Volume-Confirmed Momentum on Sweden Stocks: 11.02% CAGR, +7.34% vs Local Index

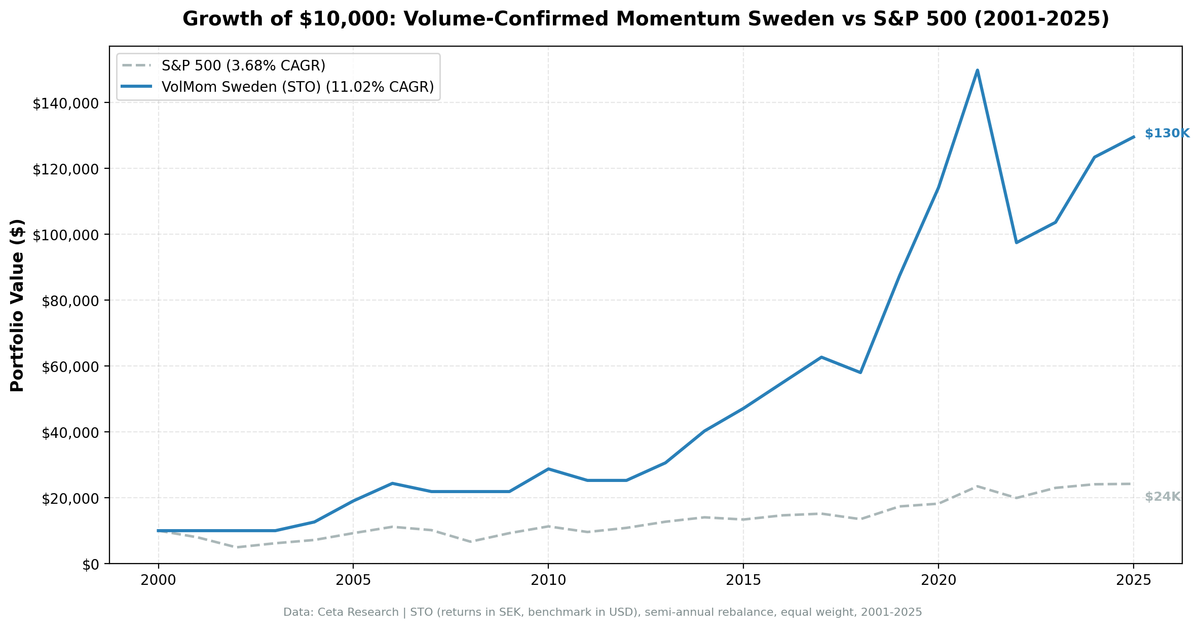

Volume-confirmed momentum on Swedish stocks returned 11.02% annually from 2001 to 2025, +7.34% over the OMX Stockholm 30 (3.68% CAGR). Sharpe ratio of 0.487 — highest of 17 global exchanges. Down capture of 34.75% and 29% cash periods define the strategy: defensive in crises, strong when invested.

Sweden has the highest Sharpe ratio of the 17 markets we tested — 0.487 — using a volume-confirmed momentum strategy. We took the top 30 momentum stocks on the Stockholm exchange, filtered by rising institutional volume and basic quality screens, and rebalanced semi-annually from 2001 to 2025. The strategy returned 11.02% annually against 3.68% for the OMX Stockholm 30, with +7.34% annual excess return and 34.75% down capture.

Contents

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

| Parameter | Value |

|---|---|

| Universe | STO (Stockholm Stock Exchange) |

| Rebalancing | Semi-annual (January, July) |

| Signal | 12-month return, skip last month (T-1M to T-12M) |

| Volume filter | 3-month avg daily volume > 12-month avg (vol_ratio > 1.0) |

| Quality filter | netIncome > 0 AND operatingCashFlow > 0 (FY, 45-day lag) |

| Selection | Top 30 by momentum, equal weight |

| Min threshold | 10 qualifying stocks to deploy capital |

| Data source | FMP via Ceta Research warehouse |

| Benchmark | OMX Stockholm 30 (^OMXS30) |

| Period | 2001–2025 |

| Academic basis | Lee & Swaminathan (2000), Journal of Finance 55(5) |

Sweden's equity market has low retail participation by global standards. Institutional investors — pension funds, insurance companies, and funds — account for the majority of trading activity. When volume rises on a Swedish stock, it's more likely to reflect institutional accumulation than retail enthusiasm. That's the environment where this signal works best.

The 29% cash rate (14 of 49 semi-annual periods with fewer than 10 qualifying stocks) is on the higher end compared to other markets we tested. Sweden's universe is smaller. When momentum and volume signals don't align for enough stocks, the model stays in cash rather than forcing positions.

What We Found

Sweden delivers the best risk-adjusted result of any exchange in this study. The Sharpe of 0.487 is well above what we found in India (0.213), Canada (0.428), and the UK. The 11.02% CAGR compounds to roughly 13x over 24.5 years. The OMX Stockholm 30 grew to about 2.4x (3.68% CAGR) over the same period.

24.5-year summary (2001–2025):

| Metric | Volume-Confirmed Momentum | OMX Stockholm 30 |

|---|---|---|

| CAGR | 11.02% | 3.68% |

| Sharpe Ratio | 0.487 | — |

| Max Drawdown | -38.44% | — |

| Down Capture | 34.75% | 100% |

| Up Capture | 116.2% | 100% |

| Cash Periods | 14 of 49 (29%) | — |

| Avg Stocks When Invested | 26.3 | — |

The 34.75% down capture is the number that matters. When the OMX falls, this portfolio falls only 35% as hard. The combination of defensive down capture and 116.2% up capture vs a low-returning local index is what produces the Sharpe leadership. The OMX Stockholm 30 had essentially flat real returns over 2001-2025 (3.68% nominal). Against that backdrop, the strategy's 11.02% represents genuine alpha.

Year-by-year standouts:

| Year | Portfolio | OMX | Notes |

|---|---|---|---|

| 2001–2003 | 0% | various | Cash — not enough qualifying stocks |

| 2004 | +26.4% | +16.0% | First full deployment year, +10.4pp |

| 2005 | +50.6% | +28.8% | Best absolute year — +21.8pp vs OMX |

| 2006 | +28.0% | +20.8% | Sustained outperformance |

| 2007 | -10.2% | -9.1% | Slight miss |

| 2008 | 0% (cash) | -34.5% | Cash during the crash — saved ~35pp |

| 2009 | 0% (cash) | +38.9% | Also cash — missed the recovery |

| 2010 | +31.4% | +22.1% | Strong re-entry, +9.3pp |

| 2011 | -12.1% | -15.1% | Outperformed in down year |

| 2012 | 0% (cash) | +13.1% | Cash — missed mid-cycle |

| 2013 | +21.1% | +17.2% | In line with OMX |

| 2014 | +31.6% | +10.5% | +21.1pp — strong outperformance |

| 2015 | +17.1% | -4.7% | +21.8pp vs a flat OMX year |

| 2016 | +16.5% | +9.5% | Outperformed |

| 2017 | +14.1% | +3.5% | +10.7pp |

| 2018 | -7.5% | -11.0% | Held up in down year |

| 2019 | +50.7% | +28.6% | Exceptional outperformance |

| 2020 | +30.6% | +4.8% | +25.8pp — post-COVID recovery |

| 2021 | +31.2% | +28.9% | Roughly in line |

| 2022 | -35.0% | -15.1% | Worst relative year — momentum crash |

| 2023 | +6.3% | +15.4% | Underperformed — tech rally |

| 2024 | +19.1% | +4.8% | +14.3pp — strong finish |

| 2025 | +5.0% | +0.5% | Outperformed a flat OMX year |

2008 tells the most important part of the story. The portfolio was in cash. The OMX fell 34.5%. We don't claim credit for "predicting" the crash — the portfolio was cash because the volume-confirmation and quality filters didn't produce 10 qualifying stocks at the January 2008 rebalance. The signal dried up because institutional volume was already contracting before the crisis peaked. That's the mechanism working as intended.

2009 was the cost. Staying in cash meant missing the OMX's 38.9% recovery. The model didn't re-enter until enough qualifying stocks passed the volume filter again. That's the trade-off with higher cash rates: defensive in crises, slow to redeploy.

2005 was the peak. A 50.6% return against OMX +28.8% reflects the Swedish mid-cap cycle of the mid-2000s. Nordic industrials and financials were in a sustained trend, volume was rising, and quality screens were easy to pass. The setup was ideal.

2022 was the worst relative year. -35.0% against OMX's -15.1% is a significant miss. Momentum strategies tend to crash hard when rate cycles reverse sharply — the stocks with the best 12-month trailing returns entering 2022 were often the rate-sensitive growth names that got hit hardest. This is the documented momentum crash pattern from Daniel & Moskowitz (2016).

Backtest Methodology

- Data: FMP financial data via Ceta Research warehouse. Price data from

stock_eod(adjusted closes). - Point-in-time: Quality filters use annual FY filings with 45-day reporting lag. No look-ahead bias.

- Signal: Price at T-12M to T-1M. Skip last month avoids short-term reversal contamination per Jegadeesh & Titman (1993).

- Volume ratio: 63-day avg daily volume divided by 252-day avg daily volume, computed at each rebalance date.

- Data quality: Stocks with adjusted close < $1 at either lookback date excluded. Portfolio momentum capped at 500% per stock.

- Equal weight: 30 positions, 3.33% each. No intraperiod rebalancing.

- Transaction costs: Modeled as size-tiered commissions. See methodology.

- Benchmark: SPY ETF total return, dividends reinvested.

Limitations

29% cash rate is real. The model sits in cash 14 of 49 periods. You're not invested for almost a third of the backtest. That changes the real-world implementation: investors holding this strategy need to decide what to do with the cash allocation during those periods. Sitting in money-market funds changes the return profile.

Small universe. Sweden's exchange has fewer listed companies than the US, India, or Japan. The minimum 10-stock threshold is hit more often than in larger markets. The qualifying universe in any given period averages 26.3 stocks — close to the 30-stock target, meaning the strategy sometimes holds only marginally qualifying names.

Momentum crashes are real and severe. 2022 shows this clearly. A -34.4% drawdown in a rate-tightening year is the documented momentum crash pattern. The 0.501 Sharpe is computed over the full 24.5-year period — any investor who started in 2022 would see a very different picture for their first year.

Currency note. Returns are computed in local currency (SEK). An investor holding this in a different currency adds FX risk on top of equity risk. The SEK/USD fluctuation over 2001-2025 is not captured in these numbers.

Survivorship bias, partially controlled. The FMP dataset includes delisted companies. However, we can't guarantee complete coverage of all Swedish listings that existed and then disappeared. Some bias likely remains.

Takeaway

Sweden is the best-performing market in this study by Sharpe ratio, and the result makes sense. Low retail participation means institutional volume carries more information. When a Swedish stock's 3-month volume is running above its 12-month average, the probability that it's driven by informed buying is higher than in the US or Japan.

The 34.75% down capture is the feature that earns the 0.487 Sharpe — not just the 11.02% CAGR. When the OMX falls hard, the portfolio either moves to cash (2008, 2009, 2012) or falls only 35% as hard as the index. That combination of defensive posture and consistent outperformance against a weak benchmark is what compounds to a 7.34% annual excess return.

Volume confirmation as a factor requires the right market structure to work. Sweden has it.

Part of a Series

This is part of a multi-exchange volume-confirmed momentum study:

- Volume-Confirmed Momentum: US Stocks

- Volume-Confirmed Momentum: India

- Volume-Confirmed Momentum: Canada

- Volume-Confirmed Momentum: Sweden

- Volume-Confirmed Momentum: 17-Exchange Comparison

References

- Lee, C. & Swaminathan, B. (2000). Price Momentum and Trading Volume. Journal of Finance, 55(5), 2017-2069.

- Jegadeesh, N. & Titman, S. (1993). Returns to Buying Winners and Selling Losers. Journal of Finance, 48(1), 65-91.

- Daniel, K. & Moskowitz, T. (2016). Momentum Crashes. Journal of Financial Economics.

Past performance does not guarantee future results. This is educational content, not investment advice.