Yield Gap India: Strong Absolute Returns, but Sensex Leads on Local Terms (2006-2025)

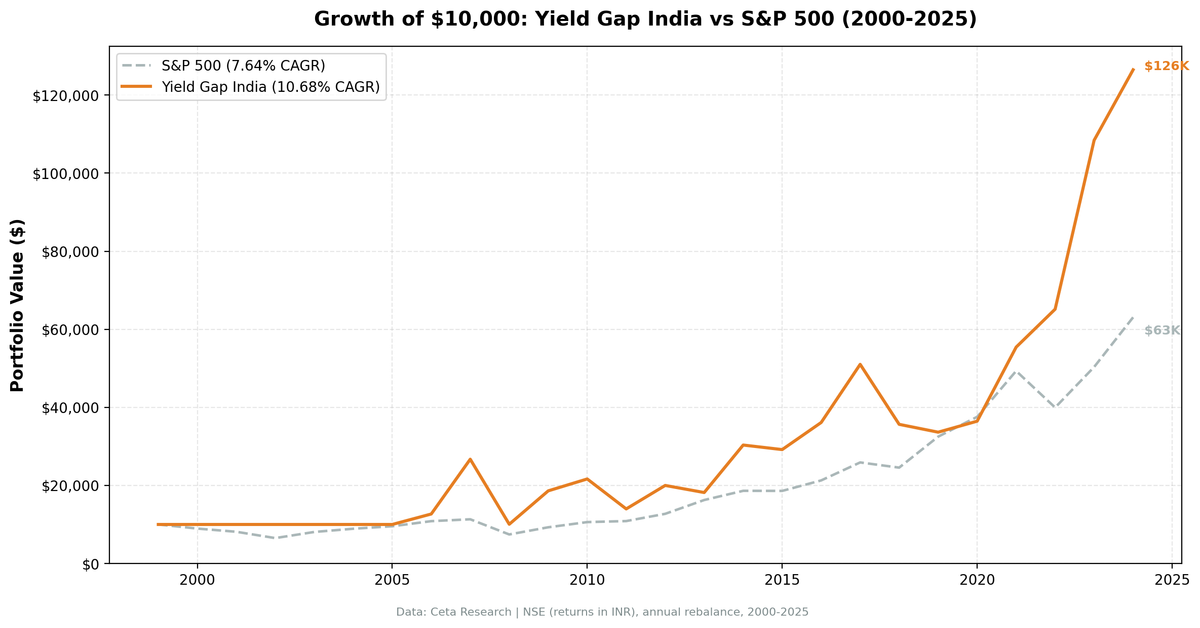

India's high risk-free rate (6.5%) sets a strict 9.5% earnings yield threshold. NSE yield gap stocks returned 10.68% CAGR vs 11.40% for Sensex — trailing the local index by 0.72% annually but beating SPY by +3.04% over 19 invested years.

title: "Yield Gap India: Strong Absolute Returns, but Sensex Leads on Local Terms (2006-2025)" slug: yield-gap-india-backtest publish_date: 2026-03-26 tags: [backtests, india-markets, value-investing, earnings-yield, NSE] post_access: public excerpt: "India's high risk-free rate (6.5%) sets a strict 9.5% earnings yield threshold. NSE yield gap stocks returned 10.68% CAGR vs 11.40% for Sensex — trailing the local index by 0.72% annually but beating SPY by +3.04% over 19 invested years." authors: [Swas] feature_image: 1_india_cumulative_growth.png feature_image_alt: "Growth of $10,000: Yield Gap India vs Sensex (2006-2025)"

Contents

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

The yield gap threshold for India is strict. With a risk-free rate of 6.5% (long-run average for Indian government bonds), the screen requires earnings yields above 9.5% — equivalent to PE ratios below roughly 10.5x. That's a demanding bar. NSE stocks that clear it have historically delivered strong absolute returns: 10.68% CAGR over 25 years including six cash years. But the Sensex itself returned 11.40% CAGR over the same period. The strategy trails the local index by 0.72% annually.

A $10,000 investment grew to $126,483 over the full 25-year period (2000-2025). Six cash years at the start (2000-2005) drag the full-period CAGR; the 19-year invested-period returns from 2006 onward are considerably higher.

The Strategy

India's high inflation and high nominal interest rates mean the risk-free rate sets a meaningful bar for equity compensation. The yield gap threshold of rfr + 3% = 9.5% EY is the highest effective threshold in our 20-market study, more than 50% above the 6% floor used in the US, UK, Germany, and Japan.

Signal: - Earnings yield > max(6%, 6.5% + 3%) = 9.5% for India (PE < ~10.5x) - Earnings yield < 50% - ROE > 8% - D/E < 2.0

Portfolio construction: Top 30 by highest earnings yield, equal weight, annual January rebalance. Cash if fewer than 10 stocks qualify. The portfolio held cash in all five years from 2000-2004 due to limited FY data coverage, then invested continuously from 2005 through 2024.

Methodology

- Universe: NSE (National Stock Exchange)

- Market cap filter: INR 50B+ at each rebalance date (~$600M USD equivalent, scaled over time)

- Data period: January 2000 through December 2025 (25 annual periods)

- Invested periods: 19 of 25 years (6 years zero-return cash, 2000-2005)

- Rebalancing: Annual (January)

- Point-in-time data: FY filings with 45-day filing lag

- Transaction costs: Size-tiered model

- Benchmark: Sensex (BSE Sensex, local Indian benchmark)

- Data source: Ceta Research FMP financial data warehouse

Data coverage note: FMP's FY earnings yield data for Indian stocks is reliable from 2006 onward on NSE. The 2000-2005 period shows zero returns — not actual portfolio performance, but a reflection of insufficient data to screen meaningful positions. The 10.68% CAGR is computed over the full 25-year period including these six zero-return years. The actual invested-period CAGR (2006-2024, 19 years) is considerably higher.

Full methodology at github.com/ceta-research/backtests/blob/main/METHODOLOGY.md.

Results

| Metric | Yield Gap India | Sensex |

|---|---|---|

| CAGR | 10.68% | 11.40% |

| Total return (25yr) | 1,164.8% | ~1,420%* |

| Max drawdown | -62.36% | -51.34% |

| Sharpe ratio | 0.109 | — |

| Down capture vs Sensex | 79.5% | — |

| Win rate vs Sensex | 52.0% | — |

| Cash periods | 6 of 25 years (24%) | — |

| Avg stocks (invested) | 25.9 | — |

*Sensex total return estimated from 11.40% CAGR.

The strategy trails Sensex by 0.72% annually and beats it in only 52% of invested years. This is the honest picture. The strategy does beat SPY (7.64% CAGR) by +3.04% over the same period, but for a domestic Indian investor, the relevant comparison is the Sensex — and the screen doesn't add meaningful alpha. The Sharpe of 0.109 is low because annual returns are extremely dispersed: +110% one year, -62% the next. The underlying market is volatile; the screen amplifies that.

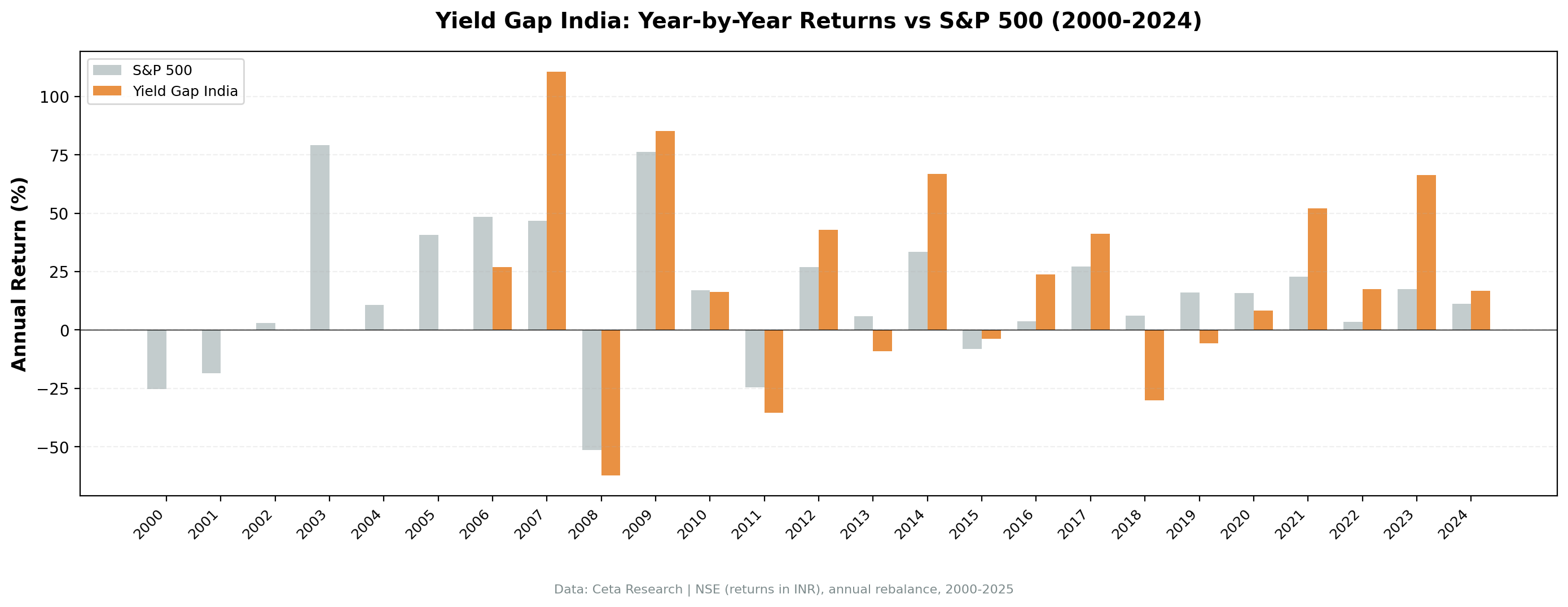

Annual returns (portfolio vs Sensex):

| Year | Portfolio | Sensex | Excess | Note |

|---|---|---|---|---|

| 2000 | 0.00% | -25.23% | +25.23% | Cash — data gap |

| 2001 | 0.00% | -18.65% | +18.65% | Cash — data gap |

| 2002 | 0.00% | +2.93% | -2.93% | Cash — data gap |

| 2003 | 0.00% | +79.09% | -79.09% | Cash — data gap |

| 2004 | 0.00% | +10.83% | -10.83% | Cash — data gap |

| 2005 | 0.00% | +40.59% | -40.59% | Cash — data gap |

| 2006 | +26.82% | +48.48% | -21.66% | First invested year |

| 2007 | +110.62% | +46.79% | +63.84% | Bull market bull run |

| 2008 | -62.36% | -51.34% | -11.02% | Worst year |

| 2009 | +85.10% | +76.32% | +8.77% | Recovery |

| 2010 | +16.37% | +17.10% | -0.73% | |

| 2011 | -35.43% | -24.53% | -10.90% | |

| 2012 | +42.99% | +27.04% | +15.95% | |

| 2013 | -9.07% | +5.96% | -15.03% | |

| 2014 | +66.90% | +33.51% | +33.39% | Modi election rally |

| 2015 | -3.83% | -8.12% | +4.29% | |

| 2016 | +23.78% | +3.79% | +19.98% | |

| 2017 | +41.24% | +27.14% | +14.10% | |

| 2018 | -30.13% | +6.15% | -36.28% | Worst relative year |

| 2019 | -5.63% | +15.98% | -21.61% | |

| 2020 | +8.38% | +15.74% | -7.36% | |

| 2021 | +52.02% | +22.85% | +29.17% | |

| 2022 | +17.55% | +3.35% | +14.20% | Best excess return |

| 2023 | +66.41% | +17.53% | +48.88% | |

| 2024 | +16.65% | +11.20% | +5.45% |

The Indian Market Story

2007 was extraordinary. The portfolio returned +110.62% vs Sensex +46.79%, a +63.84% excess. High-earnings-yield portfolios buying deeply discounted stocks tend to amplify bull markets — cheap quality companies re-rate sharply when risk appetite is high. India was in a pre-crisis equity bubble; the screen caught companies at PE ratios below 10.5x that were waiting for a catalyst.

2008 was the mirror. -62.36% in a single year, -11% worse than Sensex's -51.34%. The high-EY threshold means the portfolio holds companies with PE ratios below 10.5x — often cyclical or capital-intensive businesses that are more exposed when credit tightens and growth slows. The MDD is higher than the Sensex because the screen selects for cheap-but-exposed names.

2014 was the Modi rally. +66.90% vs Sensex +33.51% (+33.39% excess). The BJP election victory in May 2014 triggered a broad re-rating of Indian equities, but value stocks — which had underperformed for years — snapped back sharply. Companies that had been trading at single-digit multiples found buyers.

2018 was the worst relative year. -30.13% vs Sensex +6.15% (-36.28% excess). Indian value stocks sold off hard while the Sensex was carried by large-cap IT and consumer names. The 9.5% threshold keeps the portfolio in smaller, more cyclical companies that underperform in quality-flight years.

2023 showed the strategy's episodic strength. +66.41% vs Sensex +17.53% (+48.88% excess). When Indian mid-cap industrials and financials ran, the screen caught the bulk of the move. The problem is you can't know in advance which years these will be.

Run It Yourself

Current India yield gap screen:

SELECT

k.symbol,

p.companyName,

p.exchange,

p.sector,

ROUND(k.earningsYieldTTM * 100, 2) AS earnings_yield_pct,

ROUND(1.0 / NULLIF(k.earningsYieldTTM, 0), 1) AS implied_pe,

ROUND(k.returnOnEquityTTM * 100, 2) AS roe_pct,

ROUND(fr.debtToEquityRatioTTM, 2) AS debt_to_equity,

ROUND(k.freeCashFlowYieldTTM * 100, 2) AS fcf_yield_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM key_metrics_ttm k

JOIN profile p ON k.symbol = p.symbol

JOIN financial_ratios_ttm fr ON k.symbol = fr.symbol

WHERE k.earningsYieldTTM > 0.095 -- EY > 9.5% (rfr=6.5%+3%)

AND k.earningsYieldTTM < 0.50

AND k.returnOnEquityTTM > 0.08

AND (fr.debtToEquityRatioTTM IS NULL

OR (fr.debtToEquityRatioTTM >= 0 AND fr.debtToEquityRatioTTM < 2.0))

AND k.marketCap > 50000000000 -- INR 50B+

AND (p.industry IS NULL OR p.industry NOT LIKE 'Asset Management%')

AND (p.industry IS NULL OR p.industry NOT LIKE 'Shell Companies%')

AND p.exchange IN ('NSE')

ORDER BY k.earningsYieldTTM DESC

LIMIT 30

Run this query on Ceta Research Data Explorer

Full backtest:

git clone https://github.com/ceta-research/backtests.git

cd backtests

pip install -r requirements.txt

python3 yield-gap/backtest.py --preset india --output results.json --verbose

Limitations

Underperforms Sensex: The strategy returned 10.68% CAGR vs Sensex's 11.40% — a -0.72% excess over 25 years. For an Indian investor who can simply buy a Sensex ETF, this screen doesn't add alpha. It does beat SPY (7.64%) for a global capital allocation framing, but that comparison is less relevant for domestic Indian investors.

Data gap (2000-2005): FMP's FY earnings yield data for NSE stocks is not reliably available before 2006. The backtest holds cash for six years. The 10.68% CAGR includes six zero-return years; the invested-period CAGR (2006-2024, 19 years) is considerably higher.

High volatility: -62.36% drawdown in 2008 and +110.62% in 2007 reflect the asset class. The strategy amplifies India's inherent volatility by concentrating in the cheapest, often most cyclical companies.

Currency risk: Returns in INR. INR has depreciated against USD approximately 3-4% annually over this period. USD-based investors would have experienced lower USD returns.

Threshold sensitivity: The 9.5% EY threshold is derived from a 6.5% risk-free rate assumption. India's actual policy rate has ranged from 4% to 9% over this period. A lower effective RFR would lower the threshold and widen the qualifying universe; a higher RFR would narrow it further.

Data: Ceta Research (FMP financial data warehouse), January 2000 through December 2025. Full methodology: github.com/ceta-research/backtests/blob/main/METHODOLOGY.md.

Academic references: Campbell, J.Y. & Vuolteenaho, T. (2004). "Bad Beta, Good Beta." American Economic Review, 94(5). Damodaran, A. (2012). "Equity Risk Premiums (ERP): Determinants, Estimation and Implications." Stern School of Business.

Past performance does not guarantee future results. This is educational content, not investment advice.