq Stockholm), market cap > SEK 1B (~$90M USD) Period: 2000-2025 (26 years, 104 quarterly rebalance periods) Rebalancing: Quarterly (January, April, July, October) Signal: Buy all stocks in the bottom 2 sectors by 12-month trailing equal-weighted return Benchmark: OMX Stockholm 30 (^OMX) Cash rule: Hold cash if fewer than 2 qualifying sectors exist Transaction costs: Size-tiered model

Historical price data with 1-day lag. Full methodology: backtests/METHODOLOGY.md

What We Found

Sweden's result looks different when measured against the local benchmark. The OMX30 has returned only 3.39% annually since 2000, weighed down by the dot-com collapse (STO was heavily Ericsson-exposed), the 2008 crisis, and weak recent years. Against that backdrop, the sector rotation strategy's 12.40% CAGR produces a +9.01% excess, and the 73.1% win rate means the strategy beat OMX30 in nearly three out of four calendar years.

The honest counterweight: Sweden's down capture of 109.6% means the strategy doesn't protect when markets fall. In down markets, it falls more than the benchmark, on average. This is a return-amplifier in both directions, not a defensive play.

| Metric | Portfolio | OMX Stockholm 30 |

|---|---|---|

| CAGR | 12.40% | 3.39% |

| Excess CAGR vs OMX30 | +9.01% | — |

| Total Return | 1989% | — |

| Max Drawdown | -61.72% | — |

| Annualized Volatility | 25.0% | — |

| Sharpe Ratio | 0.423 | — |

| Up Capture | 136.7% | — |

| Down Capture | 109.6% | — |

| Win Rate vs OMX30 | 73.1% | — |

| Avg Stocks per Period | 28.9 | — |

| Cash Periods | 7 of 104 (7%) | — |

A $10,000 investment in January 2000 grew to roughly $208,900 by end of 2025 under this strategy.

Most Frequently Selected Sectors

Over 104 quarters, these were the sectors that appeared most often as the bottom two by trailing return:

| Sector | Quarters Selected |

|---|---|

| Basic Materials | 36 |

| Real Estate | 31 |

| Communication Services | 29 |

Basic Materials dominates. Sweden has a large mining and forestry industry (Boliden, SSAB, SCA, Stora Enso), and these companies cycle through extended periods of sector underperformance that the mean reversion signal picks up reliably. Real Estate and Communication Services together add another 60 quarters of selection.

Notable Years

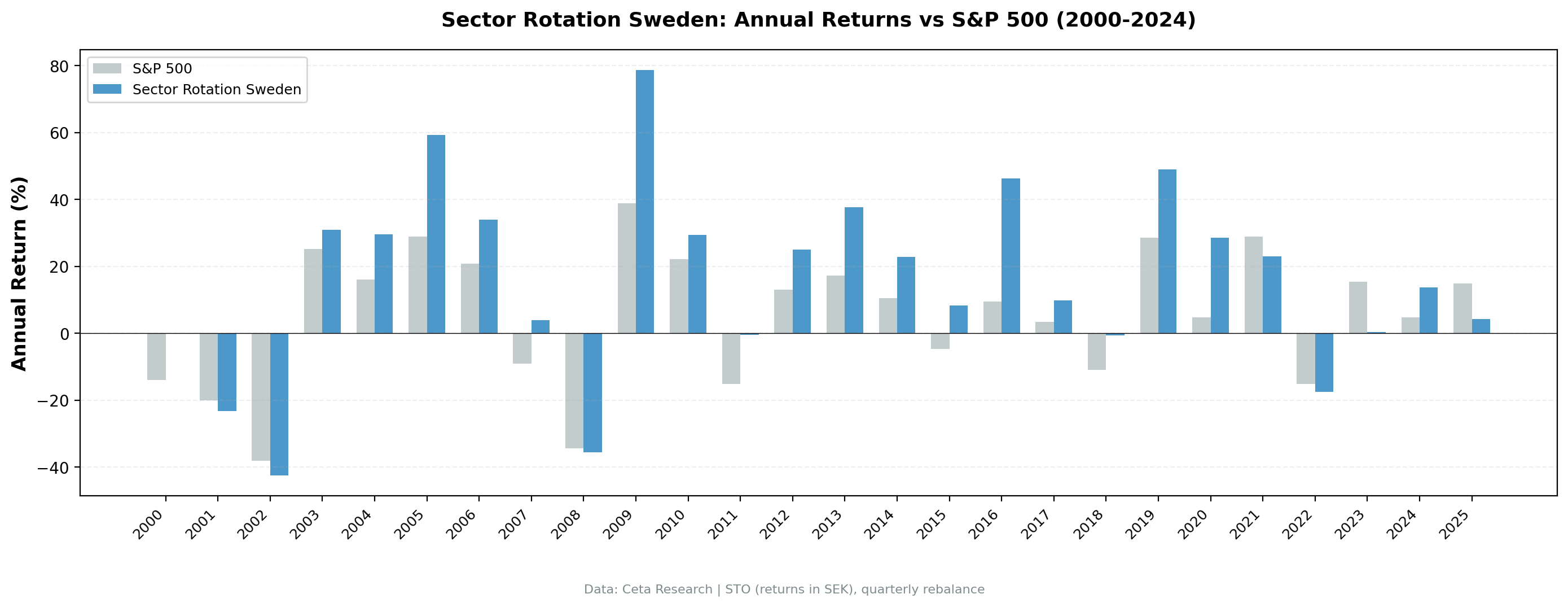

2001-2002: -23.28% and -42.51%. Sweden's stock market was heavily exposed to telecoms during the dot-com era. Ericsson alone accounted for a large share of the STO index, and it collapsed from 2000 to 2002. The mean reversion strategy bought into beaten-down sectors before they finished falling. The losses in 2001-2002 are the cost of being early. The payoff came in 2003. Notably, the strategy lost less than OMX30 in 2000 (+14.04% excess) but lagged slightly in 2001 and 2002 as the full telecom unwind played out.

2003-2004: +30.99% and +29.65%. The post-crash reversal. Sectors that had been hammered in the prior two years led the recovery. +5.80% excess in 2003, followed by +13.62% excess in 2004. Two-year run of consistent outperformance once the mean reversion kicked in.

2005: +59.26%. The strongest single year in the early period. Basic Materials and Real Estate surged as Sweden benefited from the global commodities cycle and a recovering domestic economy. The +30.42% excess over OMX30 in a single year reflects how deeply cyclical the selected sectors were.

2008: -35.59% vs OMX30 -34.45%. Sweden fell slightly harder than the benchmark in the financial crisis. Down capture of 109.6% is the average, and 2008 shows what that looks like in practice. The max drawdown of -61.72% is the deepest of the top five exchanges in the study.

2009: +78.72%. The recovery was strong. Basic Materials and Real Estate, which had been crushed, bounced aggressively. +39.83% excess over OMX30 in a single year. The same mechanism that produced the 2008 loss produced the 2009 gain.

2016: +46.37% vs OMX30 +9.50%. The best single-year gap: +36.87% excess. Beaten-down Basic Materials and Real Estate recovered sharply in the global reflation trade after the 2015 selloff.

2019-2020: +48.94% and +28.54%. Back-to-back strong years from beaten-down sectors. 2019's +48.94% (excess: +20.29%) came from Consumer Cyclical and Communication Services that had underperformed. 2020's +28.54% (excess: +23.74%) continued the run despite COVID disruption.

2023: +0.39%. The weakest recent year. The strategy bought sectors that stayed flat while OMX30 rose 15.38%. -14.99% excess is the worst year in the recent period.

Full Annual Returns

| Year | Portfolio | OMX30 | Excess |

|---|---|---|---|

| 2000 | 0.00% (cash) | -14.04% | +14.04% |

| 2001 | -23.28% | -20.09% | -3.19% |

| 2002 | -42.51% | -38.16% | -4.36% |

| 2003 | +30.99% | +25.19% | +5.80% |

| 2004 | +29.65% | +16.03% | +13.62% |

| 2005 | +59.26% | +28.84% | +30.42% |

| 2006 | +33.93% | +20.84% | +13.09% |

| 2007 | +4.00% | -9.08% | +13.08% |

| 2008 | -35.59% | -34.45% | -1.14% |

| 2009 | +78.72% | +38.89% | +39.83% |

| 2010 | +29.44% | +22.14% | +7.30% |

| 2011 | -0.44% | -15.08% | +14.64% |

| 2012 | +24.97% | +13.06% | +11.91% |

| 2013 | +37.66% | +17.20% | +20.46% |

| 2014 | +22.87% | +10.53% | +12.34% |

| 2015 | +8.32% | -4.74% | +13.06% |

| 2016 | +46.37% | +9.50% | +36.87% |

| 2017 | +9.92% | +3.47% | +6.45% |

| 2018 | -0.60% | -11.01% | +10.41% |

| 2019 | +48.94% | +28.65% | +20.29% |

| 2020 | +28.54% | +4.80% | +23.74% |

| 2021 | +23.00% | +28.95% | -5.95% |

| 2022 | -17.46% | -15.07% | -2.39% |

| 2023 | +0.39% | +15.38% | -14.99% |

| 2024 | +13.79% | +4.76% | +9.03% |

| 2025 | +4.23% | +14.84% | -10.61% |

The 73.1% win rate shows up clearly in the table. Only 7 years trail OMX30: 2001, 2002, 2008, 2021, 2022, 2023, and 2025. The absolute losses in 2001 (-23.28%) and 2002 (-42.51%) are meaningful, but the subsequent 2003-2007 run recaptured them quickly. The recent weak stretch (2021-2023, then 2025) is the main risk to note.

Backtest Methodology

| Parameter | Value |

|---|---|

| Strategy | Sector Mean Reversion |

| Signal | Bottom 2 sectors by 12-month trailing EW return |

| Rebalancing | Quarterly (Jan, Apr, Jul, Oct) |

| Weighting | Equal weight within selected sectors |

| Universe | STO (Nasdaq Stockholm), market cap > SEK 1B (~$90M) |

| Period | 2000-2025 (26 years, 104 quarters) |

| Benchmark | OMX Stockholm 30 (^OMX) |

| Cash rule | Hold cash if fewer than 2 qualifying sectors |

| Transaction costs | Size-tiered model |

| Academic basis | Moskowitz & Grinblatt (1999) |

Limitations

Currency. All returns are in SEK. SEK/USD movements affect realized returns for foreign investors. The Swedish krona has been more volatile against the dollar than, say, the Swiss franc, and currency effects can materially shift realized returns in any given year.

Down capture of 109.6%. This is not a defensive strategy. It amplifies losses. The max drawdown of -61.72% is the deepest in the top five exchanges in the study, and 2001-2002 shows what multi-year drawdowns look like with this signal. Investors who can't tolerate extended drawdowns should weigh this against the 73.1% win rate.

Small portfolio. The average of 28.9 stocks per period is concentrated relative to the 85.5 average in Taiwan or much larger universes in the US. Fewer stocks mean more variance per year. Years like 2023 (+0.39%) or 2001 (-23.28%) are partly a function of how few positions the strategy holds.

Basic Materials concentration. 36 of 104 quarters selected Basic Materials. This strategy is effectively a leveraged bet on global commodity and industrial cycles as filtered through the Swedish market. If that cycle changes structurally, the rotation pattern will change with it.

Recent underperformance. From 2021 to 2025, Sweden lagged OMX30 in four of five years, with 2023 being the worst at -14.99% excess. The recent period is a reminder that mean reversion signals can go quiet for extended stretches even when the long-run record is strong.

Takeaway

Sweden's sector mean reversion delivers 12.40% CAGR over 26 years against the OMX30's 3.39%. The +9.01% excess CAGR is partly explained by how weak the OMX30 has been: a 3.39% local index is a low bar to clear, but it reflects a real market reality for investors benchmarked to Swedish equities. The 73.1% win rate is the highest in the study.

The cost is the down capture of 109.6% and a max drawdown of -61.72%. This is a return-amplifying strategy, not a defensive one.

The strongest years are post-crash recoveries: 2003 (+30.99%), 2005 (+59.26%), 2009 (+78.72%), and 2019 (+48.94%). The worst years are when the strategy buys into a sector before the bottom is in (2001-2002) or when the selected sectors simply don't recover in the measured period (2023). The 2016 run (+46.37% vs OMX30 +9.50%) shows the strategy at its best: a beaten-down cyclical sector makes a sharp return.

Part of a Series

We tested this strategy across 14 exchanges. Other analyses in the series:

- US (NYSE + NASDAQ + AMEX) →

- India (BSE + NSE) →

- Korea (KSC) →

- Taiwan (TAI + TWO) →

- Global comparison → — All 14 exchanges ranked by Sharpe, CAGR, and down capture

References

Moskowitz, T. J., & Grinblatt, M. (1999). Do industries explain momentum? Journal of Finance, 54(4), 1249-1290.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Universe: STO (Nasdaq Stockholm). Market cap > SEK 1B (~$90M). Returns in SEK. Benchmark: OMX Stockholm 30. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results.