Net Debt/EBITDA in Sweden: The Best Developed-Market Result in 22 Exchanges

Out of 22 exchanges, Sweden's Stockholm Stock Exchange produced the best developed-market result: 10.36% CAGR, +7.18% above the OMX Stockholm 30 annually, Sharpe 0.414. Here's why the signal works here.

Out of 22 exchanges we tested the Net Debt/EBITDA screen across, Sweden's Stockholm Stock Exchange produced the best result among developed markets: 10.36% CAGR, +7.18% above the OMX Stockholm 30 annually, Sharpe ratio 0.414. The signal works in Sweden because the exchange has an unusually high concentration of mid-cap industrial companies that are naturally conservatively leveraged, and the Swedish market hasn't been dominated by the benchmark-concentration dynamic that hurt other developed exchanges.

Contents

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

Signal: Net Debt/EBITDA < 2x and > -5x, ROE > 10%, Market Cap > SEK 5B (~$460M USD). Top 30 stocks by lowest ratio, equal weight. Universe: Stockholm Stock Exchange (STO). Full exchange, not index-constrained. Period: 2000-2025 (103 quarterly periods). Rebalancing: Quarterly (January, April, July, October). 45-day filing lag for point-in-time data. Execution: Market-on-close next trading day (signal generated at close, executed at next close). Transaction costs: Size-tiered model applied. Benchmark: OMX Stockholm 30. The local Swedish blue-chip index, the correct benchmark for measuring alpha in Swedish equities. Data: Ceta Research (FMP financial data warehouse).

What We Found

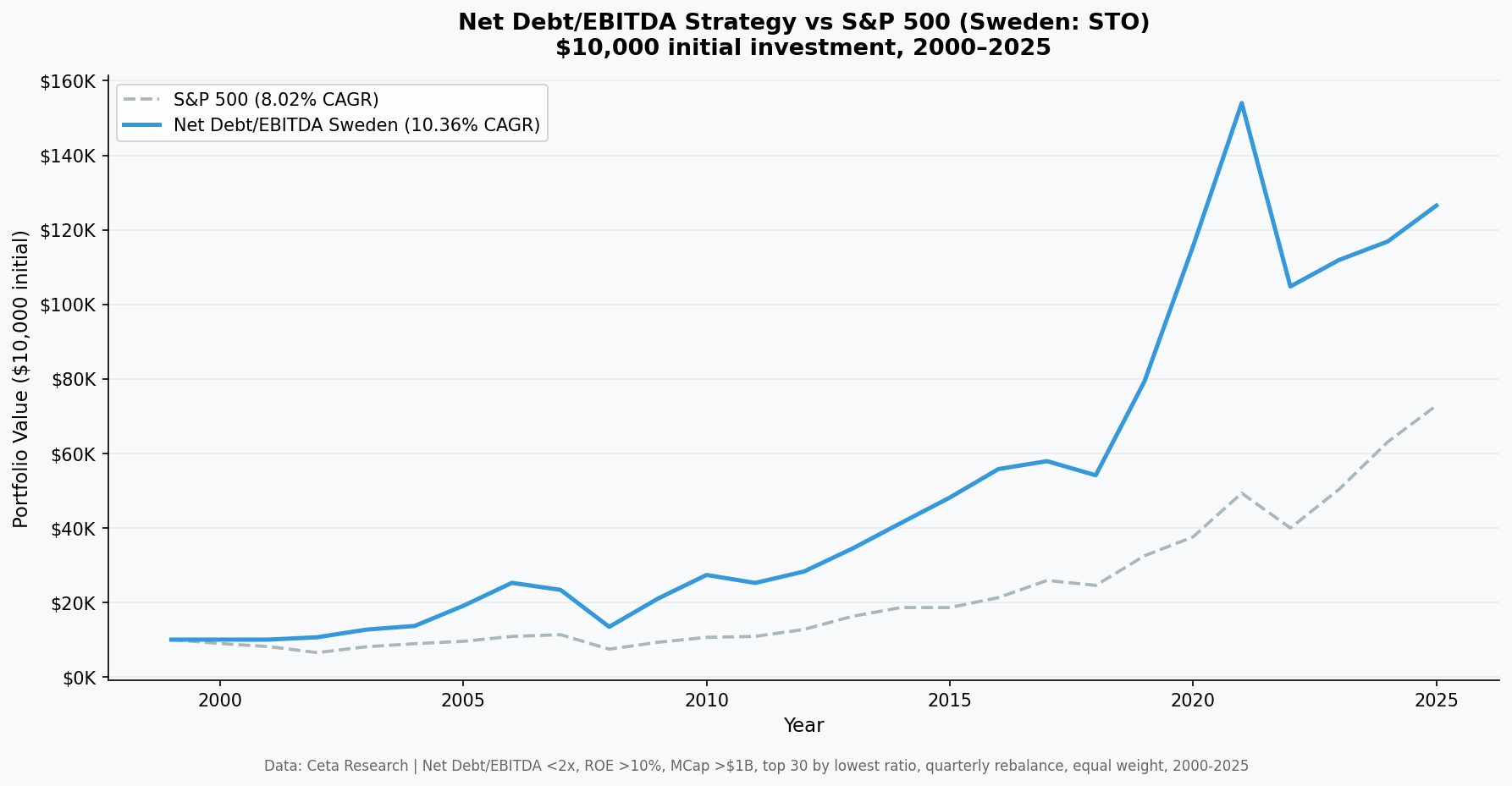

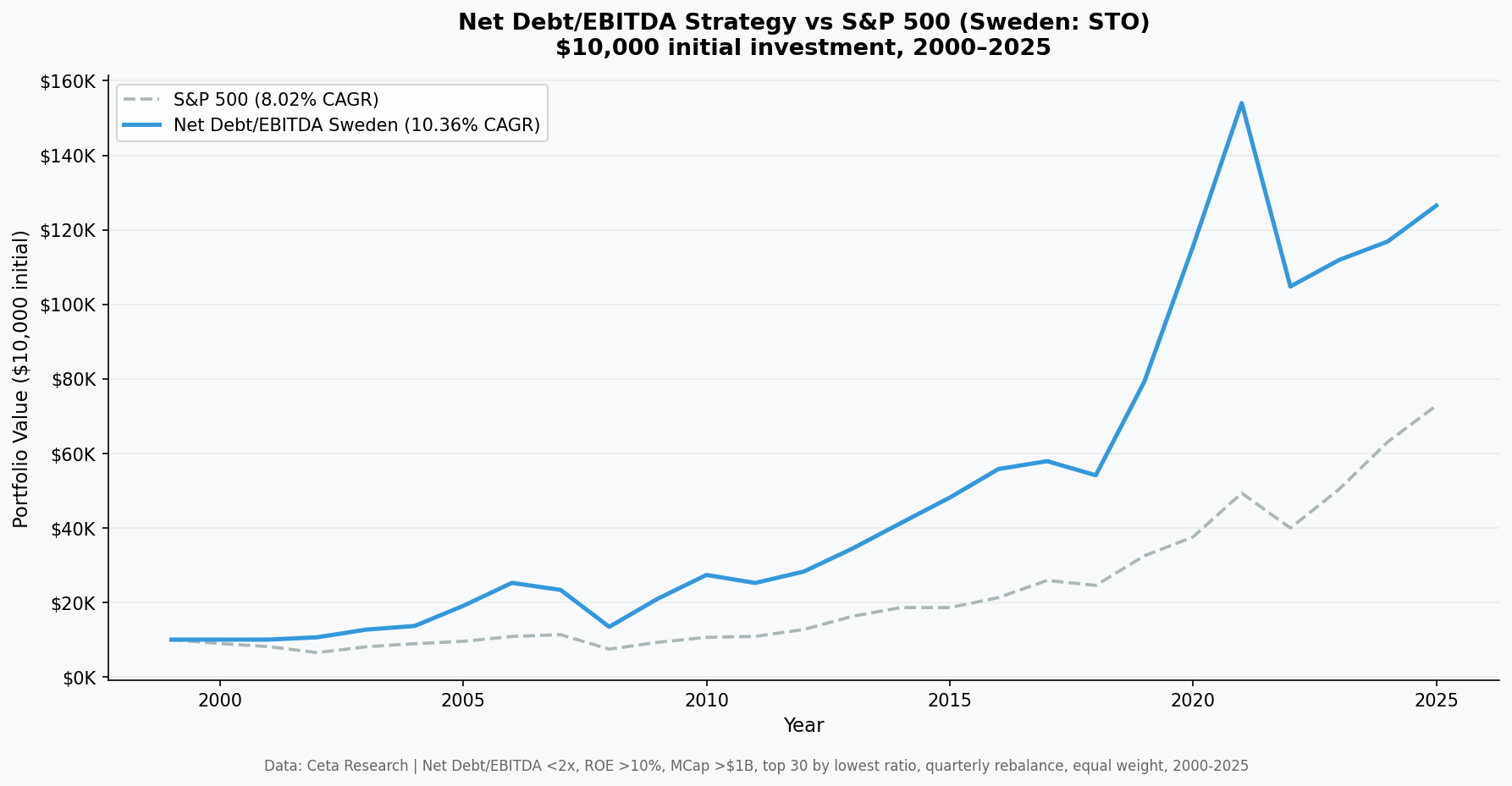

Strategy: 10.36% CAGR. OMX Stockholm 30: 3.17% CAGR (USD). Excess return: +7.18% per year over 25 years.

A $10,000 investment grew to $116,475. The same money tracking the OMX30 in USD grew to $22,452.

| Metric | Strategy | OMX Stockholm 30 |

|---|---|---|

| CAGR | 10.36% | 3.17% |

| Total Return | 1,164.8% | 124.5% |

| Max Drawdown | -52.98% | -66.13% |

| Annualized Volatility | 20.19% | 19.56% |

| Sharpe Ratio | 0.414 | 0.060 |

| Sortino Ratio | 0.689 | 0.082 |

| Beta (vs OMX30) | 0.794 | 1.0 |

| Alpha (annualized) | +7.42% | — |

| Up Capture | 109.5% | — |

| Down Capture | 62.7% | — |

The up/down capture pattern is strong: the strategy captures 109.5% of OMX30's gains and only 62.7% of its losses. The max drawdown of -52.98% is meaningfully better than the OMX30's own -66.13%, which suffered heavily in the 2000-2002 tech bust when Swedish telecom and tech companies (Ericsson, etc.) collapsed.

Note on the OMX30 CAGR: the OMX30 index is denominated in SEK, and FMP's price data is returned in USD. Swedish kronor has depreciated against the dollar over this period, which reduces the USD-converted return significantly. The OMX30's 3.17% CAGR in USD terms reflects both underlying equity returns and SEK/USD currency effects.

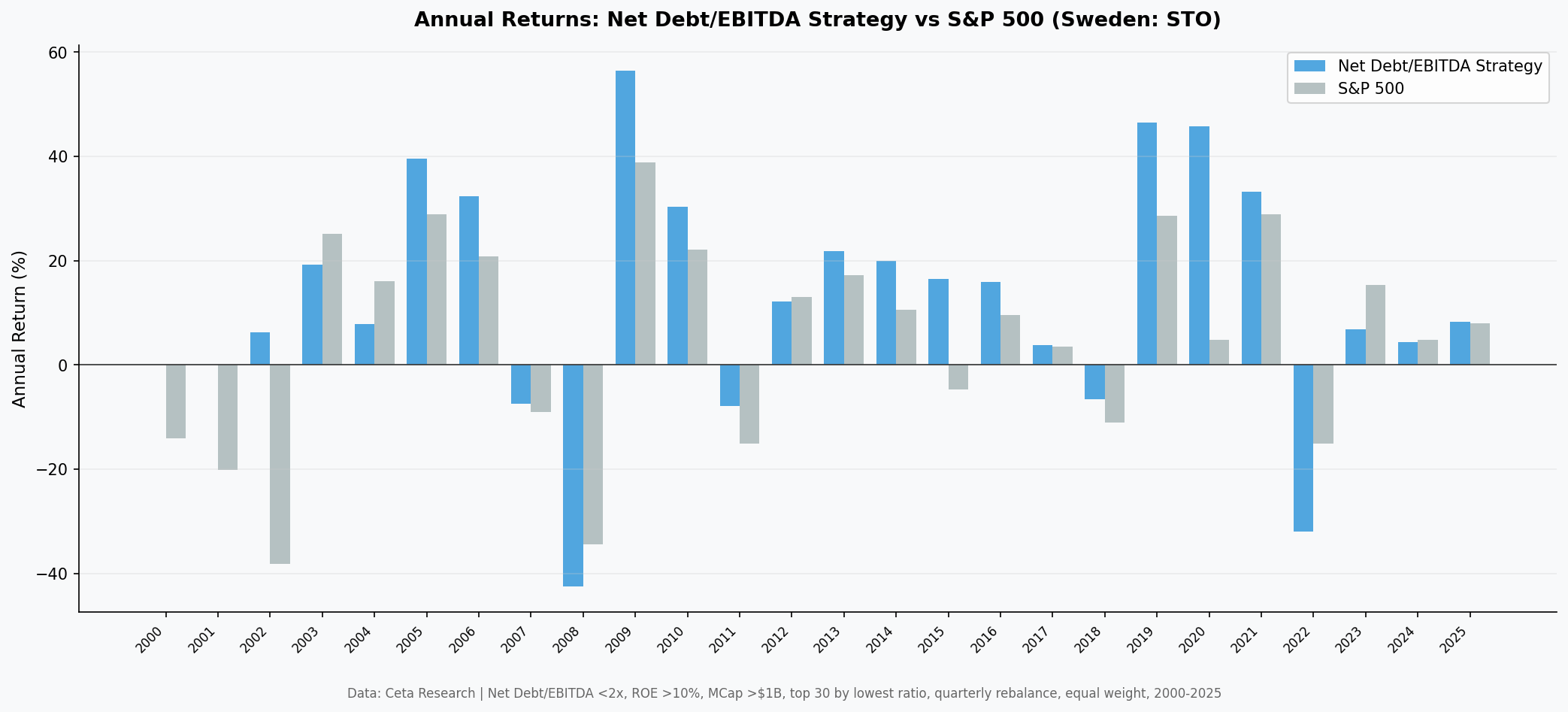

Year-by-Year

| Year | Strategy | OMX30 | Excess |

|---|---|---|---|

| 2000 | 0.0% | -14.0% | +14.0% |

| 2001 | +0.1% | -20.1% | +20.1% |

| 2002 | +6.3% | -38.2% | +44.4% |

| 2003 | +19.2% | +25.2% | -6.0% |

| 2004 | +7.8% | +16.0% | -8.2% |

| 2005 | +39.5% | +28.8% | +10.7% |

| 2006 | +32.4% | +20.8% | +11.5% |

| 2007 | -7.5% | -9.1% | +1.6% |

| 2008 | -42.5% | -34.4% | -8.1% |

| 2009 | +56.4% | +38.9% | +17.6% |

| 2010 | +30.3% | +22.1% | +8.1% |

| 2011 | -7.9% | -15.1% | +7.2% |

| 2012 | +12.1% | +13.1% | -0.9% |

| 2013 | +21.9% | +17.2% | +4.7% |

| 2014 | +20.0% | +10.5% | +9.4% |

| 2015 | +16.5% | -4.7% | +21.2% |

| 2016 | +15.9% | +9.5% | +6.4% |

| 2017 | +3.8% | +3.5% | +0.3% |

| 2018 | -6.6% | -11.0% | +4.5% |

| 2019 | +46.5% | +28.6% | +17.9% |

| 2020 | +45.8% | +4.8% | +41.0% |

| 2021 | +33.2% | +28.9% | +4.3% |

| 2022 | -32.0% | -15.1% | -16.9% |

| 2023 | +6.8% | +15.4% | -8.6% |

| 2024 | +4.4% | +4.8% | -0.3% |

| 2025 | +8.3% | +8.0% | +0.3% |

The dot-com period (2000-2002) was the clearest demonstration of the signal's protective quality. The OMX30 fell 14%, 20%, and 38% in consecutive years as Ericsson and other Swedish tech names collapsed. The low-leverage industrial screen held up: 0%, +0.1%, and +6.3% in those three years. That foundation of outperformance set the long-run compounding advantage.

2020 stands out: +45.8% vs OMX30's +4.8%. The OMX30 dropped sharply in Q1 2020 and recovered slowly in USD terms partly due to SEK weakness. The low-leverage industrials in the strategy fared better through the recovery.

2015 also shows strong defense: +16.5% vs OMX30's -4.7%. The European tightening environment hit Sweden hard, but capital-efficient industrials with low debt weathered it.

The trailing years (2022-2024) show recent weakness: the strategy fell more than the OMX30 in 2022 and underperformed modestly in 2023-2024. Swedish equities suffered from rate sensitivity and SEK/USD dynamics during the global tightening cycle.

Why Sweden?

Sweden produces an interesting combination: a developed-market equity culture with a relatively high proportion of mid-cap industrial and tech-adjacent companies that score well on balance sheet quality filters.

Key characteristics of the Swedish equity market:

Manufacturing and engineering base. Sweden has an unusually large concentration of exporters in engineering, automation, and specialty chemicals (Atlas Copco, Sandvik, ABB, Alfa Laval, Hexagon). These companies typically carry low debt relative to their earnings because their business models are capital-efficient rather than capital-intensive. The Net Debt/EBITDA screen naturally selects for them.

Strong corporate governance culture. Swedish corporate governance (ownership concentration, Wallenberg/Handelsbanken structures) tends toward financial conservatism. Swedish CFOs are not rewarded for financial engineering. They manage balance sheets conservatively as a matter of corporate culture.

Limited mega-cap tech concentration. Unlike the US, where 10 stocks now account for a third of the SPY index, Sweden's equity market is diversified enough that a fundamentals screen can actually differentiate winners from the index without constantly missing the handful of names doing all the work.

9% cash periods. The strategy was in cash 9 of 103 quarters (8.7%), periods where fewer than 10 qualifying stocks were available. These coincide with market stress periods where the balance sheet filter became very selective. The low cash rate confirms the screen had a functioning investable universe throughout the backtest.

Part of a Larger Picture

Sweden's result sits in context. This is one of 22 exchanges in a series testing the Net Debt/EBITDA screen globally. The flagship US post covers why the signal underperforms in the full US market. The India post covers the top result (+6.50% excess vs Sensex, 17.62% CAGR).

Sweden is the answer to a natural question: does the signal work anywhere in developed markets? Yes, but specifically in markets with the right sector composition and corporate culture.

The comparison across all 22 exchanges shows that markets with high weights to capital-efficient industrials and mid-caps tend to outperform on this screen. Markets with heavy financial sector or energy weights (where leverage is structural and EBITDA-relative debt is common) tend to underperform.

Run It Yourself

Current qualifying stocks (Sweden, TTM data):

SELECT

k.symbol,

p.companyName,

ROUND(k.netDebtToEBITDATTM, 2) AS net_debt_ebitda,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(k.marketCap / 1e9, 1) AS mktcap_bn

FROM key_metrics_ttm k

JOIN profile p ON k.symbol = p.symbol

WHERE k.netDebtToEBITDATTM < 2.0

AND k.netDebtToEBITDATTM > -5.0

AND k.returnOnEquityTTM > 0.10

AND k.marketCap > 5000000000 -- SEK 5B (~$460M USD)

AND p.exchange = 'STO'

ORDER BY k.netDebtToEBITDATTM ASC

LIMIT 30

Run this query on Ceta Research

Full backtest:

cd backtests

python3 net-debt-ebitda/backtest.py --preset sweden --verbose

Limitations

FX exposure. Swedish stocks report in SEK. The OMX30 benchmark also reflects SEK-denominated returns converted to USD. Both the strategy and benchmark are affected by SEK/USD movements, so the excess return (7.18%) is mostly currency-neutral. The absolute returns in USD (10.36% CAGR) reflect both equity performance and currency effects.

Small universe. STO has fewer than 500 stocks meeting the market cap filter. Cash periods (9% of quarters) reflect genuine scarcity at times. A 30-stock portfolio from ~150-200 qualifying names is more concentrated than the US equivalent.

Sector tilts. The portfolio tends to concentrate in industrials and technology-adjacent engineering firms. This isn't a Sweden ETF replacement, it's a specific sector-tilted portfolio within Sweden.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Universe: Stockholm Stock Exchange (STO), market cap > SEK 5B. Quarterly rebalance, equal weight, top 30 by lowest Net Debt/EBITDA. Point-in-time data with 45-day filing lag. Transaction costs: size-tiered model. Full methodology: backtests/METHODOLOGY.md. Backtest code: backtests/net-debt-ebitda/. Past performance does not guarantee future results. This is educational content, not investment advice.