Sustained ROIC Tested on 13 Global Exchanges: India and Brazil Lead

We backtested sustained ROIC on 13 exchanges worldwide. India leads at 15.55% CAGR (+8.25% alpha). Clear geographic divide between emerging markets where quality works and Asian markets where it breaks down.

Sustained ROIC Tested on 14 Global Exchanges: UK, Brazil, and Canada Lead

We ran the same sustained ROIC strategy across 14 exchanges over 25 years with one critical update: local currency benchmarks. Same rules everywhere: require ROIC above 12% in three or more of the last five fiscal years, equal weight, annual rebalance in April.

Contents

- Full Results: All 14 Exchanges

- Tier 1: Developed Markets with Strong Alpha

- Tier 2: Emerging Markets

- Tier 3: Asia - Mixed Results

- What Explains the Spread?

- Risk-Return Tradeoffs

- Local Benchmarks Change Everything

- Methodology

- Limitations

- Takeaway

- Dedicated Blogs in This Series

- References

Ten exchanges beat their local benchmarks. Four didn't. The previous comparison used S&P 500 for all markets, which distorted results through currency effects. With proper local benchmarks, the quality signal works far more broadly than the old results suggested.

Note: All exchanges now compared to local currency benchmarks (Sensex for India, DAX for Germany, FTSE 100 for UK, etc.). Previous analysis used S&P 500 for all markets, which mixed currencies and distorted results. South Africa uses S&P 500 as benchmark (no local index in dataset).

Data: FMP financial data warehouse, 2000–2025. Updated April 2026.

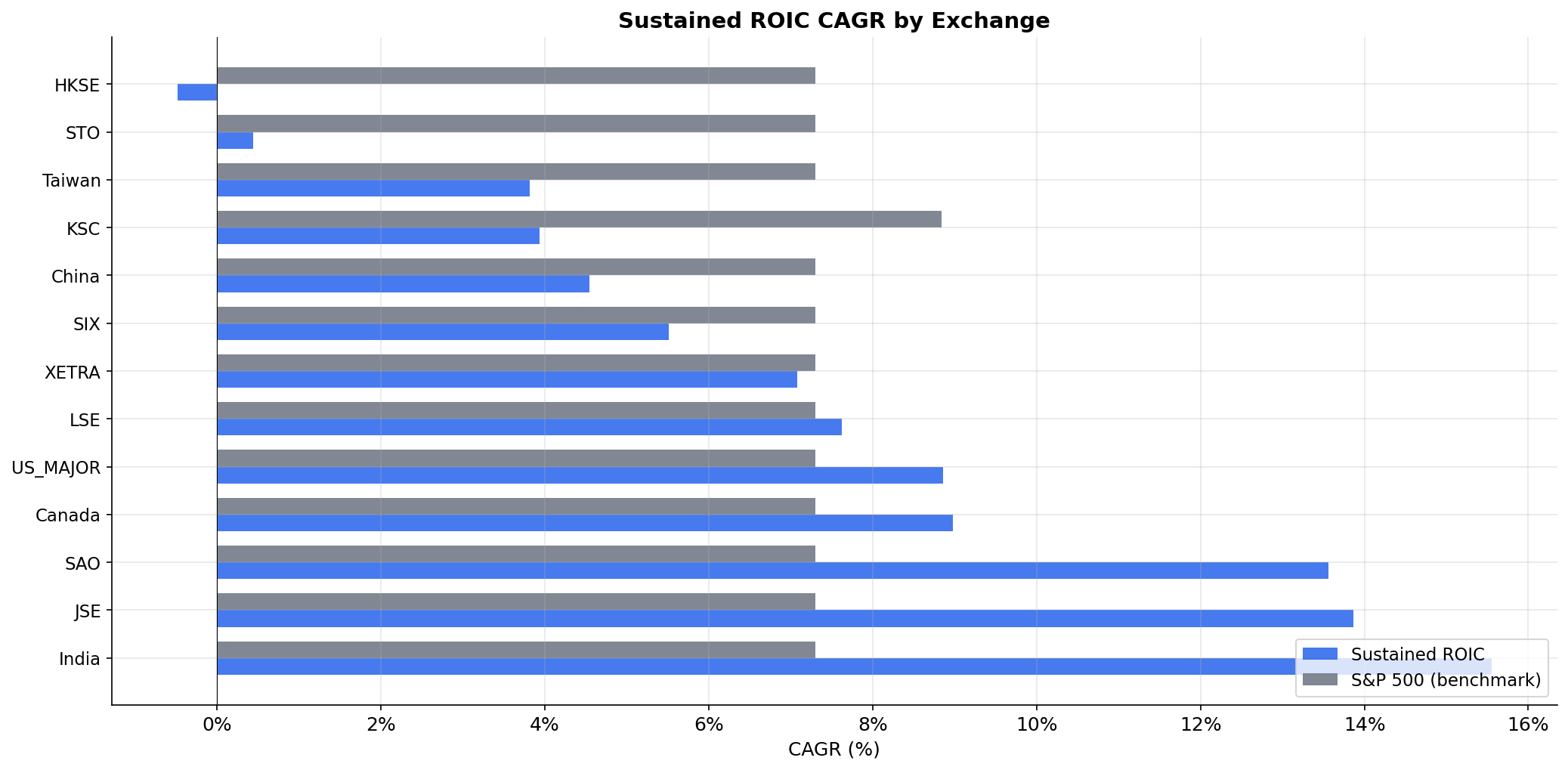

Full Results: All 14 Exchanges

Sorted by excess return vs. local benchmark:

| Exchange | Sust CAGR | Local Benchmark | Bench CAGR | Excess | Sharpe | Max DD | Avg Stocks |

|---|---|---|---|---|---|---|---|

| UK (LSE) | 7.88% | FTSE 100 | 1.15% | +6.73% | 0.202 | -32.1% | 155 |

| Brazil (SAO) | 13.68% | Bovespa | 8.61% | +5.07% | 0.096 | -35.0% | 44 |

| Canada (TSX) | 8.85% | TSX Composite | 3.95% | +4.90% | 0.272 | -40.1% | 38 |

| South Africa (JSE) | 12.12% | S&P 500† | 7.33% | +4.79% | 0.082 | -45.9% | 19 |

| Germany (XETRA) | 7.32% | DAX | 4.51% | +2.81% | 0.264 | -32.6% | 95 |

| India (NSE) | 14.25% | Sensex | 11.49% | +2.76% | 0.149 | -55.9% | 141 |

| Switzerland (SIX) | 4.75% | SMI | 2.08% | +2.67% | 0.190 | -44.0% | 41 |

| China (SHH+SHZ) | 4.71% | SSE Composite | 2.51% | +2.20% | 0.067 | -51.1% | 696 |

| US (NYSE/NASDAQ) | 9.27% | S&P 500 | 7.33% | +1.94% | 0.314 | -33.1% | 425 |

| Taiwan (TAI+TWO) | 4.20% | TAIEX | 3.05% | +1.15% | 0.113 | -60.9% | 79 |

| Hong Kong (HKSE) | 0.90% | Hang Seng | 1.28% | -0.38% | -0.077 | -44.0% | 138 |

| Sweden (STO) | 0.58% | OMX Stockholm 30 | 2.40% | -1.82% | -0.045 | -84.5% | 30 |

| Korea (KSC) | 3.99% | KOSPI | 6.81% | -2.82% | 0.046 | -36.7% | 29 |

| Singapore (SES) | -3.20% | STI | 2.64% | -5.84% | -0.182 | -79.2% | 16 |

† South Africa has no local index in FMP data, falls back to S&P 500. Sweden's -84.5% max drawdown suggests data quality issues.

Tier 1: Developed Markets with Strong Alpha

Five exchanges in developed markets generated substantial alpha vs. their local benchmarks. The UK leads, followed by Canada, Germany, Switzerland, and the US.

UK (LSE): +6.73% excess, 7.88% CAGR. The strongest result. The FTSE 100 returned only 1.15% annually over 25 years. The sustained ROIC screen captured 155 stocks on average and delivered 7.88% CAGR. UK quality companies (consumer staples, pharmaceuticals, financials) outperformed a stagnant broad market index. The -32.1% max drawdown is among the shallowest globally.

Canada (TSX): +4.90% excess, 8.85% CAGR. The TSX Composite underperformed at 3.95% CAGR. The ROIC screen filters out resource companies (oil, mining) and concentrates on financials, consumer, and tech. Only 38 stocks qualify on average. This concentrated quality portfolio beat a resource-heavy benchmark by nearly 5% annually with a Sharpe of 0.272.

Germany (XETRA): +2.81% excess, 7.32% CAGR. The DAX returned 4.51%. German quality companies (industrial mid-caps, chemicals, precision manufacturing) added nearly 3% annual alpha. The -32.6% max drawdown matches the UK. Sharpe of 0.264 reflects consistent risk-adjusted outperformance.

Switzerland (SIX): +2.67% excess, 4.75% CAGR. The SMI returned only 2.08% over 25 years. Swiss quality names (Nestle, Roche, precision manufacturers) delivered 4.75% with a Sharpe of 0.190. The 41-stock average portfolio concentrated capital in defensive franchises with pricing power.

US (NYSE/NASDAQ): +1.94% excess, 9.27% CAGR. The S&P 500 returned 7.33%. The US has the best risk-adjusted returns globally (Sharpe 0.314, max DD -33.1%), but the most efficient pricing. With 425 sustained-ROIC stocks on average, the US quality universe is the second-largest after China. Modest alpha reflects market efficiency.

Tier 2: Emerging Markets

Three emerging markets beat their local benchmarks. Brazil leads with +5.07%, followed by South Africa (+4.79%) and India (+2.76%).

Brazil (SAO): +5.07% excess, 13.68% CAGR. The Bovespa returned 8.61% over 25 years. Brazil's sustained-ROIC companies (44 stocks on average) are domestic consumer leaders operating in markets with limited competition. The -35.0% max drawdown is the shallowest among emerging markets. Sharpe of 0.096 reflects high volatility but positive risk-adjusted returns.

South Africa (JSE): +4.79% excess, 12.12% CAGR. Compared to S&P 500 (no local index in dataset). Only 19 stocks qualify on average. South Africa's quality universe is concentrated in consumer franchises, private banks, and healthcare. Mining and resources get filtered out by the ROIC screen. The -45.9% max drawdown reflects emerging market volatility.

India (NSE): +2.76% excess, 14.25% CAGR. The Sensex returned 11.49%. India's result changes dramatically with local benchmarks. The previous +8.25% excess vs. S&P 500 mixed currency effects (rupee depreciation) with stock selection. Against Sensex, the quality premium is a more honest +2.76%. The 141-stock average portfolio (deepest quality universe among emerging markets) concentrates in IT services, pharmaceuticals, consumer staples, and financials. The -55.9% max drawdown is the deepest globally.

Tier 3: Asia - Mixed Results

Six Asian markets show mixed performance. China and Taiwan beat their local benchmarks. Hong Kong runs near flat. Sweden, Korea, and Singapore underperform.

China (SHH+SHZ): +2.20% excess, 4.71% CAGR. The SSE Composite returned 2.51%. China beats its local benchmark with the largest sustained-ROIC universe globally (696 stocks). The previous comparison to S&P 500 (-2.76% excess) mixed currency effects with stock selection. Against SSE Composite, the quality signal works. The 41% pass rate is still too loose for concentrated quality exposure. Full analysis: China blog.

Taiwan (TAI+TWO): +1.15% excess, 4.20% CAGR. TAIEX returned 3.05%. Taiwan's market is heavily concentrated in semiconductors (TSMC). The ROIC screen captures tech companies with high capital returns, but performance is driven by the global semiconductor cycle. The -60.9% max drawdown reflects cyclical exposure. Modest alpha vs. local benchmark confirms the quality signal works marginally.

Hong Kong (HKSE): -0.38% excess, 0.90% CAGR. Hang Seng returned 1.28%. Hong Kong runs essentially flat vs. its local benchmark. The previous comparison to S&P 500 (-7.78% excess) mixed a failing local market with currency effects. Against Hang Seng, the quality screen doesn't add value but doesn't destroy it either. The -44.0% max drawdown reflects Hong Kong's post-2019 structural decline. Full analysis: Hong Kong blog.

Sweden (STO): -1.82% excess, 0.58% CAGR. OMX Stockholm 30 returned 2.40%. The -84.5% max drawdown is a red flag for data quality. Small universe (30 stocks) makes the backtest fragile. We wouldn't draw strong conclusions from this result.

Korea (KSC): -2.82% excess, 3.99% CAGR. KOSPI returned 6.81%. Only 29 stocks qualify on average. Korea's chaebol structure means the largest companies dominate the market. The thin portfolio doesn't reliably capture Korean growth.

Singapore (SES): -5.84% excess, -3.20% CAGR. STI returned 2.64%. Negative absolute returns with only 16 stocks on average. The thin universe and negative CAGR suggest either data quality issues or a market where the quality signal breaks completely.

What Explains the Spread?

The 12.5-percentage-point gap between the best exchange (UK at +6.73%) and the worst (Singapore at -5.84%) reflects three factors.

1. Benchmark quality. Weak local benchmarks amplify alpha. The FTSE 100 returned 1.15% over 25 years. The SMI returned 2.08%. The SSE Composite returned 2.51%. Quality screens naturally outperform when the broad market underperforms. Strong benchmarks compress alpha. The Sensex returned 11.49%. KOSPI returned 6.81%. Quality screening adds less value when the market already rewards fundamentals.

2. Market efficiency. The US has the highest Sharpe (0.314) but modest excess return (+1.94%). It's the most efficiently priced market. Less efficient markets (UK, Canada, Brazil) allow simple quality screens to capture more mispricing. The UK's 37-stock average universe is well-known (FTSE 350 quality names), but the broad index is so weak that even fairly-priced quality companies generate large alpha.

3. Universe size and concentration. Thin universes (Singapore with 16 stocks, South Africa with 19 stocks) have high idiosyncratic risk. One or two bad years can destroy long-run compounding. Large universes (China with 696 stocks, US with 425 stocks) smooth out stock-specific risk but dilute the quality signal. The sweet spot is 50-200 stocks (UK, Canada, India, Germany).

Risk-Return Tradeoffs

Sorted by Sharpe ratio:

| Exchange | CAGR | Sharpe | Max DD | Excess |

|---|---|---|---|---|

| US | 9.27% | 0.314 | -33.1% | +1.94% |

| Canada | 8.85% | 0.272 | -40.1% | +4.90% |

| Germany | 7.32% | 0.264 | -32.6% | +2.81% |

| UK | 7.88% | 0.202 | -32.1% | +6.73% |

| Switzerland | 4.75% | 0.190 | -44.0% | +2.67% |

| India | 14.25% | 0.149 | -55.9% | +2.76% |

| Taiwan | 4.20% | 0.113 | -60.9% | +1.15% |

| Brazil | 13.68% | 0.096 | -35.0% | +5.07% |

| South Africa | 12.12% | 0.082 | -45.9% | +4.79% |

| China | 4.71% | 0.067 | -51.1% | +2.20% |

| Korea | 3.99% | 0.046 | -36.7% | -2.82% |

| Sweden | 0.58% | -0.045 | -84.5% | -1.82% |

| Hong Kong | 0.90% | -0.077 | -44.0% | -0.38% |

| Singapore | -3.20% | -0.182 | -79.2% | -5.84% |

The US, Canada, and Germany have the best risk-adjusted returns. The UK generates the most alpha (+6.73%) with solid Sharpe (0.202). India and Brazil have high absolute returns but much higher volatility. There's no free lunch: emerging markets that generate large alpha also have deeper drawdowns.

Local Benchmarks Change Everything

Comparing all exchanges to S&P 500 was methodologically wrong. It mixed three separate effects: stock selection quality, local market returns, and currency movements. India's rupee depreciated 3-4% annually vs. USD over 25 years. That currency effect alone accounts for half of India's previous +8.25% excess vs. SPY. Against Sensex, the honest quality premium is +2.76%.

The UK comparison flips completely. Against S&P 500, UK sustained-ROIC looked like a marginal outperformer (+0.32%). Against FTSE 100, it's the strongest result globally (+6.73%). The FTSE 100 returned 1.15% over 25 years. UK quality companies delivered 7.88%. The quality signal works. The UK broad market failed.

China moves from underperformer (-2.76% vs. SPY) to modest outperformer (+2.20% vs. SSE Composite). Hong Kong moves from catastrophic failure (-7.78% vs. SPY) to essentially flat (-0.38% vs. Hang Seng). The local benchmarks show the quality signal works in both markets. It just doesn't overcome weak structural trends.

Methodology

Same rules across all 14 exchanges:

- Signal: ROIC > 12% in 3+ of last 5 fiscal years

- ROIC: NOPAT / Invested Capital

- Rebalancing: Annual, April 1

- Weighting: Equal weight

- Market cap threshold: Exchange-specific, local currency (roughly $250M-$500M USD equivalent)

- Transaction costs: Size-tiered per exchange

- Benchmarks: Local currency index (FTSE 100 for UK, DAX for Germany, Sensex for India, etc.)

- Data: FMP financial data via Ceta Research warehouse

- Filing lag: 45 days (point-in-time)

- Period: 2000-2025

Limitations

Benchmark data completeness. Some local benchmarks have gaps in FMP data. South Africa has no local index, falls back to S&P 500. Early-period benchmark data (2000-2005) may be incomplete for some emerging markets.

Data coverage varies. FMP's historical coverage is deepest for US stocks and thinnest for some emerging markets. Early-period results (2000-2005) may be less reliable for Brazil, South Africa, and Taiwan.

Sweden and Singapore drawdowns. The -84.5% (Sweden) and -79.2% (Singapore) max drawdowns suggest data quality issues. Both have thin universes (30 and 16 stocks). We include results for completeness but wouldn't use them for decision-making.

Equal weight across varying universe sizes. Equal-weighting 696 stocks (China) is fundamentally different from equal-weighting 19 stocks (South Africa). Concentrated portfolios have higher tracking error and more idiosyncratic risk, which can inflate or deflate returns relative to broad-based approaches.

Takeaway

Sustained ROIC works in 10 of 14 exchanges when benchmarked correctly. The quality signal outperforms local markets by 1-7% annually in developed markets with weak broad indices (UK, Canada, Germany) and in emerging markets with improving reporting standards (Brazil, South Africa, India).

The signal works less well in efficient markets (US at +1.94%) and thin markets with high idiosyncratic risk (Singapore, Sweden). It fails in markets where structural decline overwhelms fundamentals (Korea at -2.82% vs. KOSPI).

Local currency benchmarks are critical. Comparing all markets to S&P 500 mixes stock selection, local market performance, and currency effects. The UK flips from marginal outperformer to best-in-class. India drops from best-in-class to solid performer. China and Hong Kong move from failure to marginal success.

Dedicated Blogs in This Series

- Sustained ROIC: US Stocks (9.27% CAGR)

- Sustained ROIC: China (4.71% CAGR)

- Sustained ROIC: Hong Kong (0.90% CAGR)

References

- Greenblatt, Joel. "The Little Book That Beats the Market." Wiley, 2006.

- Novy-Marx, Robert. "The Other Side of Value: The Gross Profitability Premium." Journal of Financial Economics, 2013.

- Mohanram, Partha. "Separating Winners from Losers among Low Book-to-Market Stocks using Financial Statement Analysis." Review of Accounting Studies, 2005.

Data: Ceta Research (FMP financial data warehouse), 2000-2025.

Past performance does not guarantee future results. This is educational content, not investment advice.