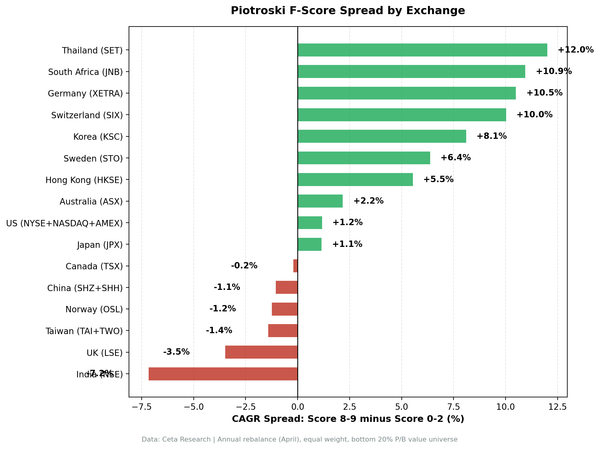

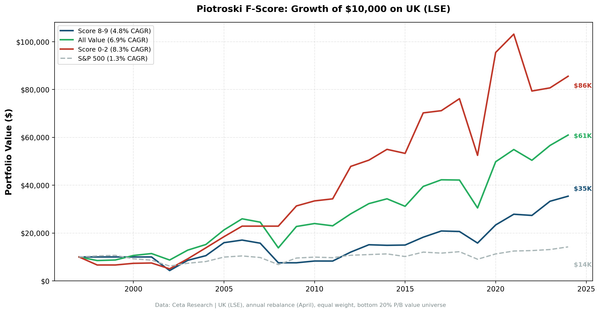

piotroski

Piotroski F-Score in the UK: Beats the FTSE, Loses to Score 0-2

UK Score 8-9 returned 4.8% CAGR over 27 years, beating the FTSE 100 (1.3%) by +3.48%. But the unfiltered value universe returned 6.9% and Score 0-2 returned 8.3%. Spread: -3.5%. Selection alpha -2.1%, avoidance alpha -1.3%.