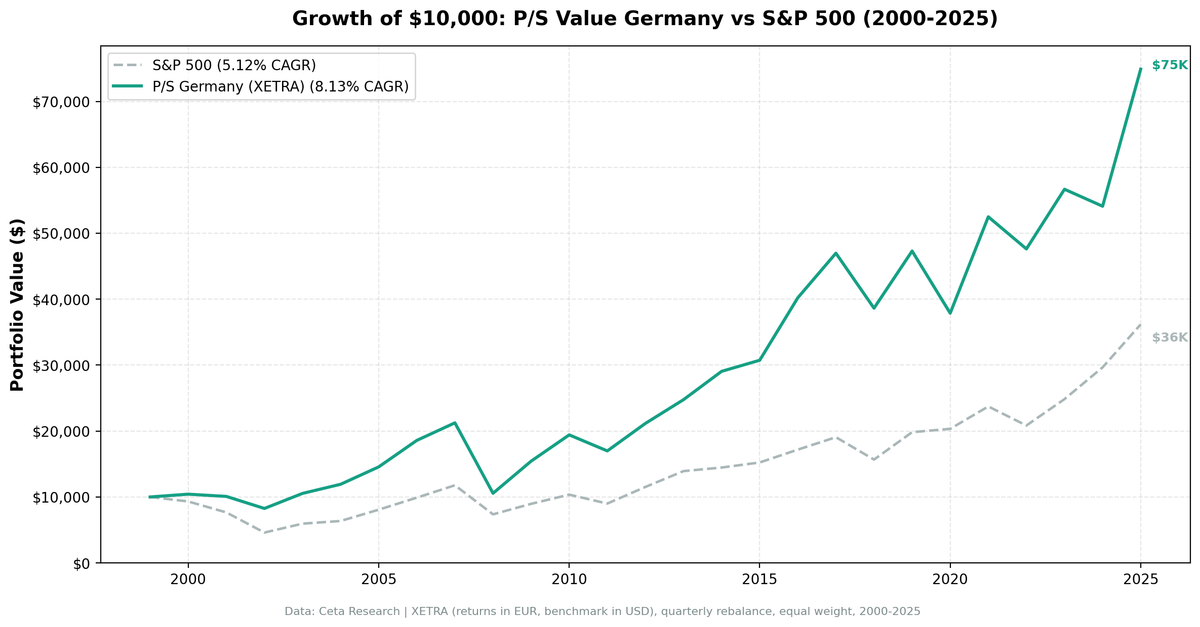

Price-to-Sales Below 1 in Germany: 8.13% CAGR, +3.01% vs DAX Over 25 Years

We screened XETRA-listed stocks for low price-to-sales ratios with qualifying margins and profitability, then backtested the resulting portfolio from 2000 to 2025. The strategy returned 8.13% annually vs 5.12% for the DAX, over 25 years and 103 quarterly periods. The Sharpe ratio is 0.291. The portfolio was never in cash.

Contents

- Method

- The Screen

- XETRA P/S Screen (SQL)

- What We Found

- 25 years. Solid alpha vs the local DAX.

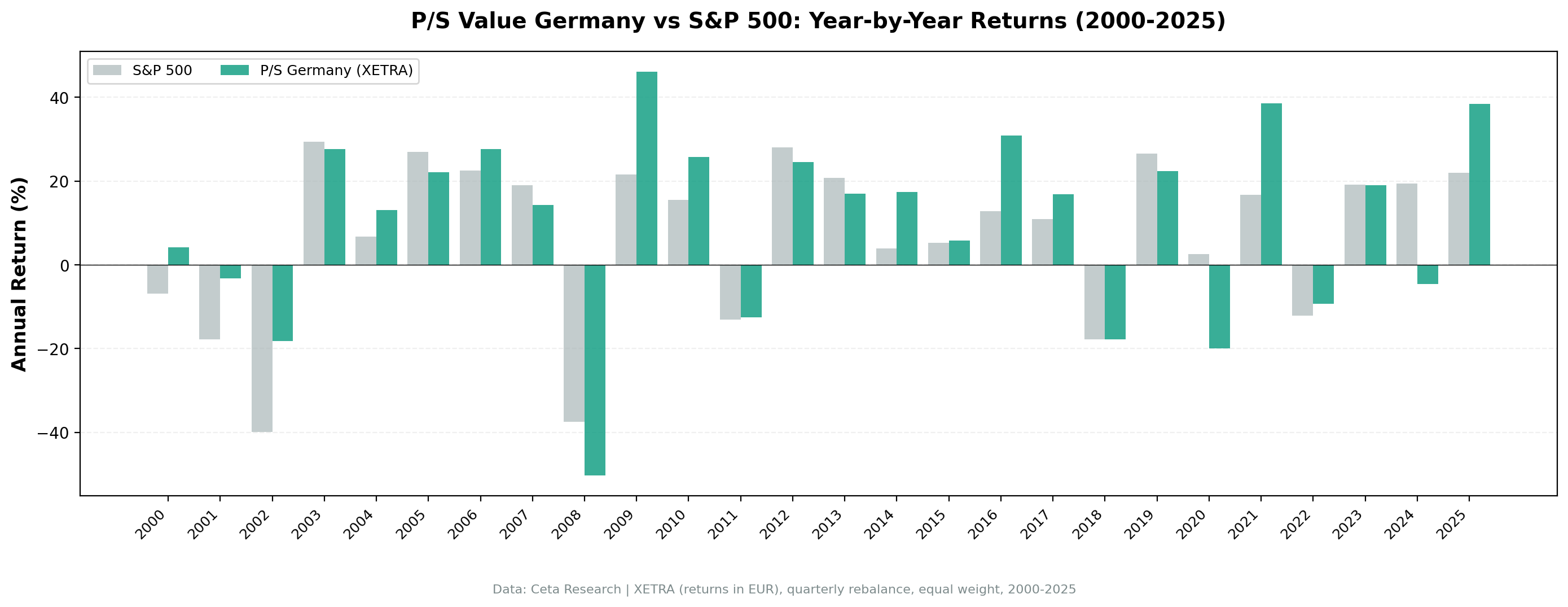

- Year-by-year returns

- 2006: a steady opening for the screen

- 2008: the drawdown event

- 2020: COVID hit European industrials differently

- 2024: flat amid structural weakness

- Where Germany's P/S screen works best

- Why Germany's Mittelstand fits this screen

- Backtest Methodology

- Limitations

- Takeaway

- Part of a Series

- References

- Run This Screen Yourself

Data: FMP financial data warehouse, 2000–2025. Updated June 2026.

Method

Data source: Ceta Research (FMP financial data warehouse) Universe: XETRA, market cap > €300M EUR Period: 2000-2025 (25 years, 103 quarterly periods) Rebalancing: Quarterly (January, April, July, October), equal weight, top 30 by lowest P/S Benchmark: DAX (German large-cap index) Cash rule: Hold cash if fewer than 10 stocks qualify Execution: Next-bar entry at close (MOC), 45-day lag on FY financial statements, data-quality guards remove price-oscillation artifacts and cap single-period returns at 200%.

Popularized by Kenneth Fisher in Super Stocks (1984). The P/S ratio avoids the noise in earnings-based metrics and works particularly well for companies with temporarily depressed margins.

The Screen

Signal filters:

| Criterion | Metric | Threshold |

|---|---|---|

| Cheap relative to revenue | Price-to-Sales | < 1.0 |

| Business quality | Gross Margin | > 20% |

| Operational efficiency | Operating Margin | > 5% |

| Capital returns | ROE | > 10% |

Size filter: Market cap > €300M EUR

Selection: Top 30 by lowest P/S among qualifying stocks.

XETRA P/S Screen (SQL)

SELECT

f.symbol,

p.companyName,

p.exchange,

p.sector,

ROUND(f.priceToSalesRatioTTM, 3) AS ps_ratio,

ROUND(f.grossProfitMarginTTM * 100, 1) AS gross_margin_pct,

ROUND(f.operatingProfitMarginTTM * 100, 1) AS op_margin_pct,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM financial_ratios_ttm f

JOIN key_metrics_ttm k ON f.symbol = k.symbol

JOIN profile p ON f.symbol = p.symbol

WHERE f.priceToSalesRatioTTM > 0

AND f.priceToSalesRatioTTM < 1

AND f.grossProfitMarginTTM > 0.20

AND f.operatingProfitMarginTTM > 0.05

AND k.returnOnEquityTTM > 0.10

AND k.marketCap > 300000000

AND p.exchange IN ('XETRA')

QUALIFY ROW_NUMBER() OVER (PARTITION BY f.symbol ORDER BY f.priceToSalesRatioTTM ASC) = 1

ORDER BY f.priceToSalesRatioTTM ASC

LIMIT 30

Run this query on Ceta Research

What We Found

25 years. Solid alpha vs the local DAX.

| Metric | P/S Screen (XETRA) | DAX |

|---|---|---|

| CAGR | 8.13% | 5.12% |

| Excess Return | +3.01% | — |

| Max Drawdown | -58.57% | — |

| Sharpe Ratio | 0.291 | — |

| Avg Stocks per Period | 16.9 | — |

| Cash Periods | 0 of 103 | — |

The strategy turned €10,000 into approximately €75,000. Zero cash periods across 103 quarters: German mid-cap companies consistently had enough stocks trading below 1x revenue to stay fully invested the entire time.

The Sharpe of 0.291 is solid but no longer top tier. After data-quality cleanup, Sweden (0.452), the US (0.404), and Japan (0.379) all sit higher. Germany combines a deep Mittelstand manufacturing base, consistent profitability, and modest market valuations relative to earnings and sales, but the corrected numbers reveal more drawdown risk than the previous run suggested.

Year-by-year returns

| Year | XETRA P/S | DAX | Excess |

|---|---|---|---|

| 2000 | +4.23% | -6.83% | +11.06% |

| 2001 | -3.25% | -17.84% | +14.58% |

| 2002 | -18.13% | -39.92% | +21.79% |

| 2003 | +27.66% | +29.42% | -1.76% |

| 2004 | +13.14% | +6.79% | +6.34% |

| 2005 | +22.12% | +26.99% | -4.88% |

| 2006 | +27.59% | +22.59% | +5.00% |

| 2007 | +14.32% | +18.98% | -4.66% |

| 2008 | -50.29% | -37.44% | -12.85% |

| 2009 | +46.13% | +21.62% | +24.51% |

| 2010 | +25.83% | +15.57% | +10.26% |

| 2011 | -12.52% | -13.08% | +0.56% |

| 2012 | +24.57% | +28.03% | -3.46% |

| 2013 | +17.01% | +20.84% | -3.83% |

| 2014 | +17.36% | +3.88% | +13.48% |

| 2015 | +5.79% | +5.31% | +0.47% |

| 2016 | +30.83% | +12.79% | +18.04% |

| 2017 | +16.81% | +10.98% | +5.83% |

| 2018 | -17.75% | -17.80% | +0.05% |

| 2019 | +22.43% | +26.52% | -4.09% |

| 2020 | -19.93% | +2.55% | -22.47% |

| 2021 | +38.60% | +16.71% | +21.89% |

| 2022 | -9.28% | -12.18% | +2.90% |

| 2023 | +19.00% | +19.19% | -0.19% |

| 2024 | -4.54% | +19.41% | -23.95% |

| 2025 | +38.43% | +21.96% | +16.47% |

2006: a steady opening for the screen

The portfolio gained +27.59% in 2006 while the DAX returned +22.59%. Germany's export machine was running at full capacity. Chinese industrialization drove demand for German capital equipment, machine tools, and automotive components. The P/S screen captured a meaningful share of that re-rating.

2008: the drawdown event

The same industrial exposure that drove the 2006-2007 gains produced a -50.29% drawdown in 2008. This is the honest tradeoff. XETRA industrials and exporters are cyclical. When global demand collapses, so do their revenues, and low P/S stocks get hit harder than defensive names. The max drawdown of -58.57% across the cycle is real.

If you're investing in this strategy, the 2008 experience is what you're signing up to survive through.

2020: COVID hit European industrials differently

The portfolio returned -19.93% in 2020 while the DAX gained +2.55%. German industrials took the full hit of lockdowns and supply chain disruption with no equivalent tech sector to cushion the fall. The DAX's recovery was driven by a handful of large-cap names; the mid-cap P/S screen didn't share in it.

2024: flat amid structural weakness

The portfolio returned -4.54% in 2024 while the DAX gained +19.41%. XETRA was weak across the board that year. The auto sector (BMW, Mercedes-Benz, Volkswagen) suffered margin compression from Chinese EV competition and weak domestic demand. Energy-intensive manufacturers were still working through post-2022 cost structures. Stocks that looked cheap on P/S kept getting cheaper.

Where Germany's P/S screen works best

The screen performs best during global growth cycles where German exports are in demand (2003-2007, 2009-2010, 2014-2016). It struggles when the DAX is being pulled up by a few large-cap names while mid-cap industrials lag (2023-2024).

| Period | XETRA P/S | DAX | Excess |

|---|---|---|---|

| Growth cycle (2003-07) | +135% cumulative | +156% cumulative | -21% |

| Post-crisis recovery (2009-10) | +84% cumulative | +41% cumulative | +43% |

| Recent drag (2019-24) | +37% cumulative | +89% cumulative | -52% |

Why Germany's Mittelstand fits this screen

German mid-cap companies (the Mittelstand) are often family-controlled, export-oriented manufacturers. They run lean balance sheets, maintain consistent margins, and rarely trade at high revenue multiples because they're not growth stories. They're durable businesses generating consistent cash flow.

That's exactly what a P/S < 1 screen with margin requirements is designed to find. The screen isn't just coincidentally working in Germany. Germany's market structure is naturally suited to it.

Backtest Methodology

| Parameter | Choice |

|---|---|

| Universe | XETRA, Market Cap > €300M EUR |

| Signal | P/S < 1.0, Gross Margin > 20%, Operating Margin > 5%, ROE > 10% |

| Portfolio | Top 30 by lowest P/S, equal weight |

| Rebalancing | Quarterly (January, April, July, October) |

| Cash rule | Hold cash if < 10 qualify |

| Benchmark | DAX |

| Period | 2000-2025 (25 years, 103 periods) |

| Execution | Next-bar (MOC), 45-day lag, data-quality guards |

Limitations

Drawdown risk. The -58.57% max drawdown is substantial. Industrial cyclicality is real. Any investor in this strategy needs to be prepared for a 2008-type event.

Currency exposure. Returns are in EUR. A US investor holding XETRA stocks takes on EUR/USD currency risk. EUR depreciation reduces USD-denominated returns; appreciation adds to them.

Concentration in industrials and materials. The P/S filter naturally pulls toward capital-intensive manufacturers. Sector concentration is a persistent feature, not an accident.

2024 structural headwinds. The auto sector's de-rating and ongoing energy cost pressures create genuine fundamental risks that a backward-looking screen won't flag. These aren't cyclical dips. Some may be structural.

Survivorship bias. Exchange membership uses current profiles, not historical. Delistings and restructurings aren't tracked.

Transaction costs not included. With quarterly rebalancing and roughly 17 stocks, cost drag is approximately 0.3-0.5% annually at standard institutional rates.

Takeaway

The XETRA P/S screen returned 8.13% CAGR over 25 years, 3.01% annual alpha over the DAX, and a Sharpe of 0.291 with zero cash periods. After data-quality cleanup it sits below Sweden (0.452), the US (0.404), and Japan (0.379) on risk-adjusted terms, but it still meaningfully beats its local benchmark.

The reason isn't mysterious. Germany has a deep base of mid-cap industrial companies with genuine profitability, consistent margins, and modest market valuations. The P/S screen finds them systematically. The 45-day lag keeps the data clean. Quarterly rebalancing keeps the portfolio current.

The tradeoff is drawdown. The worst year was 2008 at -50.29%. The max drawdown hit -58.57%. If you hold XETRA industrials through a global demand collapse, they'll fall hard. That's the deal. The 25-year track record says the long-run math works in your favor, but you have to actually stay in through those years.

Returns are in EUR. For international investors, the EUR/USD component adds another layer of risk and return to factor in.

Part of a Series

This analysis is part of our P/S value screen global exchange comparison. We tested the same four-factor screen across 15 exchanges worldwide: - P/S Value Screen on US Stocks - P/S Value Screen on Indian Stocks - P/S Value Screen on Canadian Stocks - P/S Value Screen on Swedish Stocks - P/S Value Screen on South African Stocks - P/S Value Screen on Japanese Stocks - P/S Value Screen: 15-Exchange Global Comparison

References

- Fisher, K. (1984). Super Stocks. Dow Jones-Irwin.

- Barbee, W., Mukherji, S. & Raines, G. (1996). "Do Sales-Price and Debt-Equity Explain Stock Returns Better than Book-Market and Firm Size?" Financial Analysts Journal, 52(2), 56-60.

- Gray, W. & Vogel, J. (2012). "Analyzing Valuation Measures: A Performance Horse Race over the Past 40 Years." Journal of Portfolio Management, 39(1), 112-121.

- Novy-Marx, R. (2013). "The Other Side of Value: The Gross Profitability Premium." Journal of Financial Economics, 108(1), 1-28.

Run This Screen Yourself

Via web UI: Run the P/S screen on Ceta Research. The query is pre-loaded. Hit "Run" and see what passes today.

Via Python:

import requests, time

API_KEY = "your_api_key" # get one at cetaresearch.com

BASE = "https://tradingstudio.finance/api/v1"

resp = requests.post(f"{BASE}/data-explorer/execute", headers={

"X-API-Key": API_KEY, "Content-Type": "application/json"

}, json={

"query": """

SELECT

f.symbol,

p.companyName,

ROUND(f.priceToSalesRatioTTM, 3) AS ps_ratio,

ROUND(f.grossProfitMarginTTM * 100, 1) AS gross_margin_pct,

ROUND(f.operatingProfitMarginTTM * 100, 1) AS op_margin_pct,

ROUND(k.returnOnEquityTTM * 100, 1) AS roe_pct,

ROUND(k.marketCap / 1e9, 2) AS mktcap_b

FROM financial_ratios_ttm f

JOIN key_metrics_ttm k ON f.symbol = k.symbol

JOIN profile p ON f.symbol = p.symbol

WHERE f.priceToSalesRatioTTM > 0

AND f.priceToSalesRatioTTM < 1

AND f.grossProfitMarginTTM > 0.20

AND f.operatingProfitMarginTTM > 0.05

AND k.returnOnEquityTTM > 0.10

AND k.marketCap > 300000000

AND p.exchange IN ('XETRA')

QUALIFY ROW_NUMBER() OVER (

PARTITION BY f.symbol ORDER BY f.priceToSalesRatioTTM ASC

) = 1

ORDER BY f.priceToSalesRatioTTM ASC

LIMIT 30

""",

"options": {"format": "json", "limit": 30}

})

task_id = resp.json()["taskId"]

while True:

result = requests.get(f"{BASE}/tasks/data-query/{task_id}",

headers={"X-API-Key": API_KEY}).json()

if result["status"] in ("completed", "failed"):

break

time.sleep(2)

for r in result["result"]["rows"]:

print(f"{r['symbol']:10s} P/S={r['ps_ratio']:.3f} GM={r['gross_margin_pct']:.1f}% ROE={r['roe_pct']:.1f}%")

Get your API key at cetaresearch.com. The full backtest code (Python + DuckDB) is on GitHub.

Data: Ceta Research, FMP financial data warehouse. Universe: XETRA. Returns in EUR. Quarterly rebalance, equal weight, 2000-2025.

Past performance does not guarantee future results. This is educational content, not investment advice.