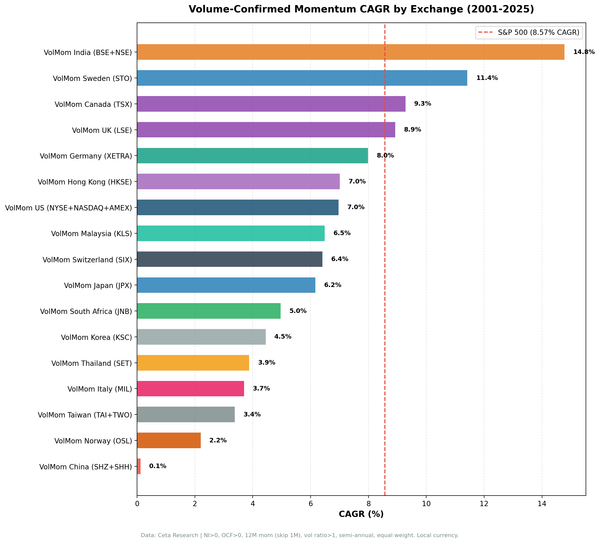

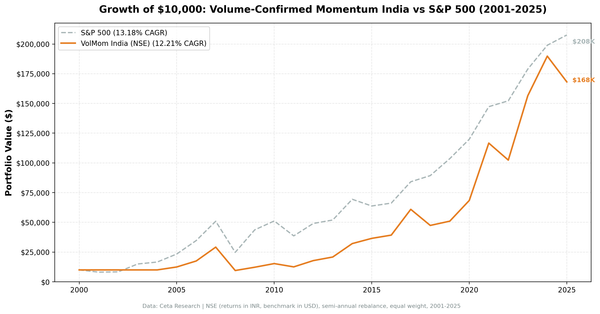

momentum investing

Volume-Confirmed Momentum on India Stocks: 12.21% CAGR, But the Sensex Did Better

Volume-confirmed momentum on Indian equities from 2001 to 2025: 12.21% CAGR with 70.6% down capture. Strong absolute returns, but the Sensex returned 13.18% over the same period. The factor provides downside protection but doesn't beat the index.