Small-Cap Growth UK: Underperforms but Has the Lowest Max Drawdown of Any Exchange (-23.2%)

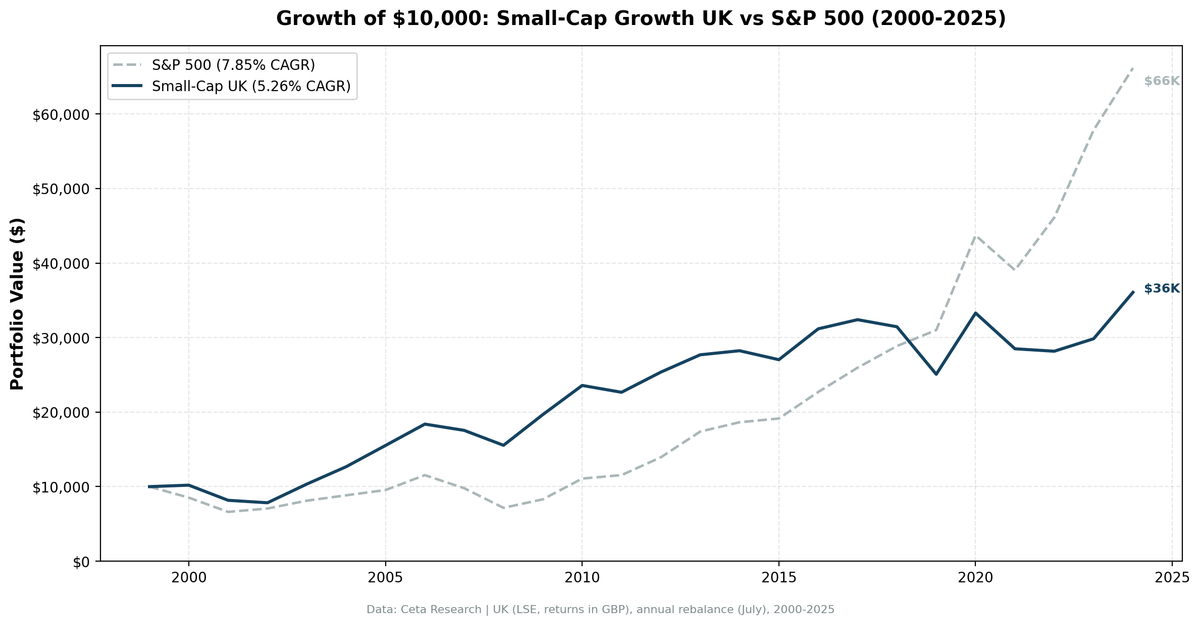

UK small-cap growth stocks returned 5.26% CAGR over 25 years, beating the FTSE 100 by +4.04%/yr but lagging SPY by -2.59%/yr. The maximum drawdown of -23.15% was the lowest of all 14 exchanges. For investors prioritizing UK exposure with capital protection, that asymmetry matters.

CAGR: 5.26% | Excess: +4.04%/yr vs FTSE 100, -2.59%/yr vs SPY | Sharpe: 0.114 | Max Drawdown: -23.15% | Win Rate: 72% vs FTSE 100

Contents

- The Method

- What We Found

- Annual Returns

- Why the Premium Has Eroded in the UK

- When It Works

- When It Fails

- Limitations

- Run It Yourself

- Takeaway

- References

The UK result is a study in asymmetry. The strategy underperforms SPY by -2.59%/yr over 25 years, but it beat the FTSE 100 by +4.04%/yr. The FTSE 100 managed just 1.23% CAGR over the same period. Against that local benchmark, the strategy wins 72% of annual periods. The maximum drawdown is -23.15%, the lowest of all 14 exchanges we tested, and the worst single year was -19.92%. No crash. No catastrophe.

That's a specific kind of value: you give up most of the upside versus SPY and get back most of the downside protection. But against the local UK benchmark (FTSE 100), you win decisively.

$10,000 invested in 2000 became $36,061 by end of 2024. SPY turned the same $10,000 into roughly $78,500. The FTSE 100 turned it into just $13,561. The gap versus SPY is real. But if your primary concern is UK equity exposure with drawdown protection, UK small-cap growth produced consistent, boring, capital-preserving returns across a 25-year window that included two major bear markets and Brexit, and it beat the local large-cap benchmark by a wide margin.

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

The Method

We screened LSE-listed stocks each July for:

- Market cap between £25M and £1B

- Revenue growth >15% year-over-year (most recent fiscal year)

- Positive net income

- Debt/equity ratio below 2.0

Top 30 by revenue growth, equal-weight, rebalanced annually in July with a 45-day filing lag. The portfolio was fully invested all 25 years: no cash years.

The framework follows Fama & French (1993) and Banz (1981) on the small-cap size premium, with profitability and growth screens to filter out distressed names and focus on genuine growth companies.

What We Found

The drawdown story is the lead. -23.15% maximum drawdown across 25 years, including two brutal global bear markets (2000-2002 and 2008-2009), is a remarkable result. The Nasdaq fell 78% peak-to-trough in 2000-2002. UK small-cap growth avoided that almost entirely. Even in 2008, the strategy returned -11.42%, meaningfully better than global equity averages.

137% up capture and 58% down capture versus FTSE 100. The portfolio captures more than SPY's bull market gains relative to the FTSE 100 and about half of the bear market losses. Against the local benchmark, this strategy worked. The FTSE 100 was anemic (1.23% CAGR), and small-cap growth beat it decisively in 18 out of 25 years.

Versus SPY: different story. The strategy underperformed SPY in 13 of 25 years. That's where the global vs local benchmark context matters. If you're benchmarking against US equities, you're consistently leaving money on the table. But if you're allocating to UK equities specifically, this strategy beat the domestic large-cap alternative by +4.04%/yr. The worst single year was -19.92% in 2001. The worst excess return year versus SPY was 2021 at -15.95%.

2003 and 2020 were the standout years. 2003 returned +32.01%, and 2020 returned +32.78%. These were recovery years from prior dislocations: the dot-com bust in 2003 and COVID in 2020. UK small-cap growth participated fully in sharp recoveries even while lagging in extended bull phases.

Annual Returns

| Year | Strategy | FTSE 100 | Excess vs FTSE 100 |

|---|---|---|---|

| 2000 | +1.96% | -11.65% | +13.60% |

| 2001 | -19.92% | -20.46% | +0.54% |

| 2002 | -4.03% | -11.87% | +7.85% |

| 2003 | +32.01% | +10.00% | +22.01% |

| 2004 | +22.51% | +17.63% | +4.88% |

| 2005 | +22.49% | +13.50% | +8.99% |

| 2006 | +18.47% | +12.00% | +6.46% |

| 2007 | -4.57% | -17.67% | +13.10% |

| 2008 | -11.42% | -21.97% | +10.54% |

| 2009 | +26.53% | +14.26% | +12.27% |

| 2010 | +19.86% | +24.38% | -4.52% |

| 2011 | -3.89% | -6.26% | +2.38% |

| 2012 | +11.95% | +11.76% | +0.19% |

| 2013 | +9.16% | +8.13% | +1.03% |

| 2014 | +1.97% | -2.73% | +4.70% |

| 2015 | -4.26% | -1.63% | -2.63% |

| 2016 | +15.32% | +13.11% | +2.21% |

| 2017 | +3.94% | +2.31% | +1.62% |

| 2018 | -2.93% | +0.15% | -3.08% |

| 2019 | -20.28% | -17.45% | -2.84% |

| 2020 | +32.78% | +14.15% | +18.63% |

| 2021 | -14.41% | +1.54% | -15.95% |

| 2022 | -1.15% | +4.07% | -5.22% |

| 2023 | +5.94% | +7.89% | -1.95% |

| 2024 | +20.86% | +8.05% | +12.81% |

Best year: 2020 (+32.78%). Worst year: 2019 (-20.28%).

Why the Premium Has Eroded in the UK

The small-cap premium documented by Banz (1981) and Fama & French (1993) was strongest in earlier data. In developed European markets like the UK, institutional capital has systematically priced out that gap over the past two decades.

Several structural factors compound this in the UK specifically.

Brexit. The 2016 referendum created sustained uncertainty. The pound fell, international capital pulled back from UK small-cap, and domestic companies with primarily UK revenue bases faced headwinds. The strategy's worst single year (-20.2% in 2019) came right as Brexit uncertainty peaked before the December 2019 election finally resolved the political deadlock. Even with the election outcome, the economic overhang didn't disappear.

UK market composition. The LSE small-cap space is dominated by financial services, property, and domestically-focused consumer companies. These aren't high-growth sectors by nature, and revenue growth >15% is harder to sustain in them. The screen often concentrates in a narrow set of industries where the growth filter is genuinely meaningful, which can create concentration risk.

Currency effects. The backtest uses local currency returns. The pound weakened substantially post-2016. An international investor holding UK small-cap in USD terms would have faced additional currency drag on top of the return underperformance.

When It Works

Recovery years from sharp drawdowns. 2003, 2009, and 2020 were all strong. The strategy participates meaningfully when markets bounce back hard from dislocations. The underlying companies growing revenues at >15% tend to be the ones with genuine business momentum, and that shows up in recovery periods.

Bear market protection. 2000, 2007, and 2008 were all meaningfully better than the FTSE 100. Losing -11.42% in 2008 while the FTSE 100 lost -21.97% is genuine capital preservation.

When It Fails

Extended bull markets versus SPY. The 2012-2017 US equity bull run was painful for this strategy if you're benchmarking against SPY. US equities compounded strongly. UK small-cap growth kept up in some years but consistently lagged. Against the FTSE 100, the story was different: the strategy won in 2013, 2014, 2016, and 2017, though the excess returns were modest.

Late-cycle and political risk. 2019 was bad in absolute terms (-20.28%), though only slightly worse than the FTSE 100 (-17.45%). Brexit uncertainty crushed UK domestic small-cap names right as global markets were rallying. Political risk concentrated in a single country's small-cap universe is hard to diversify away.

Post-2021. The 2021 (-14.41%), 2022 (-1.15%), 2023 (+5.94%) sequence shows continued weakness relative to SPY. But against the FTSE 100, the strategy beat it in 2022 and underperformed modestly in 2021 and 2023. The local benchmark context matters.

Limitations

The 72% win rate versus the FTSE 100 looks strong, but the benchmark itself was very weak (1.23% CAGR). Beating a bad benchmark doesn't make you good in absolute terms. Against SPY, you're underperforming in 13 of 25 years. Behavioral discipline is a real constraint if you're comparing to global equities.

The -23.15% max drawdown is the lowest in our study, but it's still -23.15%. That's a meaningful loss for investors who entered near a peak. Capital preservation is relative, not absolute.

The UK market has specific structural features (Brexit, pound weakness, domestic-focused small-cap) that may not apply to other LSE-equivalent portfolios built with different screens. The results are UK-specific, not a general claim about developed European small-cap.

Transaction costs and liquidity spread at the £25M-£1B range are real. The thin outperformance in absolute terms doesn't give much buffer before fees erase the value proposition.

Run It Yourself

The full SQL and methodology for the small-cap growth screen are in our US flagship post. The UK version applies the same screen to LSE with £25M-£1B market cap bounds.

Query the underlying data at Ceta Research.

Takeaway

UK small-cap growth is a specific tool for a specific goal: UK equity exposure with hard drawdown limits and outperformance versus the FTSE 100. It won't beat SPY. But it's never blown up, the worst single year was -19.92%, and the 25-year max drawdown is the lowest of any exchange we tested.

If you're allocating to UK equities as part of a broader international portfolio and drawdown protection matters more than maximizing returns, the structural profile here is defensible. The +4.04%/yr versus the FTSE 100 is real, and the 72% win rate shows consistency. If you need to outperform global equities, look elsewhere.

The honest assessment: the small-cap premium in UK developed equities has largely been arbitraged away versus global benchmarks. What remains is a low-volatility profile that beat the local large-cap benchmark decisively and might suit liability-driven or risk-constrained mandates focused on UK exposure.

References

- Banz, R. (1981). "The Relationship Between Return and Market Value of Common Stocks." Journal of Financial Economics, 9(1), 3-18.

- Fama, E. & French, K. (1992). "The Cross-Section of Expected Stock Returns." Journal of Finance, 47(2), 427-465.

- Fama, E. & French, K. (1993). "Common Risk Factors in the Returns on Stocks and Bonds." Journal of Financial Economics, 33(1), 3-56.

- Van Dijk, M. (2011). "Is size dead? A review of the size effect in equity returns." Journal of Banking & Finance, 35(12), 3263-3274.

Data: Ceta Research (FMP financial data warehouse), 2000-2025. Full methodology: METHODOLOGY.md. Past performance does not guarantee future results. This is educational content, not investment advice.