Small-Cap Growth Taiwan: Barely Beats TAIEX (+0.29%/yr), Lags SPY (-3.47%/yr)

Taiwan's small-cap growth screen returned 4.38% CAGR, barely ahead of TAIEX at 4.09% (+0.29%/yr) and well behind SPY at 7.85% (-3.47%/yr). 36% win rate versus both benchmarks. Semiconductor-cycle pattern of feast-or-famine annual returns.

Taiwan has TSMC. It has a world-class semiconductor ecosystem and decades of export-driven growth. The assumption going in is that a small-cap growth screen here should capture upstream and downstream beneficiaries of that engine. The data says otherwise. 4.38% CAGR over 25 years, barely ahead of the TAIEX at 4.09% but well behind SPY at 7.85%. A 36% win rate versus SPY. Only 9 of 25 years beat SPY.

Contents

- Executive Summary

- The Method

- What We Found

- The semiconductor cycle problem

- 89% up capture versus TAIEX, but both lag SPY

- The 6 cash-year impact

- 2024 performance breakdown

- Annual Returns

- When It Works and When It Fails

- Why Large-Cap Taiwan Works but Small-Cap Doesn't

- Limitations

- Run It Yourself

- Takeaway

- References

The issue isn't Taiwan's economy. It's the structure of Taiwan's small-cap market and how the semiconductor cycle distorts any growth filter. Against the local TAIEX benchmark, the strategy wins by just +0.29%/yr, which is statistically noise.

Executive Summary

| Metric | Taiwan (TAI) | TAIEX | SPY |

|---|---|---|---|

| CAGR | 4.38% | 4.09% | 7.85% |

| Excess vs TAIEX | +0.29%/yr | — | — |

| Excess vs SPY | -3.47%/yr | — | — |

| Sharpe Ratio | 0.175 | 0.161 | 0.360 |

| Sortino Ratio | 0.378 | 0.280 | 0.654 |

| Max Drawdown | -38.47% | -41.11% | -36.27% |

| Win Rate vs TAIEX | 36% | — | — |

| Win Rate vs SPY | 36% | — | — |

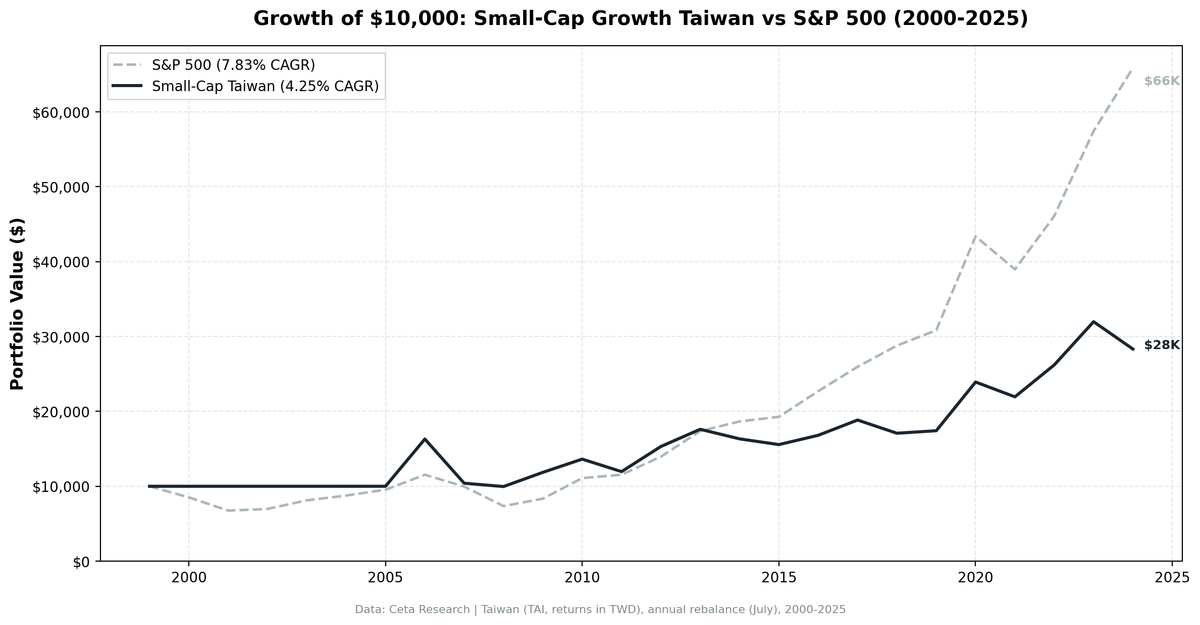

| $10K → | $29,191 | $27,209 | — |

| Up Capture vs TAIEX | 89.4% | — | — |

| Down Capture vs TAIEX | 72.8% | — | — |

$10,000 invested in 2000 became $29,191 by end of 2024. The TAIEX turned it into $27,209. SPY would have returned roughly 2.7× as much in absolute dollars. The 36% win rate versus both benchmarks means the strategy underperformed in 16 of 25 years. The +0.29%/yr versus TAIEX is barely meaningful.

The Method

We screened the Taiwan Stock Exchange (TAI) annually each July (with a 45-day filing lag). The filter:

- Market cap between NT$500M and NT$20B (small-cap bounds for Taiwan)

- Revenue growth >15% year-over-year (fiscal year)

- Positive net income

- Debt-to-equity <2.0

Top 30 by revenue growth, equal weight. Annual rebalance.

Taiwan had 6 consecutive cash years (2000-2005). The dot-com crash obliterated revenue growth across tech-adjacent companies. The strategy only began investing in 2006. This means there are effectively only 19 active investing years, and the CAGR figure reflects performance from a 2006 starting point embedded in a 25-year window. The TAIEX also sat out 2000-2005 in this comparison for apples-to-apples matching.

Full methodology: METHODOLOGY.md

For the US flagship results, see our US small-cap growth backtest.

What We Found

The semiconductor cycle problem

Taiwan's small-cap growth universe skews heavily toward semiconductor components, electronics manufacturing, and IT services. These are the businesses that feed TSMC, that supply assembly for global OEMs, that ride the chip upcycle. When the cycle turns up, revenue growth explodes. When it turns down, it collapses.

The result: feast-or-famine annual returns. 2006 delivered +63.0%. 2007 immediately gave back -36.2%. The strategy entered the market at an upcycle peak and paid for it the next year. This pattern repeats throughout the backtest. 2012 was +28.0%. 2013 was +15.0%. But the reversals are sharp.

A pure revenue-growth filter will always concentrate in cyclical upcycle winners. That's a timing problem. Annual rebalancing at a fixed calendar date doesn't align with semiconductor cycle timing, which can turn mid-year.

89% up capture versus TAIEX, but both lag SPY

Taiwan's small-cap growth screen captured 89.4% of TAIEX's upside and 72.8% of its downside. That's reasonable asymmetry relative to the local benchmark. But both the strategy and TAIEX lag SPY meaningfully. Taiwan small-caps aren't correlated with global equity indices in the same way as European markets. Their cycles are driven by the tech supply chain, not broad macro. So when SPY rallies on consumer spending or financial sector strength, Taiwan's semiconductor-heavy small-caps may not participate.

2024 illustrates this perfectly: while global markets rallied on AI enthusiasm and TSMC hit new highs, Taiwan's small-cap growth screen returned -11.37%. The TAIEX returned -2.57%. SPY returned +14.7%. The AI boom lifted TSMC (large-cap) massively. Small-cap component suppliers didn't get the same treatment, and even the broad TAIEX lagged SPY.

The 6 cash-year impact

Six consecutive years without positions (2000-2005) is the longest cash stretch of any exchange we tested. The strategy avoided the worst of the dot-com crash (SPY fell -14.8%, -20.8% in 2000-2001), but also missed the recovery rally in 2003-2004.

When the strategy finally deployed in 2006, it immediately captured a +63.05% year. That single year is a large contributor to the 25-year CAGR. Remove it and the picture gets worse. The TAIEX returned +33.06% in 2006, so the strategy had a strong first year even versus the local benchmark.

2024 performance breakdown

The worst excess year in the backtest versus SPY was 2023: -12.76 percentage points. SPY returned +35.64%. Taiwan returned +22.88%. TAIEX also participated in 2023, returning +35.64%. The 2024 result was negative for both the strategy (-11.37%) and TAIEX (-2.57%), while SPY continued upward. The AI/semiconductor boom was concentrated in large-cap names and didn't flow through to Taiwan's small-cap segment.

Annual Returns

| Year | Strategy | TAIEX | Excess vs TAIEX |

|---|---|---|---|

| 2000 | 0.00% | -41.11% | +41.11% |

| 2001 | 0.00% | +2.21% | -2.21% |

| 2002 | 0.00% | +2.01% | -2.01% |

| 2003 | 0.00% | +12.79% | -12.79% |

| 2004 | 0.00% | +9.13% | -9.13% |

| 2005 | 0.00% | +7.13% | -7.13% |

| 2006 | +63.05% | +33.06% | +30.00% |

| 2007 | -35.72% | -17.74% | -17.99% |

| 2008 | -4.27% | -9.33% | +5.07% |

| 2009 | +18.69% | +9.95% | +8.74% |

| 2010 | +15.72% | +19.70% | -3.98% |

| 2011 | -12.90% | -16.29% | +3.39% |

| 2012 | +28.27% | +9.13% | +19.14% |

| 2013 | +16.10% | +18.33% | -2.23% |

| 2014 | -7.08% | -1.11% | -5.96% |

| 2015 | -4.31% | -6.60% | +2.29% |

| 2016 | +7.89% | +18.86% | -10.97% |

| 2017 | +12.11% | +3.51% | +8.60% |

| 2018 | -9.10% | +0.81% | -9.91% |

| 2019 | +2.27% | +8.65% | -6.38% |

| 2020 | +35.97% | +50.02% | -14.05% |

| 2021 | -7.68% | -19.72% | +12.04% |

| 2022 | +19.49% | +20.17% | -0.68% |

| 2023 | +22.88% | +35.64% | -12.76% |

| 2024 | -11.37% | -2.57% | -8.81% |

The genuine alpha years where the strategy was active and outperformed TAIEX are: 2006, 2008, 2009, 2011, 2012, 2015, 2017, 2021. That's 8 out of 19 invested years, or 42%. The excess return is concentrated in 2006 (+30.00%) and 2012 (+19.14%). Remove those two outliers and the strategy barely matches TAIEX.

When It Works and When It Fails

When it works: Semiconductor upcycles. 2006 and 2012 show strong performance versus TAIEX. Also during broad EM recoveries (2009: +18.69%, +8.74% versus TAIEX). When Taiwan's export cycle aligns with a global growth pickup, the screen captures companies at peak revenue growth.

When it fails: Post-upcycle corrections (2007 immediately after 2006's surge: -35.72%, -17.99% versus TAIEX). Years when large-cap tech drives global indices but small-caps don't participate (2020, 2023, 2024). And extended sideways periods in Taiwan's domestic economy (2014-2015, 2018-2019).

The mismatch problem: The strategy rebalances in July. Taiwan's semiconductor cycle can turn within months. A company that looked like a revenue growth winner in April might be warning on guidance by July. Annual rebalancing at a fixed date is too slow to navigate this cycle.

Why Large-Cap Taiwan Works but Small-Cap Doesn't

TSMC's performance over this period is exceptional. Korean and Taiwanese large-cap tech generated real alpha for global investors. The small-cap segment doesn't share that quality.

The large-cap tech winners in Taiwan are genuinely dominant businesses with pricing power, IP moats, and captive customers. The small-cap growth filter selects for revenue acceleration, which in Taiwan means you're picking cyclical component suppliers and assembly contractors at their cyclical peaks. These are lower-margin, lower-moat businesses. The growth is real, but it reverses.

This is a different market structure problem than Europe. In Germany or Sweden, the small-cap screen fails because the market is efficiently priced. In Taiwan, it fails because the growth signal selects for the wrong kind of growth: cyclical rather than durable.

Limitations

Currency. Returns are in NT dollars. NTD/USD movements affect real returns for foreign investors.

Cyclical bias. The screen systematically overweights semiconductor cycle plays. This isn't diversified exposure to Taiwanese small-caps — it's a concentrated tech-adjacent cycle bet.

6 cash years. The long cash period means early excess return comparisons are distorted. The true performance window is 2006-2024.

52-week cycle mismatch. Annual rebalancing in July doesn't match semiconductor order cycle timing. More frequent rebalancing might improve results, but would also increase transaction costs in a less liquid market.

Liquidity. Taiwan has 24.4 average holdings, which is manageable. But some of the smaller stocks (near NT$500M) have limited daily volume.

Run It Yourself

Full backtest code is in our public repository: ceta-research/backtests.

The Taiwan filter uses exchange IN ('TAI', 'TWO') in the profile table. Market cap bounds are in NT dollars. Revenue growth uses revenue from income_statement with fiscal year lag.

Takeaway

Taiwan's small-cap growth screen barely beats the TAIEX (+0.29%/yr) and underperforms SPY by -3.47%/yr over 25 years. The 36% win rate versus both benchmarks shows consistent underperformance.

The problem isn't Taiwan's economy or stock market broadly. It's that the small-cap growth filter, applied to Taiwan's tech-heavy universe, selects for semiconductor cycle plays at their peak. The bust follows. Annual rebalancing can't time that cycle. The TAIEX itself lagged SPY, and the small-cap screen added almost no value versus the local benchmark.

The TSMC-era AI boom has reinforced the divergence between Taiwan's large-cap winners and small-cap supply chain. If anything, that divergence is widening, as AI capex concentrates in fewer, larger companies. The 2024 result (-11.37% for the strategy, -2.57% for TAIEX, +14.7% for SPY) is a data point worth taking seriously.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results. This is educational content, not investment advice.

References

- Banz, R. (1981). "The Relationship Between Return and Market Value of Common Stocks." Journal of Financial Economics, 9(1), 3-18.

- Fama, E. & French, K. (1992). "The Cross-Section of Expected Stock Returns." Journal of Finance, 47(2), 427-465.

- Fama, E. & French, K. (1993). "Common Risk Factors in the Returns on Stocks and Bonds." Journal of Financial Economics, 33(1), 3-56.

- Van Dijk, M. (2011). "Is size dead? A review of the size effect in equity returns." Journal of Banking & Finance, 35(12), 3263-3274.