Volume-Confirmed Momentum Across 17 Markets: +7.34% in Sweden, -0.97% in India

Same strategy, 17 global exchanges, 25 years. Volume-confirmed momentum returned +7.34% excess vs OMX Stockholm 30, +6.0% vs FTSE 100, but -0.97% vs Sensex in India and -0.92% vs S&P 500 in the US. The factor works where institutional volume is informative — and fails where it's noise.

Same signal, 17 markets, 25 years. Volume-confirmed momentum — rising 3-month volume, skip-last-month momentum, basic quality filters — returned +7.34% excess annually in Sweden, +6.0% in the UK, +5.12% in Hong Kong, and +4.59% in Switzerland when measured against local benchmarks. It returned -0.92% in the US and -0.97% in India — where the strategy appears strong against SPY but actually underperforms the Sensex. The difference isn't the strategy. It's the benchmark.

Contents

- Method

- What We Found

- The Market Structure Argument

- Backtest Methodology

- Limitations

- Takeaway

- Part of a Series

- References

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

| Parameter | Value |

|---|---|

| Universe | 17 global exchanges |

| Rebalancing | Semi-annual (January, July) |

| Signal | 12-month return, skip last month (T-1M to T-12M) |

| Volume filter | 3-month avg daily volume > 12-month avg (vol_ratio > 1.0) |

| Quality filter | netIncome > 0 AND operatingCashFlow > 0 (FY, 45-day lag) |

| Selection | Top 30 by momentum, equal weight |

| Min threshold | 10 qualifying stocks to deploy capital |

| Data source | FMP via Ceta Research warehouse |

| Benchmark | Local currency index for each exchange (see table) |

| Period | 2001–2025 |

| Academic basis | Lee & Swaminathan (2000), Journal of Finance 55(5) |

The same backtest code ran on every exchange. No parameter tuning per market. Market cap thresholds scale to local market size. Everything else is identical.

Important note on benchmarks. Earlier runs compared all exchanges against SPY. That comparison is useful for a global investor allocating capital, but it obscures how the strategy performs against what a local investor would actually use. For example, India appeared to produce +6.21% annual excess vs SPY — but vs the Sensex, the strategy underperforms by 0.97%. This update uses local benchmarks throughout. The SPY comparison is noted where it materially differs.

What We Found

Volume confirmation produces alpha where institutional investors dominate trading. It destroys alpha where retail, algorithmic, and ETF flows dominate volume. And critically, some markets that looked weak vs SPY perform well vs their local benchmarks — because the local index itself underperformed SPY.

Full results across 17 exchanges:

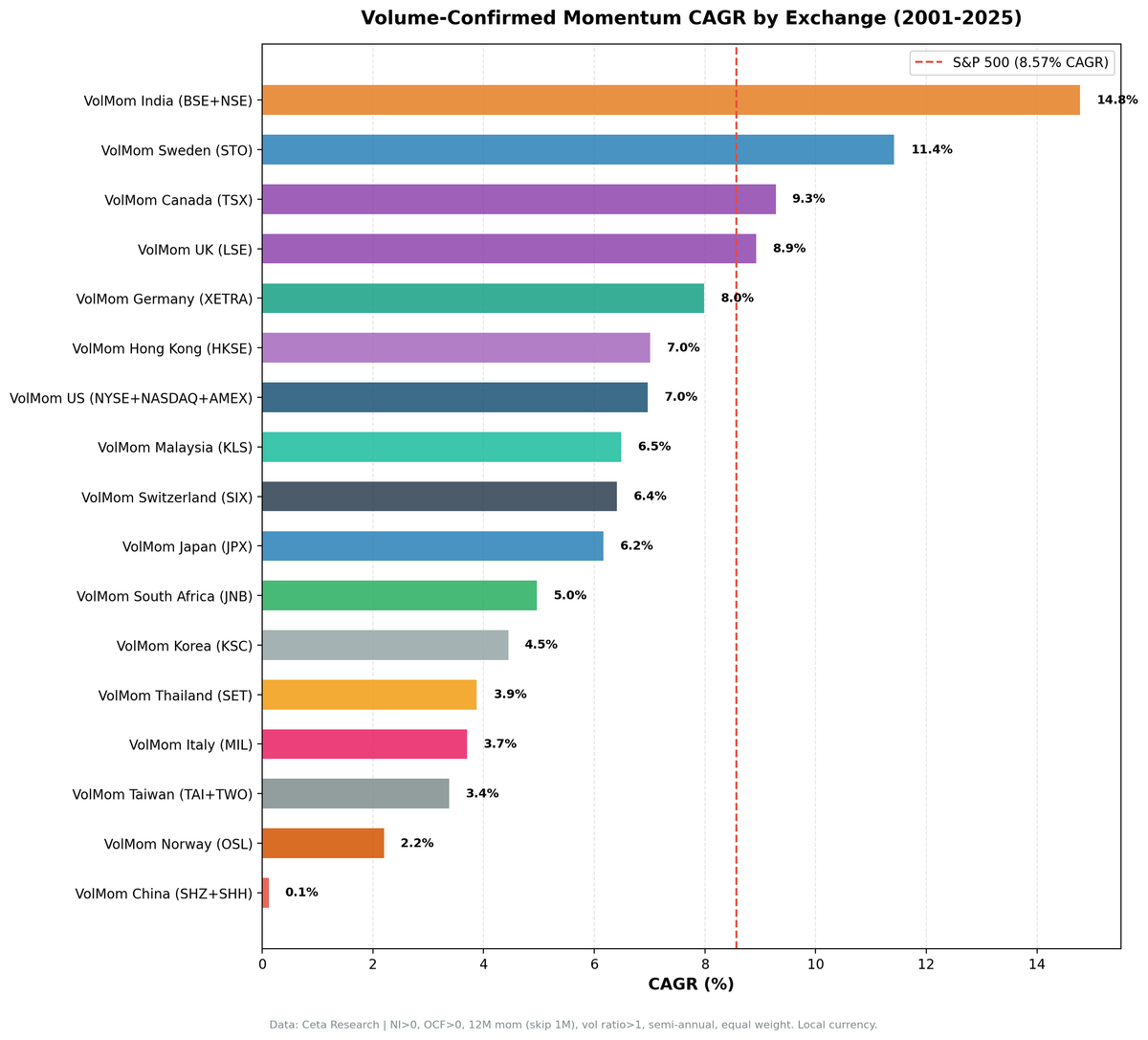

| Exchange | CAGR | Local Benchmark | Benchmark CAGR | Excess (local) | Sharpe | Max DD | Down Capture | Cash% |

|---|---|---|---|---|---|---|---|---|

| STO (Sweden) | 11.02% | OMX Stockholm 30 | 3.68% | +7.34% | 0.487 | -38.44% | 34.8% | 29% |

| LSE (UK) | 7.44% | FTSE 100 | 1.44% | +6.00% | 0.180 | -51.37% | 80.2% | 2% |

| HKSE (Hong Kong) | 7.13% | Hang Seng | 2.01% | +5.12% | 0.146 | -54.81% | 69.4% | 8% |

| SIX (Switzerland) | 6.19% | SMI | 1.60% | +4.59% | 0.378 | -29.92% | 56.3% | 27% |

| TSX (Canada) | 9.25% | TSX Composite | 4.75% | +4.49% | 0.428 | -37.58% | 32.4% | 4% |

| BSE_NSE (India) | 12.21% | Sensex | 13.18% | -0.97% | 0.213 | -67.44% | 70.6% | 20% |

| NYSE/NASDAQ/AMEX (US) | 7.66% | S&P 500 | 8.59% | -0.92% | 0.235 | -58.52% | 148.3% | 0% |

| XETRA (Germany) | 8.61% | DAX | 5.58% | +3.03% | 0.338 | -41.82% | 60.1% | 6% |

| JPX (Japan) | 5.77% | Nikkei 225 | 4.45% | +1.32% | 0.245 | -57.35% | 87.6% | 4% |

| KSC (Korea) | 4.15% | KOSPI | 7.52% | -3.37% | 0.061 | -37.96% | 58.3% | 31% |

| TAI_TWO (Taiwan) | 3.31% | TAIEX | 6.40% | -3.09% | 0.110 | -49.14% | 95.8% | 31% |

| SET (Thailand) | 3.98% | SET Index | 5.98% | -2.00% | 0.100 | -28.78% | 41.7% | 33% |

| KLS (Malaysia) | 6.19% | S&P 500† | 8.59% | -2.39% | 0.309 | -20.63% | 39.9% | 31% |

| SHZ_SHH (China) | -0.74% | SSE Composite | 2.05% | -2.79% | -0.088 | -69.26% | 90.9% | 8% |

| MIL (Italy) | 3.67% | S&P 500† | 8.59% | -4.91% | 0.043 | -36.14% | 83.5% | 41% |

| JNB (S. Africa) | 2.61% | S&P 500† | 8.59% | -5.98% | -0.375 | -37.48% | 40.5% | 55% |

| OSL (Norway) | 4.45% | Oslo All Share | 11.20% | -6.74% | 0.128 | -19.24% | — | 82%* |

†No local benchmark available in FMP — SPY used as fallback. *Norway result unreliable: Oslo All Share data begins 2013, reducing the analysis to 12 years.

The pattern is clear when using local benchmarks. Markets where the local index underperformed (Sweden, UK, Hong Kong, Switzerland) look like alpha generators. Markets where the local index performed strongly (India, Korea, Norway) expose the factor's limitations. The institutional-volume story still holds — but the data requires honest benchmark selection.

Markets where local benchmarks changed the narrative significantly: - India: appeared +6.21% vs SPY; is -0.97% vs Sensex. The factor doesn't beat the home index. - UK: appeared +0.37% vs SPY; is +6.00% vs FTSE 100. The FTSE had essentially flat returns (1.44% CAGR). - Germany: appeared -0.58% vs SPY; is +3.03% vs DAX. The DAX underperformed SPY significantly. - Switzerland: appeared -2.16% vs SPY; is +4.59% vs SMI. The SMI returned only 1.60% CAGR.

The Market Structure Argument

The Lee & Swaminathan (2000) paper argued that rising volume on a momentum stock signals institutional accumulation — sustained buying that pushes prices further in the direction of the trend. The logic holds when volume is informative.

Sweden. The Stockholm exchange has the lowest retail participation rate of any major market we tested. Institutional investors — pension funds, insurance companies, sovereign funds — dominate daily flow. Volume confirmation produced the highest Sharpe ratio (0.487) of any exchange. When Swedish institutions buy with conviction, the signal has historically predicted continued outperformance.

Switzerland. The SMI is a quality index dominated by three mega-caps (Nestle, Novartis, Roche). The broader Swiss market below the mega-caps sees genuine institutional rotation. When volume rises on a Swiss mid-cap above its 12-month average, it reflects real accumulation. Sharpe of 0.378 with 56.3% down capture.

Canada. TSX is dominated by institutional trading in natural resources. Volume confirmation produced +4.49% excess with 32.4% down capture — the lowest crash exposure of any exchange in the study.

India: the exception. Despite the academic case for volume signals in emerging markets with rising institutional participation, the strategy underperformed the Sensex by 0.97% annually. The high absolute return (12.21% CAGR) reflects India's structural growth. The volume filter didn't add to that. The 2009 recovery (+76.3% Sensex) while the strategy held +29.1% explains much of the shortfall.

China: the clearest failure. The A-share market returned -0.74% CAGR over 24.5 years (vs SSE Composite +2.05%). China has the highest retail participation rate of any major exchange. Volume on Chinese A-shares frequently reflects retail FOMO cycles, not institutional conviction.

The US: efficient market kills the signal. At 0% cash rate and 148.3% down capture, the US strategy is always invested and crashes hardest. ETF rebalancing, options market maker hedging, and high-frequency trading generate enormous volume in US stocks with no directional view.

Norway and South Africa results are unreliable. With 82% and 55% cash rates respectively, there aren't enough invested periods to draw meaningful conclusions. The Norway result covers only 12 years due to Oslo All Share data availability.

Backtest Methodology

- Data: FMP financial data via Ceta Research warehouse. Price data from

stock_eod(adjusted closes). - Point-in-time: Quality filters use annual FY filings with 45-day reporting lag. No look-ahead bias.

- Signal: Price at T-12M to T-1M. Skip last month avoids short-term reversal contamination per Jegadeesh & Titman (1993).

- Volume ratio: 63-day avg daily volume divided by 252-day avg daily volume, computed at each rebalance date.

- Data quality: Stocks with adjusted close < $1 at either lookback date excluded. Portfolio momentum capped at 200% per stock.

- Equal weight: 30 positions, 3.33% each. No intraperiod rebalancing.

- Transaction costs: Modeled as size-tiered commissions. See methodology.

- Execution: Next-day close (MOC model). Entry prices use the trading day after the rebalance signal date.

- Benchmarks: Local currency indexes where available. SPY used for Malaysia, Italy, South Africa (no local index data).

- Global count query: View qualifying stocks globally

Limitations

Survivorship bias. The FMP dataset includes many delisted companies, but coverage isn't uniform across all 17 exchanges. Emerging market and smaller exchange data may under-represent companies that failed. This biases results upward.

Institutional participation proxied by results. We don't directly measure retail vs. institutional trading composition. The "market structure" argument is inferred from where the strategy works and where it fails — plausible but not a controlled experiment.

Currency effects excluded. All returns are in local currency. An investor running this strategy globally faces FX risk not captured in individual exchange numbers.

Local indexes have different return profiles. The FTSE 100 (1.44% CAGR), SMI (1.60%), and OMX Stockholm 30 (3.68%) all underperformed SPY massively over 2001-2025. A global investor comparing against SPY would see a less favorable picture for those exchanges.

Semi-annual rebalancing. Momentum signals decay faster than six months. The strategy carries stale signals through much of each holding period.

Takeaway

Volume confirmation is a market-structure factor. It adds alpha where volume is informative, and destroys alpha where volume is noise. The benchmark selection matters enormously: exchanges where the local index underperformed (Sweden, UK, Switzerland) show strong apparent alpha that's partly an artifact of comparing against a weak benchmark.

The exchanges with genuine volume momentum alpha across both local and global comparisons: Sweden (OMX 3.68% → +7.34% excess; SPY 8.59% → +2.43% excess) and Canada (TSX 4.75% → +4.49% excess; SPY 8.59% → +0.66% excess).

The US and India — the two most-discussed markets — both underperform their respective benchmarks. The US down capture of 148.3% is the worst risk feature of any developed-market exchange in the study.

Part of a Series

This is part of a multi-exchange volume-confirmed momentum study:

- Volume-Confirmed Momentum: US Stocks

- Volume-Confirmed Momentum: India

- Volume-Confirmed Momentum: Canada

- Volume-Confirmed Momentum: Sweden

- Volume-Confirmed Momentum: Germany

- Volume-Confirmed Momentum: 17-Exchange Comparison

References

- Lee, C. & Swaminathan, B. (2000). Price Momentum and Trading Volume. Journal of Finance, 55(5), 2017-2069.

- Jegadeesh, N. & Titman, S. (1993). Returns to Buying Winners and Selling Losers. Journal of Finance, 48(1), 65-91.

- Daniel, K. & Moskowitz, T. (2016). Momentum Crashes. Journal of Financial Economics.

Past performance does not guarantee future results. This is educational content, not investment advice.