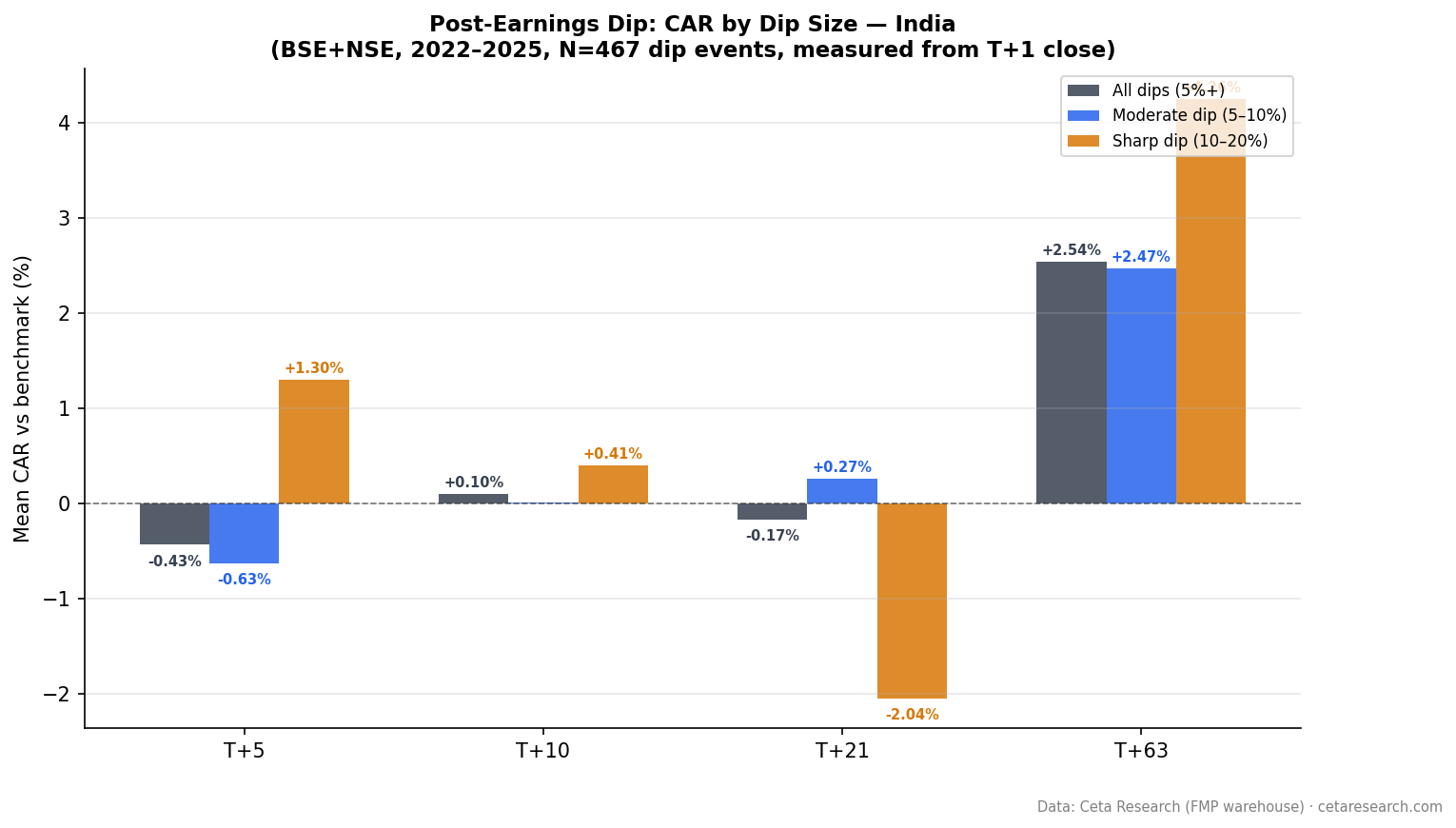

Post-Earnings Dip in India: Flat for a Month, Then +2.54%** at Three Months

India beat-and-dip events show a delayed reversion pattern. T+21 is flat (-0.17%, t=-0.42). T+63 is +2.54%** (t=3.55). 467 events from BSE and NSE, with 78% from 2023–2024 — a data caveat worth understanding before trading on this.

India's Post-Earnings Dip: Three Months to Flip the Narrative

India beats earnings and drops 5%+. At one month, nothing has happened. At three months, stocks have recovered +2.54% vs benchmark. The reversion is real, but slow — and the data has a caveat worth knowing before you read too much into the numbers.

Contents

- The Signal

- What We Found

- The Dip Size Breakdown

- The Data Caveat

- Why the Delay?

- Practical Implications

- Limitations

- Takeaway

The Signal

Same setup as the global study: a company beats earnings estimates (epsActual > epsEstimated), and the stock drops ≥ 5% from T-1 close to T+1 close. We measure CAR from T+1 close at T+5, T+10, T+21, and T+63 windows.

Universe: BSE and NSE-listed stocks with market cap above ₹20B (approximately $230M USD). Data from FMP, 2016–2025. 467 total events.

Benchmark: INDA (iShares MSCI India ETF). CAR = India stock return minus INDA return.

What We Found

India shows a clear delayed reversion pattern: flat to slightly negative for the first month, then a statistically significant recovery at T+63.

| Window | Mean CAR | t-stat | N | Hit Rate |

|---|---|---|---|---|

| T+5 | -0.43% | -1.86 | 467 | 40.7% |

| T+10 | +0.10% | +0.35 | 441 | 46.9% |

| T+21 | -0.17% | -0.42 | 442 | 47.3% |

| T+63 | +2.54%** | +3.55 | 457 | 48.4% |

p<0.05, p<0.01

The T+5 period is mildly negative and the T+10 and T+21 results are flat (not statistically significant). Then T+63 jumps to +2.54% with a t-stat of 3.55. Something flips between 21 and 63 trading days.

The hit rate at T+63 is 48.4% — just below the coinflip. The positive mean is driven by a subset of strong recoveries, not a consistent effect across all events. The median at T+63 is -0.69%, meaning more than half of events still underperform the benchmark at 3 months.

The Dip Size Breakdown

| Dip Category | N | T+21 CAR | t-stat | T+63 CAR | t-stat |

|---|---|---|---|---|---|

| All dips (5%+) | 467 | -0.17% | -0.42 | +2.54% | +3.55** |

| Moderate (5–10%) | 401 | +0.27% | +0.63 | +2.47% | +3.28** |

| Sharp (10–20%) | 57 | -2.04% | -1.76 | +4.26% | +1.70 |

The T+63 signal is concentrated in the moderate 5–10% dip group (n=401, t=3.28). The 10–20% group has only 57 events, and while the mean T+63 CAR is +4.26%, it's not significant (t=1.70). The dip_20 category has just 9 events — not meaningful.

The story is: moderate dips in India recover at 3 months, consistently enough to be statistically significant. Sharp dips have too few events to draw firm conclusions.

The Data Caveat

India's result needs a note. The effective data window is concentrated in 2022–2025. Looking at the yearly breakdown:

| Year | Events |

|---|---|

| 2016–2021 | 11 (combined) |

| 2022 | 27 |

| 2023 | 106 |

| 2024 | 193 |

| 2025 | 130 |

97% of India's 467 events are from 2022 or later, with 64% concentrated in 2023 and 2024 alone. FMP's India coverage expanded significantly around 2022–2023. This means the T+63 result of +2.54%** is telling you about how beat-and-dip events behaved during one specific period — primarily 2023 and 2024 — when Indian markets were in a strong bull phase.

The t-stat of 3.55 is real. But extrapolating it as a structural property of the Indian market over 25 years would be overreading the data. It's a recent-period finding with a promising t-stat and a sample size that's still building.

This is the same caveat that applies to India's beat-streaks result. As the FMP India data pipeline matures, this will sharpen.

Why the Delay?

The T+21 flat period followed by T+63 recovery is unusual. A few explanations are consistent with it:

Institutional re-evaluation cycles. Indian institutional investors may re-analyze quarterly results more slowly than US counterparts, especially for mid-cap names that get initial sell pressure from retail traders.

Earnings quality reassessment. Many of the beat events in India involve companies where the sell-off is driven by non-EPS concerns (guidance, revenue mix, promoter pledging news) that are later re-evaluated as the quarter's data is absorbed.

Market structure. India has a significant retail trading base that reacts quickly to post-earnings price moves and may reverse that initial reaction over the subsequent 40–60 days once fundamental data is more broadly digested.

None of these is proven by the data. They're consistent explanations for the delay pattern, but the sample is too recent to test them rigorously.

Practical Implications

The T+63 result suggests a patient entry approach: if you're watching a beat-and-dip event in India, waiting until 30–40 days post-announcement before establishing a position may avoid the T+5 to T+21 flat/weak period. The recovery appears to be a second-order institutional re-rating rather than an immediate retail reversal.

The hit rate of 48.4% at T+63 means this isn't a reliable individual stock trade. It's a statistical effect in an aggregate sample — a 1-in-2 chance of beating the benchmark isn't a usable edge at the stock level.

Limitations

Data recency. 97% of events from 2022 or later (64% from 2023–2024). Strong bull market tailwinds during that period. This is the biggest risk to the result.

Benchmark. INDA tracks the MSCI India Index. Some India mid-caps in the sample may not be well-represented in the benchmark, which could inflate or deflate the benchmark-adjusted return.

Small sample for dip_10. 57 events in the sharp dip category is too few for reliable conclusions. The 10–20% dip T+63 CAR of +4.26% looks compelling but carries high uncertainty.

Takeaway

India is an interesting case: delayed mean reversion with a legitimate statistical signal that's concentrated in recent years during a strong market period. The T+63 result of +2.54%** is real but should be read with caution — it's a 2023–2024 finding, not a 25-year structural property.

Check back in 2-3 years as the India pipeline data matures. If the T+63 signal holds across a full market cycle, including a downturn, it becomes much more credible.

Part of a series: Post-earnings dip mean reversion tested across 12 exchanges. See US, Taiwan, and the global comparison.

Data: FMP earnings surprises + adjusted prices, 2016–2025. BSE and NSE. Market cap > ₹20B. 467 beat-and-dip events. CAR vs INDA ETF, measured from T+1 close.