Small-Cap Growth Backtest US: The Size Premium Is Dead

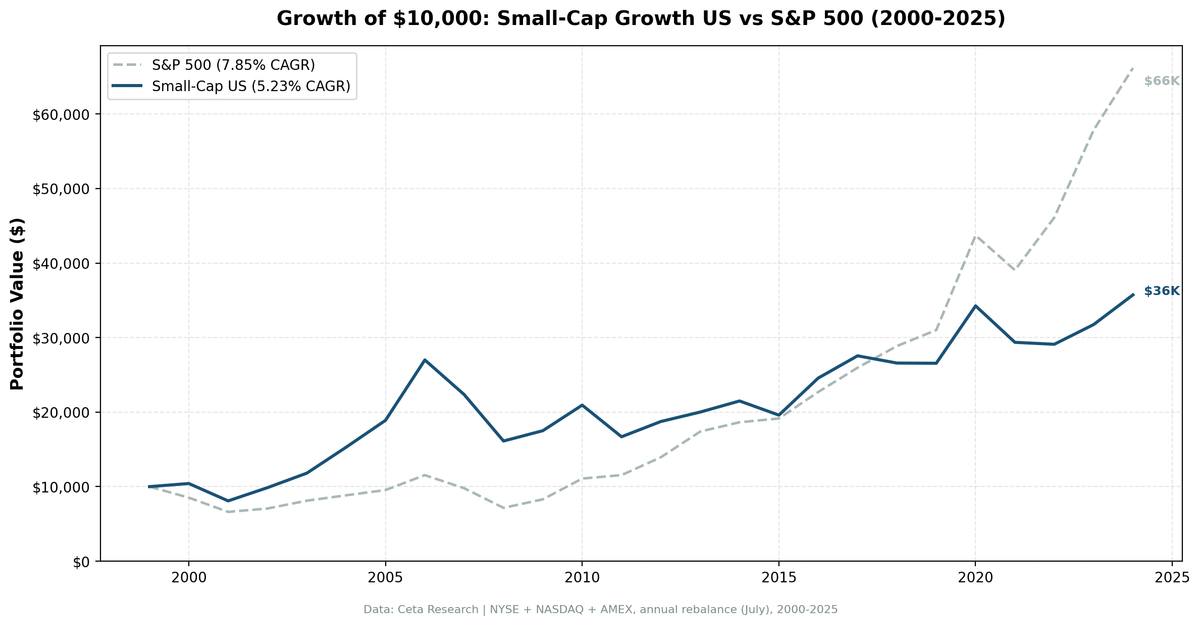

25 years of data, 36% win rate against the S&P 500, and $10K that became $35,734 while the index turned it into $65,900. The small-cap growth premium in the US has effectively disappeared.

The academic case for small-cap stocks is one of the most cited findings in finance. Banz (1981) documented it. Fama and French (1993) built it into their three-factor model. Decades of textbooks told investors that smaller companies deliver higher returns because they carry more risk and receive less analyst attention.

Contents

- What We Tested

- What We Found

- Annual Returns: 25 Years

- When It Works, When It Fails

- Why the Premium Disappeared

- Comparison to Other Markets

- Limitations

- Run It Yourself

- Takeaway

- References

We ran 25 years of data on the US market to see if that's still true. It isn't.

$10,000 invested in 2000 using this strategy became $35,734 by end of 2024. The S&P 500 turned the same $10,000 into approximately $65,900. That's a -2.63% annual underperformance across a quarter century. The strategy beat SPY in only 9 of 25 years, a 36% win rate.

The size premium in the US has been arbitraged away. Here's the evidence.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

What We Tested

The strategy screens for small-cap US stocks showing genuine revenue momentum:

- Market cap: $50M to $2B (small-cap range, 5%-200% of the exchange threshold)

- Revenue growth: >15% year-over-year (fiscal year)

- Profitability: Net income > 0 (no money-losers)

- Leverage: Debt-to-equity < 2.0 (avoiding overleveraged names)

- Selection: Top 30 by revenue growth, equal-weighted

- Rebalancing: Annual in July, with a 45-day filing lag to avoid look-ahead bias

The signal blends the size factor (Fama & French, 1993) with a growth quality filter. We're not just buying small companies, we're buying small companies that are actually growing profitably without excessive debt.

Universe covers NYSE, NASDAQ, and AMEX. Data from the FMP financial data warehouse, 2000-2024. Backtests run on the Ceta Research platform. Full methodology at METHODOLOGY.md.

You can run the exact stock selection query here: cetaresearch.com/data-explorer?q=HvOnWyI67o

What We Found

The headline number is -2.63%/yr excess return over 25 years. That compounds into a large gap.

The up/down capture ratio tells the real story. The portfolio captured 77.3% of SPY's upside but 86.2% of its downside. You want those numbers to be the other way around. A good strategy should capture more upside than downside. This one does the opposite, which explains why it trails even though it has some strong individual years.

The worst excess year was 2011 (-24.8% relative to SPY), when the portfolio fell 20.7% while SPY gained 4.1%. The best years came early: 2000 through 2006, when small-cap value was less crowded and institutional money hadn't fully colonized the space.

The early vs late split matters. 2000-2006 shows meaningful alpha. 2007 onward is mostly a story of underperformance. This pattern fits what we'd expect from a premium that gets discovered and arbitraged away. Small-cap ETFs, factor funds, and quant strategies now systematically target these stocks. The inefficiency that created the premium no longer exists at the scale it once did.

The 36% win rate is lower than it looks. In most years this strategy falls short, occasionally by a lot. The worst year was 2011: -20.3% vs SPY +4.2% (-24.5% excess). The years it wins tend to be modest outperformance. The years it loses can be punishing.

Annual Returns: 25 Years

| Year | Strategy | SPY | Excess |

|---|---|---|---|

| 2000 | +4.2% | -14.8% | +19.0% |

| 2001 | -22.4% | -22.4% | +0.1% |

| 2002 | +22.0% | +6.9% | +15.1% |

| 2003 | +19.7% | +14.9% | +4.8% |

| 2004 | +29.5% | +8.9% | +20.6% |

| 2005 | +23.6% | +8.0% | +15.6% |

| 2006 | +42.9% | +20.9% | +21.9% |

| 2007 | -17.2% | -15.2% | -2.0% |

| 2008 | -27.9% | -26.9% | -1.0% |

| 2009 | +8.6% | +16.0% | -7.4% |

| 2010 | +19.6% | +33.5% | -14.0% |

| 2011 | -20.3% | +4.2% | -24.5% |

| 2012 | +12.3% | +20.7% | -8.5% |

| 2013 | +6.8% | +24.7% | -18.0% |

| 2014 | +7.4% | +7.2% | +0.3% |

| 2015 | -8.8% | +2.7% | -11.5% |

| 2016 | +25.4% | +18.6% | +6.8% |

| 2017 | +12.2% | +14.3% | -2.2% |

| 2018 | -3.5% | +11.2% | -14.7% |

| 2019 | -0.1% | +7.4% | -7.5% |

| 2020 | +29.0% | +41.0% | -12.0% |

| 2021 | -14.3% | -10.7% | -3.6% |

| 2022 | -0.9% | +18.1% | -19.0% |

| 2023 | +9.1% | +25.4% | -16.3% |

| 2024 | +12.5% | +14.4% | -1.9% |

The early period (2000-2006) shows consistent alpha. Seven years, six of which beat SPY. This was before small-cap factor investing became a crowded trade. After 2010, the picture changes sharply. Only four years beat SPY in the 2010-2024 period.

When It Works, When It Fails

The strategy's strongest stretch was 2000-2006. It also had a solid 2016 and a reasonable 2020. These align with periods of broader small-cap outperformance — market dislocations, recovery phases, or moments when large-cap tech wasn't dominating.

It fails persistently in the era of mega-cap dominance. 2013, 2017, 2019, 2020, 2022, 2023 all saw large-cap growth stocks pull SPY higher while small-caps struggled to keep up. The strategy's -27.5% in 2008 wasn't much worse than SPY's -26.1%, but the 2011 crash (-20.7% vs SPY's +4.1%) demonstrates how quickly drawdowns compound relative to the index.

MaxDD of -40.29% is slightly worse than SPY's -36.27% for the same period. You're taking comparable downside risk for less return.

Why the Premium Disappeared

Van Dijk (2011) posed the question directly: "Is size dead?" His review found the size premium had weakened substantially since the 1980s. There are a few plausible reasons:

Capacity crowding. Small-cap factor funds, ETFs like IWM, and systematic quant strategies now hold large portions of the small-cap universe. When capital floods into an inefficiency, the inefficiency shrinks.

Reporting improvements. The original size premium partly reflected information asymmetry. Analyst coverage was thin for small companies. Now, data is cheap, screens are commoditized, and even retail investors run the same filters.

Survivorship in the premium. Early studies may have overstated returns through survivorship bias in databases. Modern replications with cleaner data show smaller effects.

The growth filter specifically. High-revenue-growth small-caps attract momentum traders. When momentum works, the strategy does well. When it doesn't (2011, 2019, 2023), the portfolio lags badly.

Comparison to Other Markets

This strategy doesn't fail everywhere. In emerging and frontier markets, the picture looks very different.

India (NSE): 13.44% CAGR, +5.59% excess vs SPY, the strongest result in our 14-exchange study. China (SHZ/SHH): 10.19% CAGR, +2.34% excess vs SPY. South Africa (JNB): 10.81% CAGR, +2.96% excess.

The pattern is consistent: the small-cap growth premium survives where markets are less efficient. Fewer analysts, less institutional coverage, less systematic capital. The US is the most efficiently priced equity market in the world. That's precisely why the premium doesn't exist here anymore.

See our regional comparison post for the full cross-market breakdown.

Limitations

- Slippage and liquidity: Small-cap stocks can be illiquid. A 25-stock equal-weight portfolio rebalanced annually would face real transaction costs and market impact that aren't captured here.

- Filing lag: We apply a 45-day lag to avoid look-ahead bias, but some small-cap financials are filed later.

- Equal weighting: The strategy holds 30 stocks equally weighted. In practice, position sizing around liquidity constraints would reduce returns.

- Delisting bias: Stocks that were delisted are excluded from the universe in standard databases, which may slightly overstate returns.

Run It Yourself

The stock selection query is publicly available: cetaresearch.com/data-explorer?q=HvOnWyI67o

This runs against the live FMP financial data warehouse on the Ceta Research platform. You can modify the revenue growth threshold, leverage filter, or market cap bounds directly in SQL and re-run.

Takeaway

The US small-cap growth premium was real. It worked from roughly 1981 through the mid-2000s. Since then, systematic capital has priced it away. 25 years of data with a 36% win rate and -2.25%/yr excess return isn't noise. It's a signal that the arbitrage has been completed.

If you're looking for the size premium in 2025, look outside the US. The data from India and China suggests it's alive in markets where analyst coverage is thin and institutional capital is light. In the US, it's gone.

References

- Banz, R. (1981). "The Relationship Between Return and Market Value of Common Stocks." Journal of Financial Economics, 9(1), 3-18.

- Fama, E. & French, K. (1992). "The Cross-Section of Expected Stock Returns." Journal of Finance, 47(2), 427-465.

- Fama, E. & French, K. (1993). "Common Risk Factors in the Returns on Stocks and Bonds." Journal of Financial Economics, 33(1), 3-56.

- Van Dijk, M. (2011). "Is size dead? A review of the size effect in equity returns." Journal of Banking & Finance, 35(12), 3263-3274.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results. This is educational content, not investment advice.