EV/EBITDA Sector Discount on US Stocks: 25 Years of Data

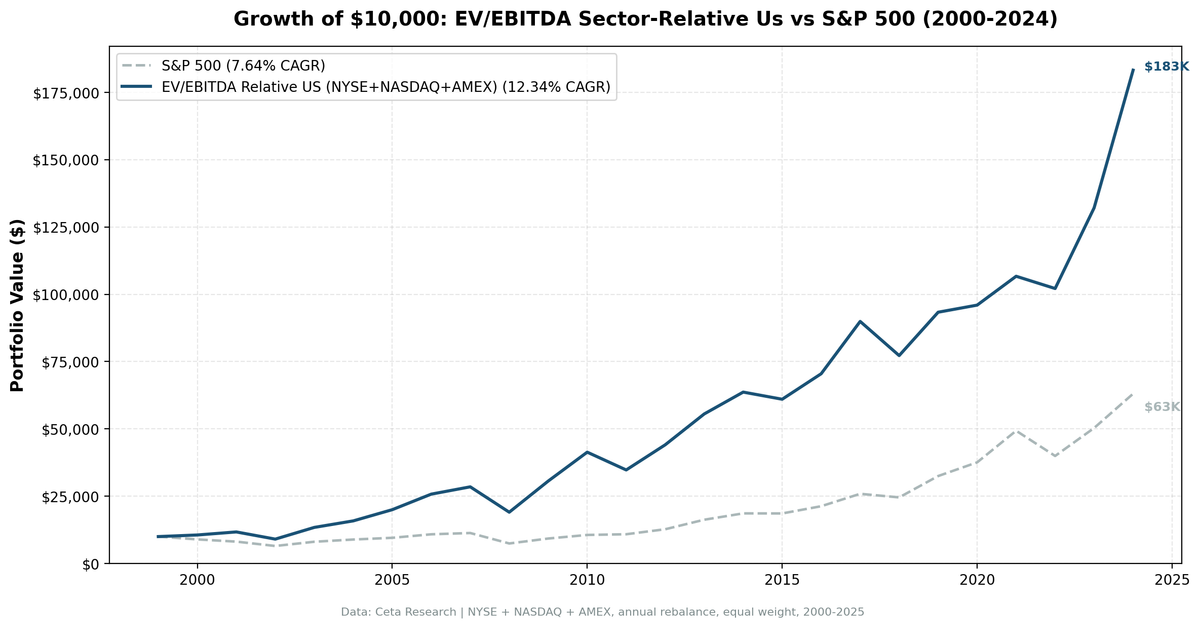

When a profitable company trades at a 30% discount to its sector peers on EV/EBITDA, something tends to happen. Either the business is genuinely broken, or the market has mispriced it. We built a screen to find the latter, ran it on 25 years of US stock data, and the results are hard to ignore: 12.34% CAGR vs 7.64% for SPY, with down capture of just 62.9%.

Contents

- Method

- The Screen

- What We Found

- Annual Returns

- The Early 2000s: Where the Gap Was Built

- Crisis Comparison

- The Growth Regime Problem: 2019-2021

- Limitations

- Conclusion

That's the short version. Here's the full picture.

Method

We screened NYSE, NASDAQ, and AMEX stocks from 2000 through 2025. Each January, we computed sector median EV/EBITDA and selected the 30 stocks trading at the deepest discount to their peers. We held for 12 months, then reset.

| Parameter | Value |

|---|---|

| Universe | NYSE + NASDAQ + AMEX |

| Market cap minimum | $1B USD |

| EV/EBITDA range | 0.5x to 25x |

| ROE filter | > 8% |

| D/E filter | < 2.0 |

| Sector discount required | ≥ 30% below sector median |

| Selection | Top 30 by deepest discount |

| Rebalancing | Annual (January) |

| Cash condition | If fewer than 10 qualify |

| Data source | Ceta Research (FMP financial data warehouse) |

| Filing lag | 45 days (point-in-time, avoids look-ahead) |

| Period | 2000-2025 (25 years) |

| Benchmark | SPY (S&P 500 Total Return) |

Why EV/EBITDA instead of P/E?

P/E breaks in two situations: when companies carry heavy debt (earnings are depressed by interest), and when depreciation policies differ across firms. EV/EBITDA captures the full enterprise value against operating earnings before financing and accounting choices distort the picture. It's a cleaner signal for cross-company comparison, especially across capital-intensive sectors like energy and industrials where P/E becomes unreliable.

Why sector-relative?

A tech stock at 8x EV/EBITDA isn't the same as a utility at 8x. Technology companies typically trade at higher multiples because their growth profiles justify it. Comparing a tech name against the whole-market median creates false positives. By measuring discount relative to sector peers, we ask a narrower question: is this company unusually cheap compared to others doing similar things? The sector-relative approach adapts to prevailing valuation regimes. When tech runs hot at 30x, a name at 18x looks cheap. When industrials trade at 9x, an 8x name barely registers. The screen filters for genuine relative value rather than absolute level.

The academic foundation for this approach comes from Loughran and Wellman (2011), who showed EV/EBITDA predicts cross-sectional returns, and the sector-relative framing extends that by controlling for industry-level effects.

The Screen

Here's the current EV/EBITDA sector-relative screen running against the live warehouse. It finds profitable US companies trading at 30%+ below their sector median, with quality filters to exclude distressed names.

WITH universe AS (

SELECT k.symbol, p.companyName, p.exchange, p.sector,

k.evToEBITDATTM AS ev_ebitda, k.returnOnEquityTTM AS roe,

fr.debtToEquityRatioTTM AS de, k.marketCap

FROM key_metrics_ttm k

JOIN financial_ratios_ttm fr ON k.symbol = fr.symbol

JOIN profile p ON k.symbol = p.symbol

WHERE k.evToEBITDATTM BETWEEN 0.5 AND 25

AND k.returnOnEquityTTM > 0.08

AND (fr.debtToEquityRatioTTM IS NULL OR (fr.debtToEquityRatioTTM >= 0 AND fr.debtToEquityRatioTTM < 2.0))

AND k.marketCap > 1000000000

AND p.sector IS NOT NULL

AND p.exchange IN ('NYSE', 'NASDAQ', 'AMEX')

),

sector_medians AS (

SELECT exchange, sector,

PERCENTILE_CONT(0.5) WITHIN GROUP (ORDER BY ev_ebitda) AS median_ev_ebitda,

COUNT(*) AS n_sector_stocks

FROM universe GROUP BY exchange, sector HAVING COUNT(*) >= 5

)

SELECT u.symbol, u.companyName, u.exchange, u.sector,

ROUND(u.ev_ebitda, 2) AS ev_ebitda_ttm,

ROUND(sm.median_ev_ebitda, 2) AS sector_median_ev_ebitda,

ROUND(u.ev_ebitda / sm.median_ev_ebitda, 3) AS ev_ratio_to_sector,

ROUND((1 - u.ev_ebitda / sm.median_ev_ebitda) * 100, 1) AS discount_pct,

ROUND(u.roe * 100, 1) AS roe_pct,

ROUND(u.de, 2) AS debt_to_equity,

ROUND(u.marketCap / 1e9, 2) AS mktcap_b

FROM universe u JOIN sector_medians sm ON u.exchange = sm.exchange AND u.sector = sm.sector

WHERE u.ev_ebitda / sm.median_ev_ebitda < 0.70

ORDER BY u.ev_ebitda / sm.median_ev_ebitda ASC LIMIT 30

Run this query on the live data: cetaresearch.com/data-explorer?q=BirLYENzA8

What We Found

The headline number is 12.34% annualized over 25 years, turning $10,000 into $183,000. SPY returned 7.64% annualized over the same period, turning $10,000 into $63,000. The strategy held cash zero times across all 25 years. There was always a qualifying cohort.

| Metric | Strategy | SPY |

|---|---|---|

| CAGR | 12.34% | 7.64% |

| Excess return | +4.69% | — |

| Total return | 1,732.94% | 530.71% |

| Sharpe ratio | 0.468 | — |

| Sortino ratio | 1.033 | — |

| Calmar ratio | 0.373 | — |

| Max drawdown | -33.09% | -34.90% |

| Down capture | 62.91% | 100% |

| Up capture | 129.98% | 100% |

| Win rate | 68% | — |

| Cash periods | 0 / 25 | — |

| Avg stocks held | 21.9 | — |

The down capture of 62.9% is the statistic we keep coming back to. When SPY drops 10%, this portfolio drops roughly 6.3%. Over 25 years with multiple market crises, that asymmetry compounds. You capture 130% of the upside and absorb only 63% of the downside on average. That combination produces a much smoother wealth trajectory.

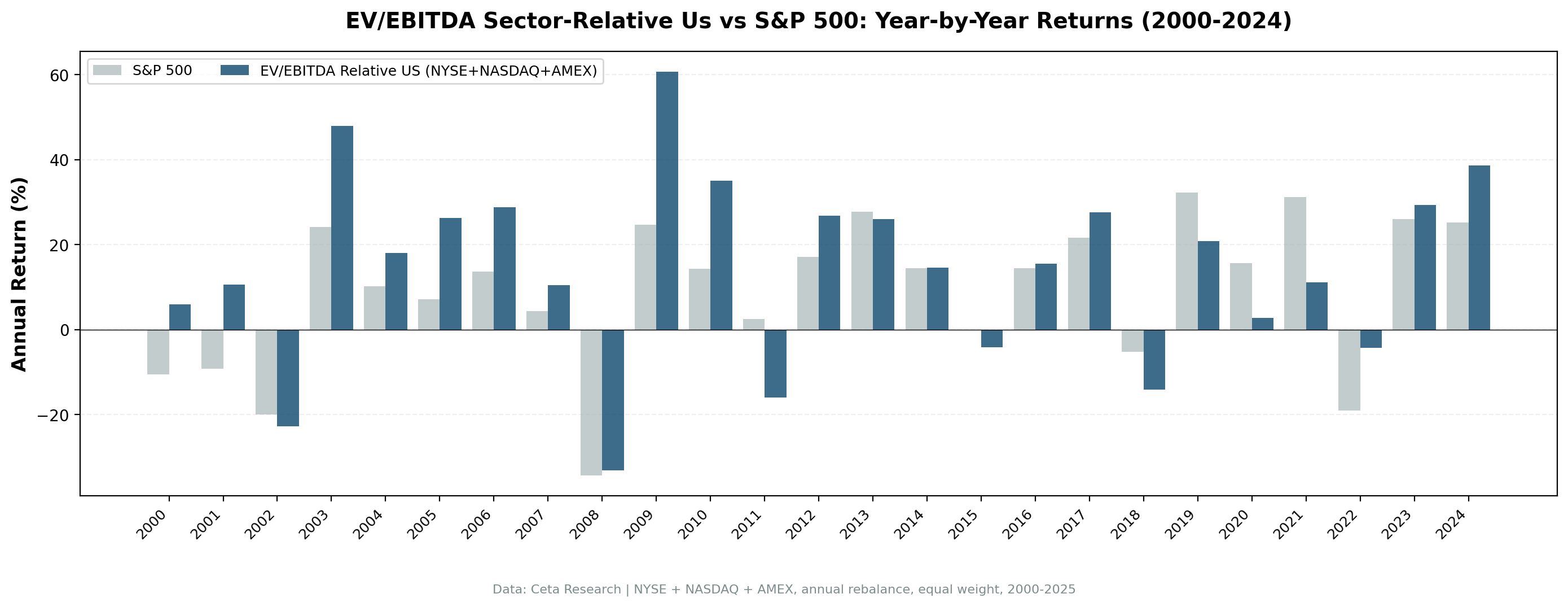

Annual Returns

| Year | Strategy | SPY | Excess |

|---|---|---|---|

| 2000 | +6.0% | -10.5% | +16.4% |

| 2001 | +10.7% | -9.2% | +19.9% |

| 2002 | -22.8% | -19.9% | -2.8% |

| 2003 | +48.0% | +24.1% | +23.9% |

| 2004 | +18.1% | +10.2% | +7.9% |

| 2005 | +26.3% | +7.2% | +19.1% |

| 2006 | +28.9% | +13.7% | +15.2% |

| 2007 | +10.5% | +4.4% | +6.1% |

| 2008 | -33.1% | -34.3% | +1.2% |

| 2009 | +60.7% | +24.7% | +36.0% |

| 2010 | +35.0% | +14.3% | +20.7% |

| 2011 | -16.0% | +2.5% | -18.4% |

| 2012 | +26.9% | +17.1% | +9.8% |

| 2013 | +26.0% | +27.8% | -1.8% |

| 2014 | +14.6% | +14.5% | +0.1% |

| 2015 | -4.2% | -0.1% | -4.0% |

| 2016 | +15.5% | +14.4% | +1.1% |

| 2017 | +27.6% | +21.6% | +5.9% |

| 2018 | -14.1% | -5.2% | -9.0% |

| 2019 | +20.9% | +32.3% | -11.4% |

| 2020 | +2.8% | +15.6% | -12.8% |

| 2021 | +11.2% | +31.3% | -20.1% |

| 2022 | -4.3% | -19.0% | +14.7% |

| 2023 | +29.3% | +26.0% | +3.3% |

| 2024 | +38.7% | +25.3% | +13.4% |

The Early 2000s: Where the Gap Was Built

The strategy's biggest structural advantage appeared in the dot-com bust. In 2000 and 2001, when SPY fell 10.5% and 9.2% respectively, this screen returned +6.0% and +10.7%. The sector-relative signal naturally avoided the frothy tech and telecom names because those stocks weren't cheap relative to sector peers. They were the sector peers, trading at the high end of their cohorts.

Value names in industrials, financials, and consumer sectors absorbed almost none of the growth selloff. Then came the recovery: 2003 brought +48.0% against SPY's +24.1%, and 2005-2006 extended the outperformance to +19.1% and +15.2% in excess.

That 2000-2010 decade was exceptional for this type of strategy. The market repeatedly repriced speculative assets downward while mean-reverting the genuinely undervalued.

Crisis Comparison

| Event | Strategy | SPY | Excess |

|---|---|---|---|

| Dot-com bust (2000-2002) | -9.7% cumulative | -34.2% cumulative | +24.5% |

| GFC 2008 | -33.1% | -34.3% | +1.2% |

| COVID crash (2020) | +2.8% | +15.6% | -12.8% |

| Rate shock 2022 | -4.3% | -19.0% | +14.7% |

The GFC is telling. In 2008, the strategy fell -33.1% versus SPY's -34.3%. Essentially no protection in a systemic, liquidity-driven crisis where all assets sold off simultaneously. The sector-relative discount couldn't defend against forced selling when correlation goes to one.

Compare that to 2022, when the rate-shock selloff was valuation-driven rather than systemic. The strategy fell -4.3% while SPY fell -19.0%. The companies in this screen, already cheap on EV/EBITDA, had less air to come out of valuations during a repricing regime.

The Growth Regime Problem: 2019-2021

The three years from 2019 to 2021 produced the worst sustained underperformance. The strategy returned +20.9%, +2.8%, and +11.2% against SPY's +32.3%, +15.6%, and +31.3%. In aggregate, that's 57 percentage points of missed upside over three years.

This is the value trap risk: when growth stocks lead and narrow leadership drives index performance, a sector-relative value screen sits out the party. The names passing the EV/EBITDA filter in those years were disproportionately in sectors that lagged, while the mega-cap tech names inflating SPY never qualified.

The strategy recovered sharply. 2022 (+14.7% excess), 2023 (+3.3% excess), and 2024 (+13.4% excess) show the screen reasserting itself when valuation started mattering again.

Limitations

Concentration risk. Averaging 21.9 stocks over 25 years means some individual company blowups can hit hard. The screen's quality filters (ROE > 8%, D/E < 2.0) reduce but don't eliminate this.

Sector concentration. In some years, the discount signal clusters in one or two sectors. You can end up with a portfolio that's effectively a sector bet, not a diversified value screen.

Systemic crashes aren't protected. 2008 demonstrates the ceiling on downside protection. When credit markets freeze and forced selling dominates, EV/EBITDA relationships temporarily stop mattering. Down capture of 62.9% is a long-run average, not a guarantee in any specific crisis.

Execution costs. Annual rebalancing on 21-30 positions is low-cost in theory, but mid-cap and small-cap names in this screen may have wider bid-ask spreads than the index. The backtest doesn't model transaction costs.

Growth regime risk. Three consecutive years of underperformance (2019-2021) require conviction in the strategy's long-run validity. Many investors would capitulate at year two.

Filing lag. We apply a 45-day filing lag to avoid look-ahead bias, but real-world data latency, restatements, and revisions add noise that backtests can't fully capture.

Conclusion

A sector-relative EV/EBITDA screen on US stocks produced 12.34% annualized over 25 years, more than 4.5 percentage points above SPY, with meaningful downside protection (62.9% down capture) and zero cash periods. The mechanism is straightforward: companies that are cheap relative to sector peers on EV/EBITDA tend to mean-revert.

The honest caveats are equally clear. Systemic crises offer limited protection. Growth regime years punish the screen. And the approach requires patience through multi-year underperformance.

The strength of this screen isn't that it avoids drawdowns. It's that the upside captures more than the downside gives back, and it does so consistently across 25 years of varying market conditions.

What's your experience running sector-relative value screens? Do you adjust for sector weighting or just take the top-30 list straight?

Part of a Series: Sweden | Global | UK | Switzerland | Japan | India | Hong Kong | Germany

Data: Ceta Research (FMP financial data warehouse). Backtest covers 2000-2025 using point-in-time financial data with 45-day filing lag. Results are hypothetical and don't reflect actual investment results. Past performance doesn't guarantee future results.