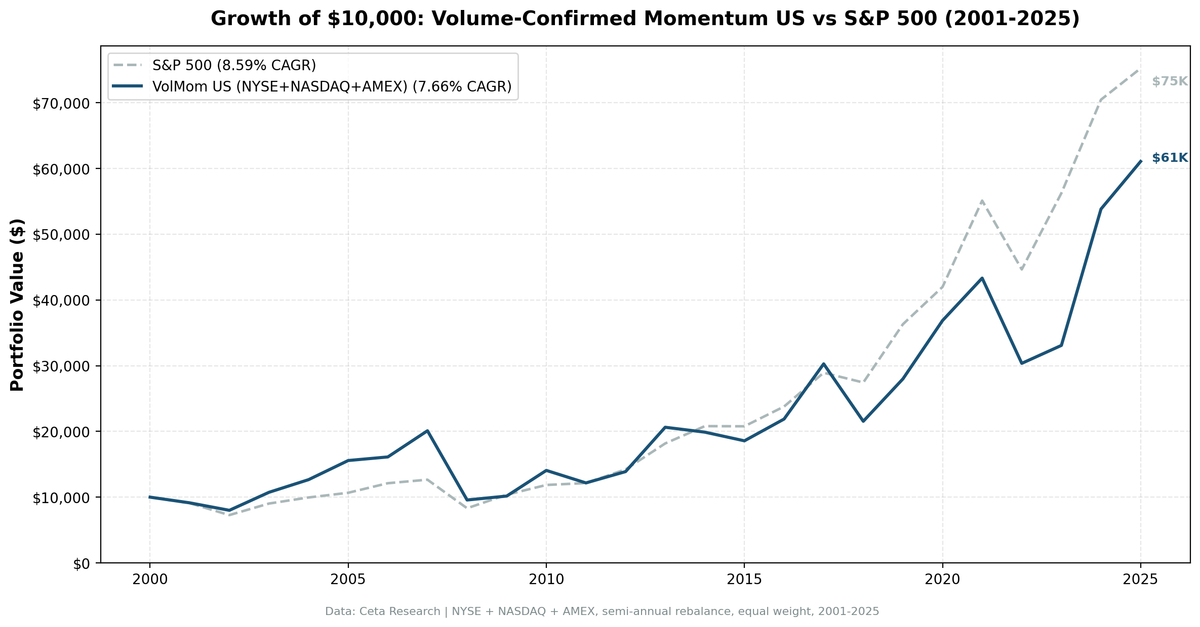

Volume-Confirmed Momentum on US Stocks: 7.66% CAGR vs 8.59% for the Index

We added volume confirmation to 12-month momentum on US stocks: rising 3-month volume, positive earnings, positive cash flow. From 2001 to 2025, the strategy returned 7.66% annually vs 8.59% for SPY — with 148.3% down capture. Volume signals are noise in the world's most traded market.

Volume confirmation does nothing for momentum in US equities. We filtered the top 30 momentum stocks using a rising-volume signal — 3-month average daily volume exceeding the 12-month average — plus basic quality screens. From 2001 to 2025, the strategy returned 7.66% annually against 8.59% for SPY. The 148.3% down capture tells the real story: when the market falls, this portfolio falls 48% harder.

Contents

Data: FMP financial data warehouse, 2000–2025. Updated March 2026.

Method

| Parameter | Value |

|---|---|

| Universe | NYSE, NASDAQ, AMEX |

| Rebalancing | Semi-annual (January, July) |

| Signal | 12-month return, skip last month (T-1M to T-12M) |

| Volume filter | 3-month avg daily volume > 12-month avg (vol_ratio > 1.0) |

| Quality filter | netIncome > 0 AND operatingCashFlow > 0 (FY, 45-day lag) |

| Selection | Top 30 by momentum, equal weight |

| Min threshold | 10 qualifying stocks to deploy capital |

| Data source | FMP via Ceta Research warehouse |

| Benchmark | S&P 500 (SPY) |

| Period | 2001–2025 |

| Academic basis | Lee & Swaminathan (2000), Journal of Finance 55(5) |

The volume filter is the key addition over pure momentum. Lee & Swaminathan (2000) showed that high-volume momentum stocks sustain outperformance longer than low-volume momentum stocks, arguing that rising volume signals institutional conviction. The quality filter removes stocks with negative earnings or negative operating cash flow, cutting speculative names from the pool.

What We Found

The strategy underperforms SPY by 0.92% annually. Over 24.5 years, that compounds: $1 grew to roughly 6.1x vs 7.5x for SPY. Volume confirmation doesn't just fail to add alpha — it adds crash risk.

24.5-year summary (2001–2025):

| Metric | Volume-Confirmed Momentum | S&P 500 (SPY) |

|---|---|---|

| CAGR | 7.66% | 8.59% |

| Total Return | ~511% | ~652% |

| Sharpe Ratio | 0.235 | — |

| Max Drawdown | -58.52% | -38.01% |

| Down Capture | 148.3% | 100% |

| Up Capture | 123.0% | 100% |

| Cash Periods | 0 of 49 (0%) | — |

| Avg Stocks Held | 29.3 | — |

Down capture of 148.3% means the portfolio falls 1.48x harder than SPY during down periods. Up capture of 123.0% means it captures more of the upside. But the downside penalty is bigger than the upside benefit, and it shows in the 24.5-year return gap.

Year-by-year standouts:

| Year | Portfolio | SPY | Notes |

|---|---|---|---|

| 2002 | -12.4% | -19.9% | Outperformed during dot-com crash |

| 2003 | +34.3% | +24.1% | Recovery led by quality names |

| 2004 | +17.9% | +10.2% | Continued outperformance |

| 2005 | +23.0% | +7.2% | Strongest relative year of the mid-2000s |

| 2006 | +3.5% | +13.7% | Momentum stalled — 10pp miss |

| 2007 | +24.7% | +4.4% | Pre-crisis strength |

| 2008 | -52.4% | -34.3% | Down capture problem exposed |

| 2009 | +6.2% | +24.7% | Missed the recovery by 18.5pp |

| 2013 | +48.6% | +27.8% | Best outperformance year outside 2024 |

| 2018 | -28.9% | -5.2% | Rate shock — leveraged names hit hard |

| 2024 | +62.7% | +25.3% | AI/tech momentum — best absolute year |

| 2025 | +13.4% | +6.8% | Continued outperformance |

2008 and 2009 together define the US result. The portfolio lost 52.4% in 2008 — 18.1 percentage points worse than SPY. That's the down capture problem in one year. Then in 2009, while SPY recovered 24.7%, this portfolio captured only 6.2%. The stocks with the strongest volume-confirmed momentum entering 2009 were the defensive names that hadn't fallen far. The beaten-down financials and cyclicals that led the recovery weren't in the portfolio. Two bad years in sequence cost compounding that the strategy never recovered.

2006 and the momentum stall. The portfolio returned 3.5% against SPY's 13.7%. This was a period when value and cyclicals led, breaking momentum's narrative. Rising-volume names had run hard through 2003-2005 and then consolidated while the broader market kept climbing.

2024 was the best year. At +62.7%, AI and semiconductor momentum drove exceptional returns. The volume filter likely helped here — genuinely institutionally-driven buying in tech names coincided with rising relative volume. One year doesn't fix the 24.5-year gap, but it shows the factor still fires under the right conditions.

Why volume signals don't work in the US. In the most traded equity market in the world, volume is noise. Retail flows, ETF rebalancing, options hedging, and algorithmic trading all generate volume that has no predictive relationship with future returns. The institutional-conviction signal that Lee & Swaminathan identified in 2000 was real in a pre-ETF, pre-algo market. Today, US volume data contains too many confounding signals to filter on it reliably.

Backtest Methodology

- Data: FMP financial data via Ceta Research warehouse. Price data from

stock_eod(adjusted closes). - Point-in-time: Quality filters use annual FY filings with 45-day reporting lag. No look-ahead bias.

- Signal: Price at T-12M to T-1M. Skip last month avoids short-term reversal contamination per Jegadeesh & Titman (1993).

- Volume ratio: 63-day avg daily volume divided by 252-day avg daily volume, computed at each rebalance date.

- Data quality: Stocks with adjusted close < $1 at either lookback date excluded. Portfolio momentum capped at 500% per stock.

- Equal weight: 30 positions, 3.33% each. No intraperiod rebalancing.

- Transaction costs: Modeled as size-tiered commissions. See methodology.

- Benchmark: SPY ETF total return, dividends reinvested.

Limitations

Negative alpha in the world's most efficient market. The -1.59% annual drag over 24.5 years is consistent with a crowded factor. Academic papers have documented US momentum since 1993. Systematic funds have been trading it for 30 years. The volume overlay adds complexity without adding returns.

Down capture is the structural problem. 139.3% down capture means this strategy makes portfolios more vulnerable to market crashes, not less. The quality filter (positive income, positive OCF) doesn't prevent large drawdowns — it just removes the worst speculative stocks from a pool that still concentrates in high-beta momentum names.

The Lee & Swaminathan result may not translate. The 2000 paper used data from a different market structure. Today's US volume is dominated by ETF flows and high-frequency trading. The signal that identified institutional accumulation in 1990s data may not identify the same thing in 2020s data.

Semi-annual rebalancing misses momentum decay. The strategy rebalances only in January and July. Momentum is a faster-moving signal. A holding period of six months means the portfolio carries stale momentum signals through much of the year.

Takeaway

Volume-confirmed momentum underperforms a simple SPY investment in the US. The 7.66% CAGR vs 8.59%, 148.3% down capture, and Sharpe of 0.235 don't make a case for running this strategy in US equities. The volume filter adds screening complexity without adding return.

The US is the wrong market for volume-based momentum screens. The comparison across exchanges is more instructive: the same strategy in Sweden returns 11.02% annually with +7.34% excess over the OMX Stockholm 30. Germany returns 8.61% with +3.03% over the DAX. The factor works where institutional volume signals carry genuine information — and in the US, they don't.

Part of a Series

This is part of a multi-exchange volume-confirmed momentum study:

- Volume-Confirmed Momentum: US Stocks

- Volume-Confirmed Momentum: India

- Volume-Confirmed Momentum: Canada

- Volume-Confirmed Momentum: Sweden

- Volume-Confirmed Momentum: 17-Exchange Comparison

References

- Lee, C. & Swaminathan, B. (2000). Price Momentum and Trading Volume. Journal of Finance, 55(5), 2017-2069.

- Jegadeesh, N. & Titman, S. (1993). Returns to Buying Winners and Selling Losers. Journal of Finance, 48(1), 65-91.

- Daniel, K. & Moskowitz, T. (2016). Momentum Crashes. Journal of Financial Economics.

Past performance does not guarantee future results. This is educational content, not investment advice.