Low Volatility Quality on Taiwan Stocks: +2.3% vs TAIEX Over 25 Years

We backtested low-vol quality stocks on the Taiwan Stock Exchange (TAI) from 2000 to 2025. The portfolio returned 6.65% CAGR with a 0.422 Sharpe ratio, beating the TAIEX by +2.28% annually. Down capture of 29.0% and a beta of 0.317 in a market dominated by TSMC and semiconductors. The...

Taiwan's stock market is dominated by semiconductors. TSMC alone accounts for a massive share of total market cap, and hundreds of listed companies sit in its supply chain: foundries, packaging, testing, equipment, materials. This is a high-beta, export-driven market that moves with the global tech cycle.

Contents

- Method

- The Screen

- Results

- Cash Periods

- When It Works

- When It Struggles

- Why Taiwan's Low-Vol Profile Is Unusual

- Limitations

- Part of a Series

- Run It Yourself

- Takeaway

- References

That makes it an interesting test for low-volatility quality. If the strategy works here, it's doing something genuinely useful: finding the non-cyclical corner of a cyclical market. Over 25 years, the screen returned 6.65% CAGR with a 0.422 Sharpe ratio, beating the TAIEX by +2.28% annually. It captured only 29% of market downside while participating in 53% of upside. The portfolio went to cash in 20% of periods, reflecting how few Taiwanese stocks pass both quality and low-vol filters simultaneously.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Data source: Ceta Research (FMP financial data warehouse, 70K+ global stocks) Universe: All stocks on the Taiwan Stock Exchange (TAI) with market cap > NT$10B (~$312M USD) Period: January 2000 to March 2025 (25.8 years, 103 quarterly periods) Rebalancing: Quarterly (January, April, July, October) Benchmark: Taiwan Stock Exchange Capitalization Weighted Stock Index (TAIEX) Execution: Next-day close (MOC) Cash rule: Portfolio holds cash if fewer than 10 stocks qualify Transaction costs: Size-tiered model (0.1% for large caps, 0.3% for mid caps, 0.5% for small caps) Data quality guards: 45-day lag on annual filings, minimum 200 trading days for vol computation, max single return capped at 200%, penny stocks excluded

Signal filters:

| Filter | Threshold | Source |

|---|---|---|

| Return on equity | > 10% | key_metrics FY |

| Operating profit margin | > 10% | financial_ratios FY |

| Market cap | > NT$10B (~$312M USD) | key_metrics FY |

| 252-day realized volatility | Rank ASC, top 30 | stock_eod daily returns |

| Minimum trading days | >= 200 in 14-month window | stock_eod |

The Screen

SELECT

k.symbol,

p.companyName,

ROUND(k.returnOnEquityTTM * 100, 2) AS roe_pct,

ROUND(f.operatingProfitMarginTTM * 100, 2) AS opm_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM key_metrics_ttm k

JOIN financial_ratios_ttm f ON k.symbol = f.symbol

JOIN profile p ON k.symbol = p.symbol

WHERE k.returnOnEquityTTM > 0.10

AND f.operatingProfitMarginTTM > 0.10

AND k.marketCap > 312000000

AND p.exchange = 'TAI'

ORDER BY k.marketCap DESC

LIMIT 30

This produces the quality universe. The full strategy then ranks these candidates by trailing 252-day realized volatility (computed from daily returns) and selects the 30 lowest-volatility names.

Try the quality screen on Ceta Research

Results

| Metric | Low Vol + Quality | TAIEX |

|---|---|---|

| CAGR | 6.65% | 4.38% |

| Total Return | 424.97% | 188.84% |

| Max Drawdown | -44.68% | -53.74% |

| Annualized Volatility | 13.38% | 23.56% |

| Sharpe Ratio | 0.422 | 0.127 |

| Sortino Ratio | 0.692 | 0.193 |

| Calmar Ratio | 0.149 | 0.082 |

| VaR (95%) | -10.68% | -23.26% |

| Beta | 0.317 | 1.0 |

| Alpha | 4.58% | -- |

| Up Capture | 53.26% | -- |

| Down Capture | 29.01% | -- |

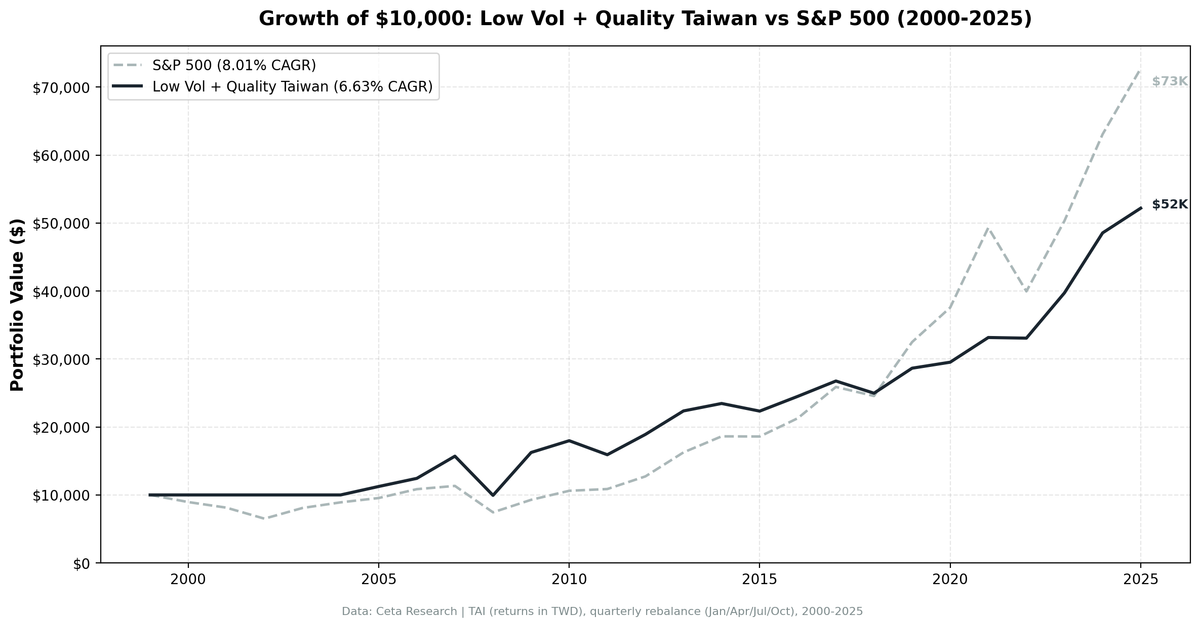

$10,000 invested in 2000 grew to $52,497 in the low-vol quality portfolio vs $28,884 in the TAIEX.

The Sharpe ratio tells the story. At 0.422, Taiwan's low-vol quality screen massively outperforms the TAIEX's 0.127. The Sortino ratio is even more striking: 0.692 vs 0.193, meaning the portfolio's downside volatility is proportionally much lower than its total volatility. It captures 53% of market upside but only 29% of downside. That asymmetry, persistent across 25 years, is the core value proposition.

The beta of 0.317 is notable in a market known for high-beta semiconductor stocks. The strategy effectively builds a portfolio that behaves like one-third the market's risk but keeps most of the quality exposure.

Cash Periods

The portfolio went to cash in 21 of 103 quarters (20%). Taiwan's market is smaller than the US, Japan, or India. When tech cycles drive volatility up across most listed companies, there simply aren't 10 stocks that pass both quality and low-vol filters. This isn't a flaw. The strategy is doing what it should: refusing to own stocks when the low-vol universe is too thin.

Average stocks held when invested: 28.3 out of a maximum 30.

When It Works

The strategy's best years come when Taiwan's broad market falls or stagnates, and the low-vol portfolio holds up.

| Year | Excess vs TAIEX |

|---|---|

| 2022 | +23.2% |

| 2007 | +17.9% |

| 2011 | +11.2% |

2022 stands out. Taiwan's semiconductor-heavy index fell 22% while the low-vol quality portfolio gained 1%. The portfolio's defensive positioning (telecoms, utilities, food) avoided the tech selloff. 2007 was similar: TAIEX gained only 5% while the portfolio rallied 23%.

When It Struggles

| Year | Excess vs TAIEX |

|---|---|

| 2020 | -19.8% |

| 2006 | -10.0% |

| 2009 | -10.1% |

2020 was the semiconductor super-cycle. Taiwan's chip stocks rallied 23% as pandemic demand for electronics exploded. The low-vol portfolio gained only 3%. The strategy deliberately avoids high-beta tech stocks, so it missed that rally. The same pattern in 2021 (+12% vs TAIEX +23%) and 2019 (+14% vs TAIEX +27%). Low-vol quality doesn't participate in tech surges. That's the trade-off.

Why Taiwan's Low-Vol Profile Is Unusual

Taiwan is a tech-dominated market where low-vol quality dramatically outperforms the local index on risk-adjusted returns (0.422 Sharpe vs 0.127 for TAIEX). The reason is structural.

Taiwan's listed company universe has a clear split. On one side: semiconductor and tech supply chain companies with high earnings cyclicality, tight analyst coverage, and high beta to global demand cycles. On the other: a smaller group of domestic-facing companies in telecoms, financials, food, and infrastructure. These companies have stable earnings, consistent margins, and genuinely low price volatility.

The quality filters (ROE > 10%, operating margin > 10%) don't eliminate one group or the other. Both tech and non-tech companies pass. But the volatility rank filter does the real work. It pulls the portfolio toward the domestic, non-cyclical cluster. The result is a portfolio that looks nothing like Taiwan's market cap-weighted index (which is overwhelmingly semiconductor stocks) but captures Taiwan's domestic economic stability.

This creates a genuine diversification benefit for global investors. You get Taiwan's corporate quality without Taiwan's tech-cycle risk.

Limitations

Cash drag. 20% cash periods reduce compounding. The 6.65% CAGR includes these periods. An investor could deploy capital elsewhere during cash quarters, but that requires a separate allocation decision.

Max drawdown was still -44.68%. Better than TAIEX's -53.74%, but still a large decline. The low-vol filter reduced volatility and improved risk-adjusted returns, but it didn't prevent deep drawdowns during market-wide panics.

Sector concentration risk. The low-vol filter concentrates the portfolio in non-tech sectors. Regulatory changes, domestic policy shifts, or sector-specific issues could hit these names disproportionately.

Currency effects. Returns are in TWD. TWD appreciation or depreciation against USD/EUR/etc. affects what a non-Taiwan investor actually receives.

Absolute return beats local market. The portfolio's 6.65% CAGR beats TAIEX's 4.38% by +2.28% annually. For investors seeking Taiwan exposure, this is a genuine improvement over the index.

Part of a Series

This is part of a global study testing low volatility + quality across 14 exchanges using local benchmarks. Taiwan beats its local benchmark by +2.28% annually.

- US flagship: 0.426 Sharpe over 25 years

- India: 16.8% CAGR, +5.7% vs Sensex

- Full 14-exchange comparison

Run It Yourself

Live screen:

python3 low-vol-quality/screen.py --preset taiwan

Backtest:

python3 low-vol-quality/backtest.py --preset taiwan --output results/returns_TAI.json --verbose

Code: github.com/ceta-research/backtests/tree/main/low-vol-quality

Takeaway

Taiwan's stock market is built around semiconductors. The low-vol quality strategy ignores that. It finds the 30 quietest, most profitable stocks on the exchange and holds them. The result: a portfolio that behaves like one-third the market's risk (beta 0.317), delivers a 0.422 Sharpe vs TAIEX's 0.127, and beats the local market by +2.28% annually with only 29% down capture.

The 20% cash rate shows the strategy is frequently starved for qualifying names. But when it's invested, the risk-adjusted performance is strong. Taiwan's non-cyclical companies, hidden behind the semiconductor headlines, provide genuine low-vol quality exposure that beats the local index.

For investors who want Taiwan exposure without the semiconductor roller coaster, this is what the data supports.

References

- Baker, M., Bradley, B. & Wurgler, J. (2011). "Benchmarks as Limits to Arbitrage: Understanding the Low-Volatility Anomaly." Financial Analysts Journal, 67(1), 40-54.

- Ang, A., Hodrick, R., Xing, Y. & Zhang, X. (2006). "The Cross-Section of Volatility and Expected Returns." Journal of Finance, 61(1), 259-299.

- Frazzini, A. & Pedersen, L. (2014). "Betting Against Beta." Journal of Financial Economics, 111(1), 1-25.

- Novy-Marx, R. (2013). "The Other Side of Value: The Gross Profitability Premium." Journal of Financial Economics, 108(1), 1-28.

Data: Ceta Research, 2000-2025. Full methodology: Methodology

Past performance does not guarantee future results. This is educational content, not investment advice.