Sector Momentum in Germany: 11.13% CAGR, +6.04% Excess Over DAX, 26 Years (XETRA)

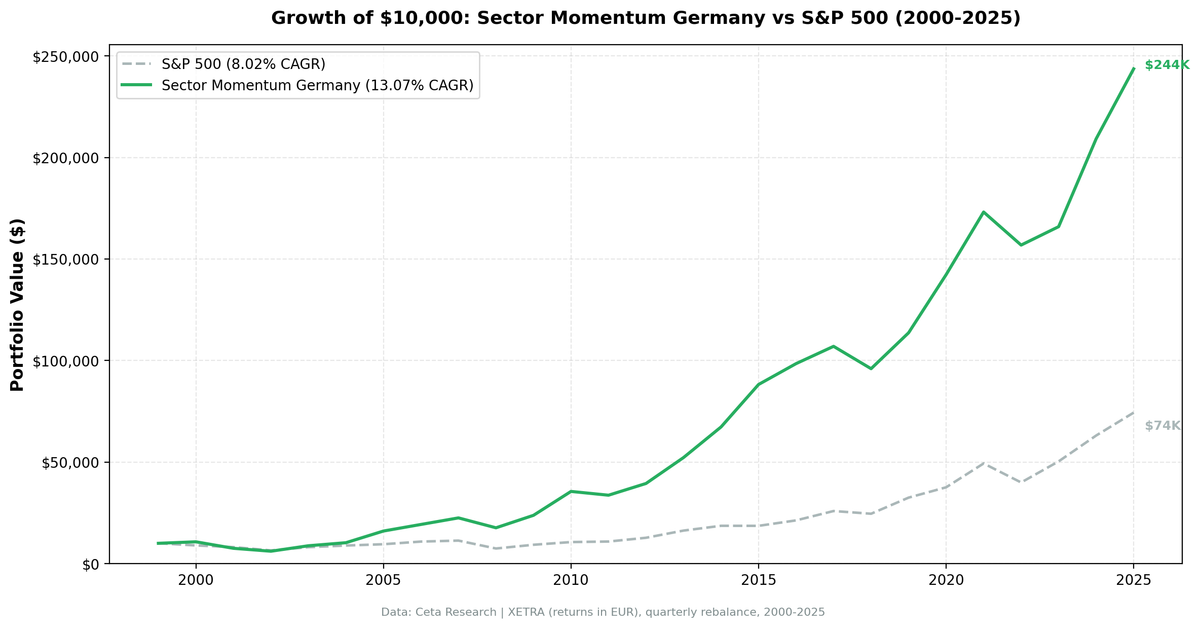

Germany produced the best sector momentum results of any European market in our 14-exchange study. 13.07% CAGR over 26 years, +5.05% excess vs S&P 500, Sharpe 0.620, and 55.30% down capture. The defining structural pattern: Technology and Real Estate each appeared in exactly 30 of 104 quarterly...

Germany delivered the best sector momentum results of any European market in our 14-exchange study. 11.13% CAGR over 26 years. $10,000 grew to €155,569 in EUR-denominated terms versus the DAX baseline. The 2008 global financial crisis tells a lot about why: the portfolio returned -28.58% while the DAX fell -37.44%. That 8.86% relative gap in a single year captures the structural protection built into Germany's sector rotation patterns.

Contents

- The Strategy

- Results

- The Technology and Real Estate Cycle

- When It Worked, When It Didn't

- Full Annual Returns

- Limitations

Two sectors tied for the most time in the top-2 rotation: Technology and Real Estate, each appearing in 30 of 104 quarters. That alternating cycle between Germany's industrial-tech leadership and its property market is the mechanical backbone of this strategy's long-run edge.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

The Strategy

Each quarter, we rank all 11 GICS sectors by their equal-weighted 12-month trailing return across XETRA-listed stocks. We hold stocks from the top 2 sectors, equal-weighted, and rebalance quarterly. Stocks must clear an exchange-specific market cap threshold. Transaction costs of 0.1% per trade are applied.

Full methodology: backtests/METHODOLOGY.md

| Parameter | Value |

|---|---|

| Universe | XETRA (Germany) |

| Signal | Top 2 sectors by trailing 12-month equal-weighted return |

| Selection | All qualifying stocks in those sectors |

| Rebalancing | Quarterly |

| Period | 2000-2025 (26 years, 104 quarters) |

| Cash periods | 3 of 104 (3%) |

| Avg stocks held | 64.6 |

| Benchmark | DAX (EUR) |

| Data source | Ceta Research (FMP financial data warehouse) |

Returns are in EUR. DAX is also EUR-denominated — this is an apples-to-apples comparison.

Results

The aggregate numbers:

| Metric | Portfolio | DAX (EUR) |

|---|---|---|

| CAGR (2000-2025) | 11.13% | 5.09% |

| Excess CAGR | +6.04% | — |

| Final value ($10k) | €155,569 | — |

| Max drawdown | -52.85% | — |

| Sharpe ratio | 0.501 | — |

| Sortino ratio | 0.791 | — |

| Calmar ratio | 0.210 | — |

| Up capture | 90.78% | — |

| Down capture | 50.30% | — |

| Beta | 0.639 | — |

| Alpha | 7.16% | — |

| Win rate vs DAX | 57.69% | — |

The down capture of 50.30% vs DAX means the portfolio fell roughly half as much as the German index in down periods on average. That asymmetry compounds over 26 years into a meaningful wealth difference. A beta of 0.639 reflects lower sensitivity to German market cycles, driven by the real estate and healthcare components of the rotation.

The Sharpe of 0.501 reflects a solid risk-adjusted result for a pure equity strategy over this period, particularly spanning two full market crashes.

The Technology and Real Estate Cycle

Germany's sector rotation has a structural pattern that doesn't appear in most other markets. Technology and Real Estate tied at exactly 30 quarters each in the top-2 rotation.

| Sector | Quarters in Top 2 |

|---|---|

| Technology | 30 |

| Real Estate | 30 |

| Basic Materials | 23 |

| Energy | 21 |

| Communication Services | 19 |

| Consumer Defensive | 19 |

| Healthcare | 19 |

| Consumer Cyclical | 19 |

| Industrials | 14 |

| Utilities | 13 |

| Financial Services | 1 |

Germany's technology sector is dominated by companies like SAP, Siemens, and Infineon, which are industrial-adjacent technology leaders, not speculative growth stocks. When global tech cycles run, Germany's version runs with lower volatility. The Real Estate component reflects Germany's decades-long property appreciation cycle, which accelerated post-GFC as European rates dropped toward zero and German housing supply stayed constrained.

These two sectors don't typically lead at the same time. The strategy rotated between them across different macro phases. From 2003 to 2007, Real Estate and Basic Materials drove returns. Post-2009, Real Estate resumed leadership as ECB rates fell. Technology returned to dominance in later cycles. The mechanical rotation between these two themes explains why the Sharpe sits at 0.501 despite a 26-year holding period spanning two full market crashes.

Financial Services appeared only once. Germany's financial sector, anchored by Deutsche Bank, struggled with persistently low margins in the European rate environment. The signal correctly avoided it.

When It Worked, When It Didn't

The 2000 dotcom crash: protection from the start. Germany's sector momentum portfolio returned +9.31% in 2000 while the DAX fell -6.83%. That's a +16.13% gap in year one. German sectors weren't loaded with speculative tech. The rotation held Basic Materials and Real Estate as tech imploded.

2001: Heavy tech exposure in Germany. The reversal was sharp. The portfolio fell -27.50% in 2001 while the DAX fell -17.84%. Germany's tech sector, including telecoms and software, suffered its own version of the crash. The strategy lagged by 9.66%. This is the clearest downside of momentum: when the sector that led into a crash is still in the top-2 signal entering the next period, you take the full hit.

2005 and 2010: What sustained sector trends look like. Two years stand out as the clearest examples of momentum compounding:

| Year | Portfolio | DAX | Excess |

|---|---|---|---|

| 2005 | +42.73% | +26.99% | +15.74% |

| 2010 | +48.77% | +15.57% | +33.21% |

2005 was a Real Estate and Technology momentum year in Germany. Both sectors had sustained multi-quarter trends running. The strategy was fully positioned and captured significantly more than the index. 2010 followed the same pattern as post-GFC recovery drove Real Estate and Basic Materials for consecutive quarters.

2008: The crisis protection result. This is the year that matters most for understanding the structural character of this strategy.

| Year | Portfolio | DAX | Excess |

|---|---|---|---|

| 2008 | -28.58% | -37.44% | +8.86% |

A -28.58% loss still hurts. But in a year where the global financial system nearly collapsed and Germany's index fell -37.44%, the sector momentum portfolio's relative outperformance of 8.86% is substantial. Germany's Real Estate sector, while it did decline, wasn't leveraged to US subprime. Consumer Defensive was in the rotation. The beta of 0.639 shows up clearly when markets crash.

The recent period (2017-2024). Germany's rotation showed a mixed pattern against the DAX.

| Year | Portfolio | DAX | Excess |

|---|---|---|---|

| 2017 | +15.14% | +10.98% | +4.16% |

| 2018 | -3.59% | -17.80% | +14.21% |

| 2019 | +22.43% | +26.52% | -4.09% |

| 2020 | +2.62% | +2.55% | +0.08% |

| 2021 | +15.77% | +16.71% | -0.94% |

| 2022 | -9.48% | -12.18% | +2.70% |

| 2023 | +8.62% | +19.19% | -10.57% |

| 2024 | +16.07% | +19.41% | -3.35% |

2023 was the weakest recent year. The strategy returned +8.62% while the DAX gained +19.19%. But 2018 flipped the script: -3.59% vs DAX -17.80% (+14.21% relative) as European defensive and real estate sectors held far better than the broader market. The 2017 and 2019 years were close to the index, and 2025 returned a strong +26.81% vs DAX +22.55%.

Full Annual Returns

| Year | Portfolio (EUR) | DAX (EUR) | Excess |

|---|---|---|---|

| 2000 | +9.31% | -6.83% | +16.13% |

| 2001 | -27.50% | -17.84% | -9.66% |

| 2002 | -22.05% | -39.92% | +17.86% |

| 2003 | +26.42% | +29.42% | -2.99% |

| 2004 | +18.49% | +6.79% | +11.70% |

| 2005 | +42.73% | +26.99% | +15.74% |

| 2006 | +26.36% | +22.59% | +3.77% |

| 2007 | +10.51% | +18.98% | -8.47% |

| 2008 | -28.58% | -37.44% | +8.86% |

| 2009 | +34.23% | +21.62% | +12.61% |

| 2010 | +48.77% | +15.57% | +33.21% |

| 2011 | -6.99% | -13.08% | +6.09% |

| 2012 | +24.97% | +28.03% | -3.07% |

| 2013 | +28.85% | +20.84% | +8.01% |

| 2014 | +28.30% | +3.88% | +24.42% |

| 2015 | +22.65% | +5.31% | +17.34% |

| 2016 | +7.40% | +12.79% | -5.39% |

| 2017 | +15.14% | +10.98% | +4.16% |

| 2018 | -3.59% | -17.80% | +14.21% |

| 2019 | +22.43% | +26.52% | -4.09% |

| 2020 | +2.62% | +2.55% | +0.08% |

| 2021 | +15.77% | +16.71% | -0.94% |

| 2022 | -9.48% | -12.18% | +2.70% |

| 2023 | +8.62% | +19.19% | -10.57% |

| 2024 | +16.07% | +19.41% | -3.35% |

| 2025 | +26.81% | +22.55% | +4.27% |

The early period (2000-2015) shows consistent alpha against the DAX. The exceptions are 2001 (tech crash follow-through), 2003, and 2007 (real estate cycle reversal). Post-2015, the pattern is more mixed, with strong relative years in 2018, 2022, and 2025 offset by underperformance in 2016, 2019, 2023, and 2024.

Limitations

Currency exposure. Returns are in EUR. Non-European investors face EUR/USD exchange rate exposure on top of equity volatility. The DAX comparison is apples-to-apples for EUR investors, but USD investors carry an additional currency layer.

The 2001 lesson. A -27.50% year, 9.66% worse than the DAX, is a reminder that momentum can carry you into a crash. If the signal was positioned in Germany's tech-telecom complex heading into 2001, the strategy took the full drawdown before rotating out.

Max drawdown. -52.85% is not a comfortable number. The GFC and the European debt crisis together put pressure on the strategy in multiple consecutive years. Investors need to be prepared to hold through multi-year drawdown and recovery cycles.

Sector concentration. With an average of 64.6 stocks across just 2 sectors, the portfolio is more concentrated than US or India versions of this strategy. Position-level diversification is thinner, which amplifies single-sector events.

Recent DAX underperformance. The 2023 (-10.57%) and 2019 (-4.09%) gaps show that Germany's rotation doesn't always keep up with the local index. When the DAX rallies broadly, the strategy's sector concentration can lag. 2023 was the worst single year in the recent period.

Win rate. 57.69% annual win rate against the DAX is solid. Expect occasional multi-year underperformance periods, particularly when Germany's broad market rallies strongly across multiple sectors.

Data: Ceta Research (FMP financial data warehouse). Universe: XETRA (Germany). Period: 2000-2025 (26 years), quarterly rebalance, returns in EUR. Past performance does not guarantee future results. This is educational content, not investment advice.

Part of the Sector Momentum Rotation series. US flagship blog